You are right, most regulations are shared. Maybe I wasn’t clear.

In a traditional pension fund that pays a pension, you need to match your assets and liabilities. That is what they call “security of realization of retirement planning” (sorry, just my simple translation of Art 50, al 2 OPP2). But what happens when you have no “retirement planning”? (ie: you don’t pay any pensions) Then you can deviate from the investment limits if you prove in your annual report that you respect Art 50, al 1-3.

I am not sure if the law was interpreted more leniently, but it’s been a couple of years that we have seen 3a solutions with almost 100% equities (UBS offers for example Vitainvest 100 since November 2018).

You are right that “the regulators could have done things differently”, but in my opinion it was easier to leave the current law and just interpret it a little more liberally. Also, we have to keep in mind that these laws were instituted before we had negative interest rates, so times were different.

I think the difference is that it’s a fund, they decide what gets in it in the end (and it’s still 20% CH equity). It explicitly calls out its compliance to BVV regulations.

If you were to invest in 100% bitcoin through finpension (is that possible), it’s not like the bitcoin fund can say it follows BVV regulation right? Isn’t there a difference between having a fund with explicit BVV compliance and full freedom of asset allocations?

Of course. I don’t think that Finpension allows you to put whatever asset you want in your allocation. I suppose they only allow some pre-screened funds and you get to choose from that authorized list. Sorry, no bitcoins

It could be considered as an alternative asset. A vested benefit pension could allow an allocation of X% in bitcoin if a financial product exists (like a bitcoin ETF). Viac offer Gold and private equity.

However, a 100% allocation wouldn’t be aligned with this rule:

“3 When investing the assets, the pension fund must comply with the principle of appropriate risk diversification; in particular, the funds must be distributed among various investment categories, regions and economic sectors”

The pre-screened funds are chosen by the pension fund. There is not list.

My main issue is to find the data. In the CS factsheets the country breakdown is not always there, so I had to google it (for example I found emerging markets in teletrader.com with a bit of luck). Is there a good reference website to have country, industry split ect. instead of hoping it is in the factsheets?

How to find the market cap of the swiss indexes?

Also I’m not sure to understand fully the share class and some wording in the fund names. So here’s my newbie questions:

“Blue” means “Blue chips”? If not what does it mean?

“Z”?

“D”?

A indicate distributing share classes (source credit suisse, see below)

B indicates accumulating share classes (source credit suisse, see below)

H indicates for hedged share classes (source credit suisse, see below)

Source: All CSIF (CH) in Switzerland are licensed for distribution in Switzerland. All CSIF (Lux) and CSIF (IE) are licensed for distribution in the following countries: AT/CH/DE/ES/FR/UK/IT/LU/NL/SE/SG/LI/IE. The suffix “TR” after an index name stands for “total return” (gross dividends reinvested); “NR” stands for “net return” (net dividends reinvested). Q share classes are reserved to Qualified Investors, whereas the F and B share class can be subscribed by both qualified and private investors. Denominations containing the letter A indicate distributing share classes, the letter B indicates accumulating share classes. H indicates for hedged share classes. Source: Credit Suisse, as of 30.09.2020.

