Isn’t interest on all current accounts zero in CH?

As far as I know ZKb, UBS, Swissquote etc

Wherever we get interest , we need to have some duration risk. But FP can’t do that because they need cash all the time.

Isn’t interest on all current accounts zero in CH?

As far as I know ZKb, UBS, Swissquote etc

Wherever we get interest , we need to have some duration risk. But FP can’t do that because they need cash all the time.

I think I read an interview or something when someone from finpension mentioned that they are actually having operational difficulties holding all this cash, but can’t do anything about it.

Yeah for an investor it’s 1% of 1%, that’s negligible.

Sure, I was only responding to the “why hold cash” part.

Mate you’re in a FIRE forum, wars have started for less ![]()

Every penny counts!

I think you are talking about two different things

Indian Mutual fund investments for NRIs are taxed simply based on buy and sell price of mutual fund units. The capital gains is based on that. It’s not based on CGT that is triggered when mutual fund sells the underlying shares of companies.

However for Foreign funds or ETFs , the situation works a bit different. They always have to pay CGT when they sell underlying shares of companies.

Most likely since CSIF only charges at time of redemption , they should have a way to estimate this value. It’s not that difficult because they just need to know the CGT per unit at time of purchase and at time of redemption. Why they choose to assign a specific percentage to redeeming shareholders instead of actual value is not clear to me. Maybe they always want to benefit the remaining shareholders rather than leaving members

See article by Franklin which used a different approach and simply adjust NAV for the provisional CGT

I think for investor in the end impact is same because the principle is not changing. In one fund the NAV is already reduced and in other one the exit fees is accounting for that

So on average it should be fine. But the issue could be that for some individuals it might be negative . This could be particularly costs during rebalancing if transactions result in net outflow

In order to reduce this headache I simple excluded EM from my 3a and replaced it with US. I invest in EM using taxable accounts

I think if you check the value of EM fund , most likely it increase 7-8% since this discussion started. So the more you wait, the more impact to switch ![]()

Just a suggestion

If you want to minimise your redemption costs, my suggestion would be to do it on Monday which comes after the payday. Most likely during that week FP receives lot on incoming flows for 1E funds and that could mean that there isn’t really any redemption at fund level. They invest money on Tuesday for the funds that credited by Monday every week

Looks like they read your comment and took it personally:

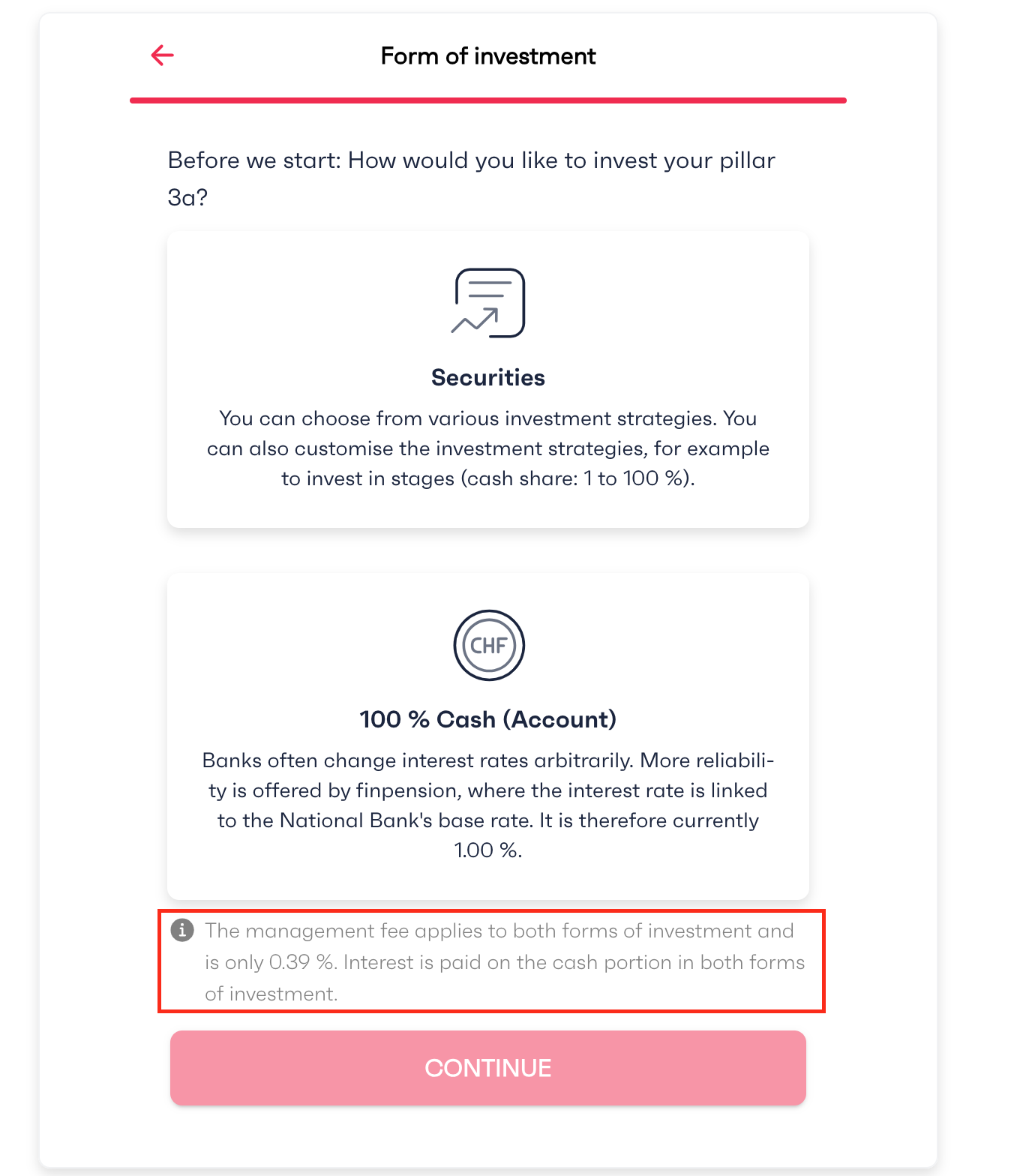

Just received the email from Finpension regarding the 100% cash account ![]()

Looks like they’re starting to reap the benefits of their (recent) FINMA authorisation as a securities firm (Wertpapierhaus).

Will you have the same offer for free assets? I.e. a “savings” account for taxable cash with SNB rate minus your management fee?

I’m not sure, but don’t you need a banking licence first? As @ skyw4lker mentioned, they are only licensed as a securities firm.

Wouldn’t that bring the interest to just about the same as a standard savings account with UBS, PostFinance etc?

A securities firm is allowed to hold cash accounts for clients when its connected to settling securities trades (art. 44 par. 2 FinIA). Thats of course not as broad as a banking licence. So there are limits in comparison to a banking licence, which is why they are also pursuing a full fledged banking licence.

It also says in the press statement that the cash accounts are held at regular banks (ie. licenced banks).

;

Great news! I can be pesky ![]()

Looks like its better*:

Seems very fair to me, well done. ![]()

*For 3a; other settings that you might have referred to could be different.

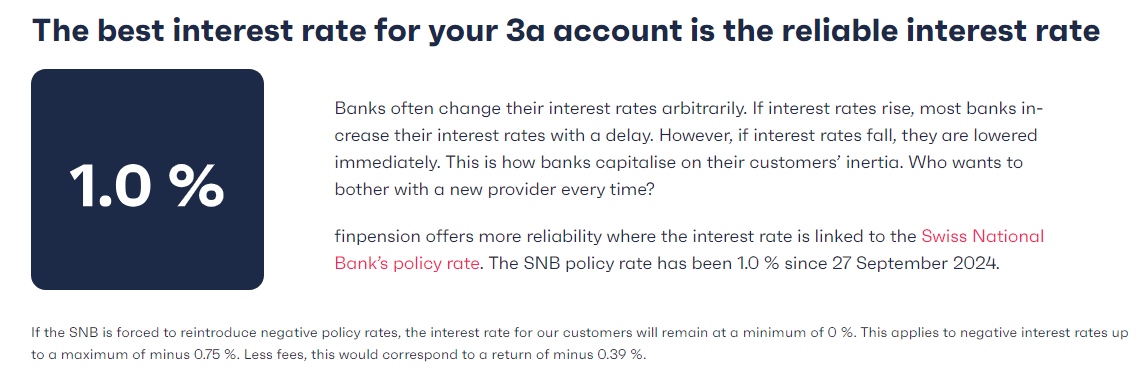

Is it just me who does not find this new offering particularly interesting? It just looks nice at a first glympse, but after I have read that they charge fees on cash, it is net (currently 0.61%) way lower than most banks / other 3a apps (Viac: 0.95%, Truewealth: 1.25%). At least Truewealth does not charge fees on it. Or do I miss something?

I think the difference is that they’re upfront about it and you know what to expect (rate will be SNB minus margin).