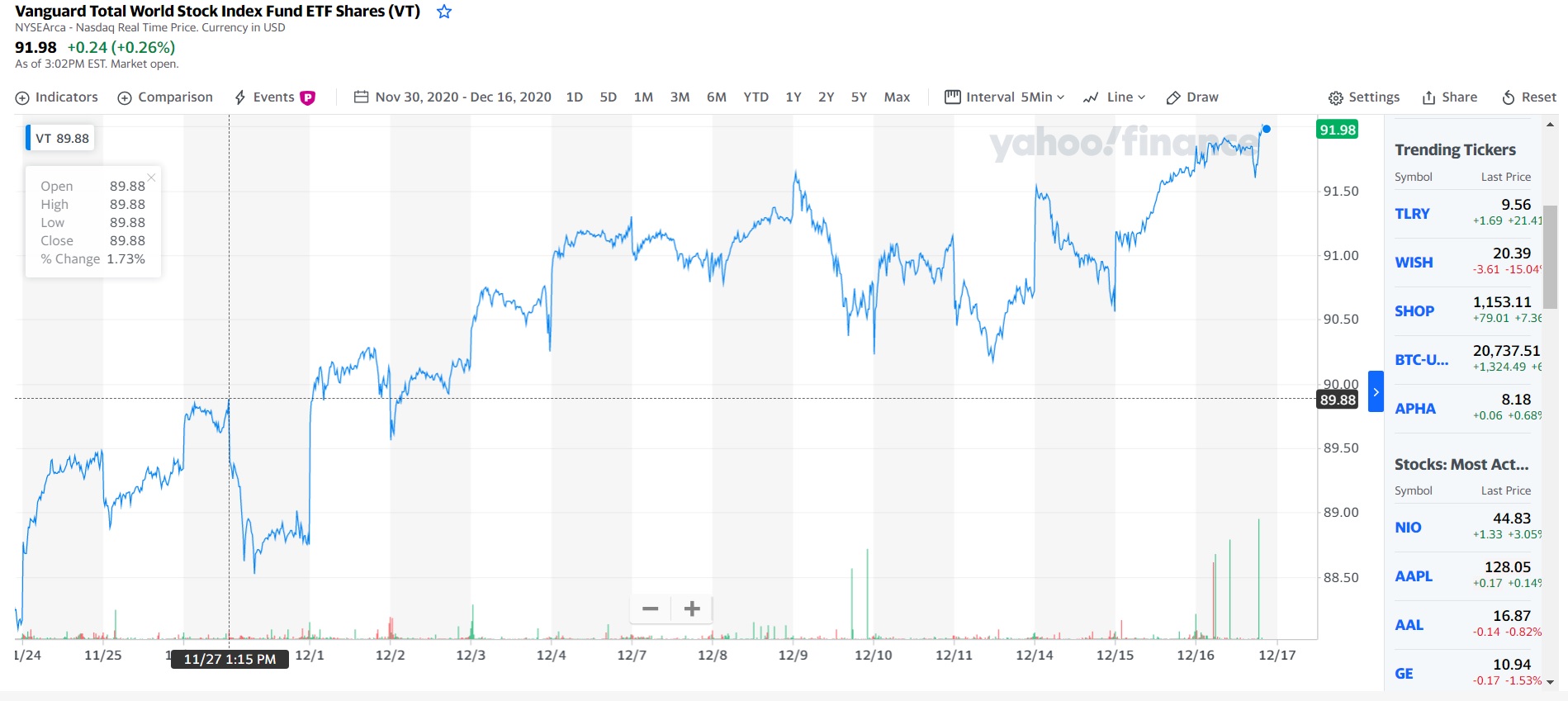

Thanks @Lonair and @MrLeanLife for sharing your spreadsheets. I have gone through them and both seem to be a good replication of Vanguard VT in terms of country allocation.

I had a (maybe rookie) question: even if the country allocation is the same, or very approximate, how certain can we be that the assets are the same as VT’s?

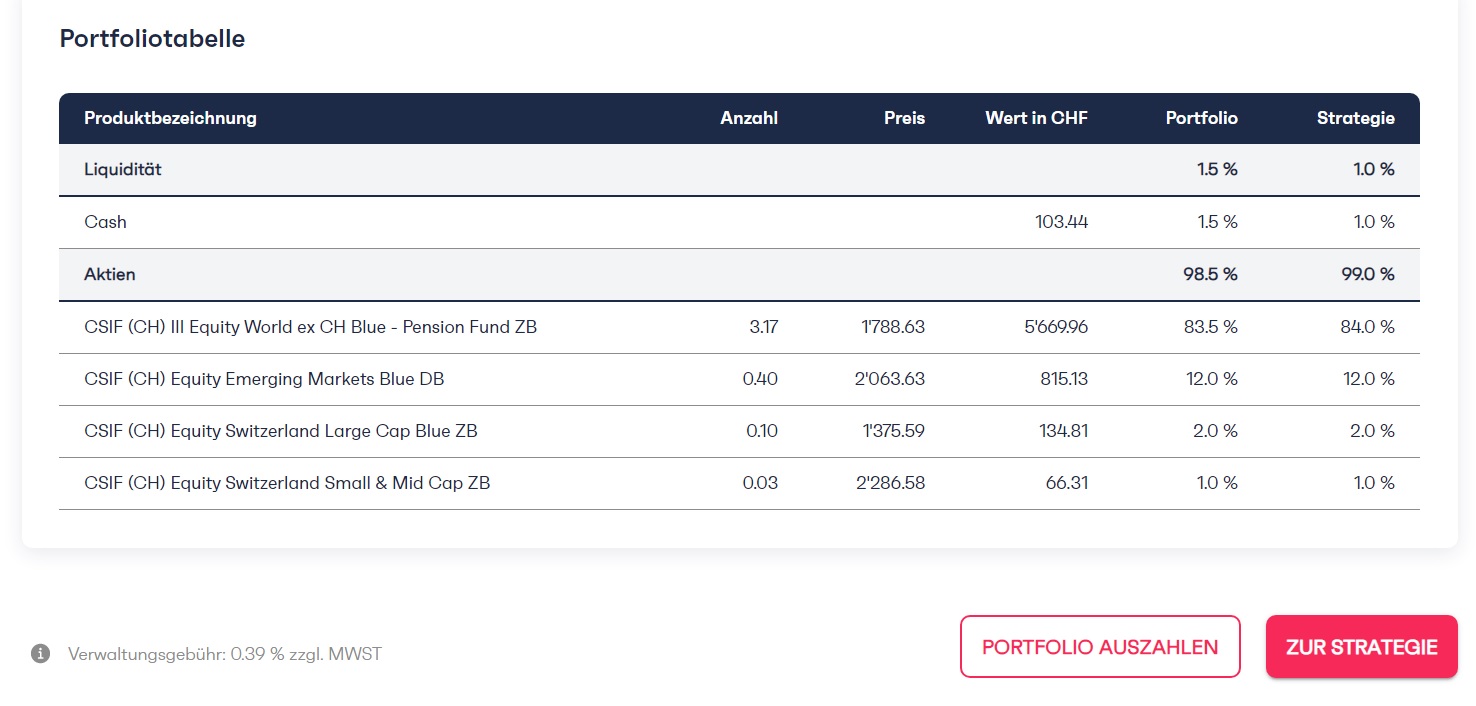

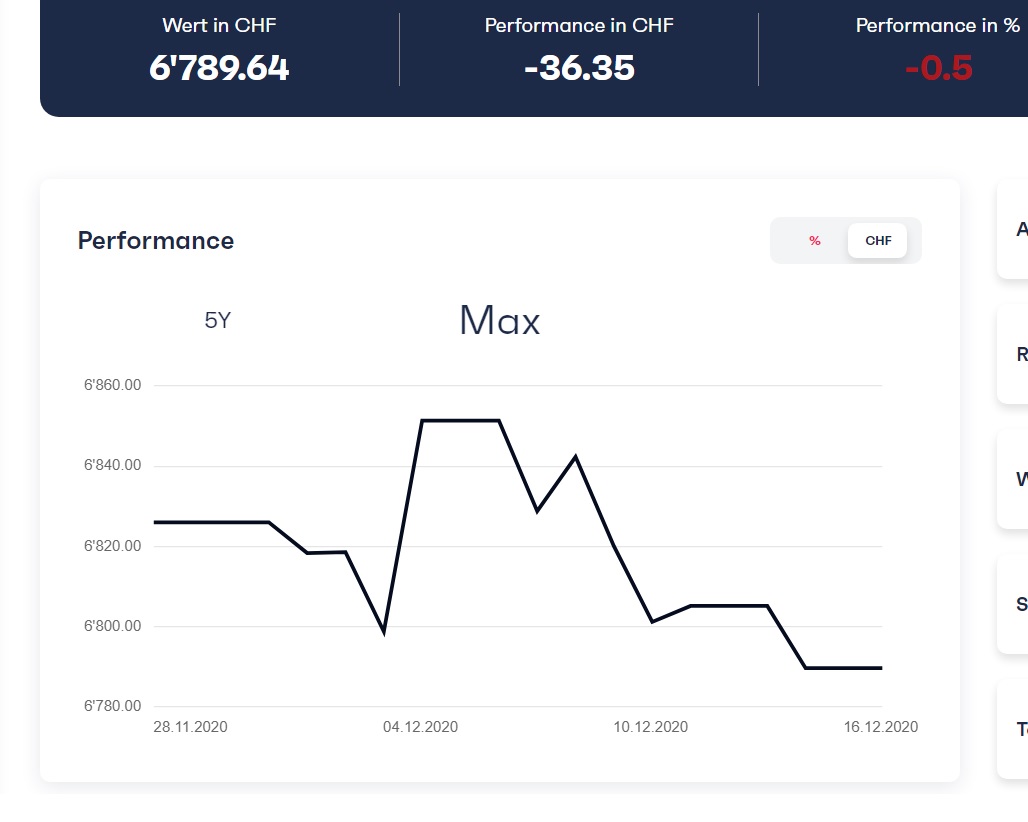

I opened a Portfolio at the end of November with this allocation (I guess the shares were first bought on the 30th):

We can see that the portfolio plot has highs and lows at points where the Vanguard VT hasn’t, or for example, taking the last 2-3 days, VT is rising while the portfolio has fallen. Also the “final” value (at Dec 16th) of VT is bigger than on the 30th of November, and not lower.

If the assets are the same, shouldn’t both plots be more similar or have a closer correlation?

still struggling between finpension or viac; based on that there is a big difference.

Is it determinated by something or what? double performance almost it’s a lot, especially for a month period.

thanks

Difference in what exactly?

You can create/choose pretty much the same performing portfolio in both.

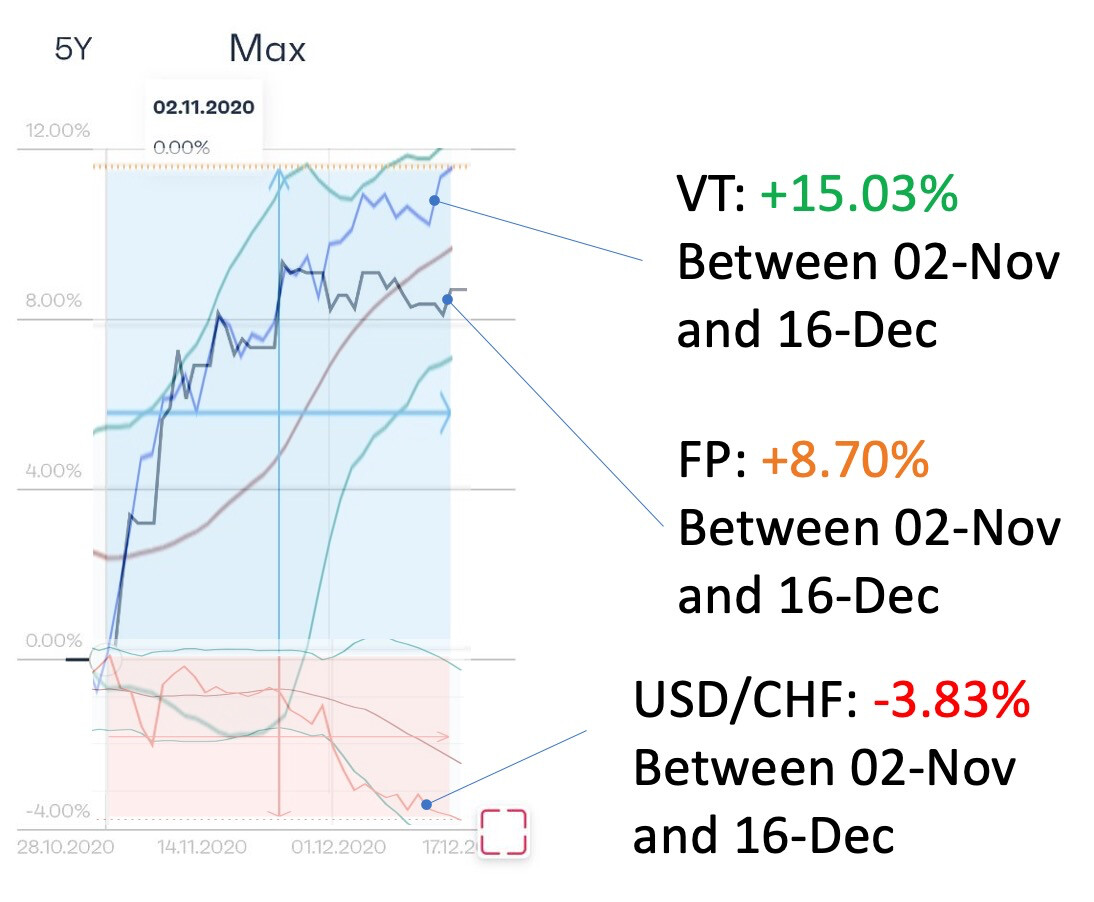

Maybe not 100%; but I suspect that you misinterpreted the VT in the above chart as VIAC - it is a Vanguard Total World ETF, not VIAC…

Hi guys, I just went for finpension and also tried do emulate VT in there, using @MrLeanLife approach:

84% CSIF (CH) III Equity World ex CH Blue - Pension Fund ZB

12% CSIF (CH) Equity Emerging Markets Blue DB

2% CSIF (CH) Equity Switzerland Large Cap Blue ZB

1% CSIF (CH) Equity Switzerland Small & Mid Cap ZB

1% Cash

I just wonder if it would make any sense to use the hedged version of the 84% one, since the Dollar seems to be getting weaker. What do you guys think?

Hedging is a losing strategy on the long term. The cost of hedging is pretty high and this will definitely hurt your portfolio’s performance.

On the other hand, on the short term, It can make sense to hedge if you want to bet on a specific movement of a currency pair. Personally, I find it pretty difficult to foresee in which direction currencies will go, so I wouldn’t play with hedging.

Hi @TeaCup , thanks for the hint! I am pretty new at this, so can you explain a bit more how exactly this will improve the returns (rather than trying to match the % of investment in each country from VT)?

My question will be a bit off-topic here but I was wondering on your statement above: does your statement also apply to US treasury bond ETFs? Would you also recommend not to take the hedged version of that ETF? or does your statement only apply for equity ETFs?

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.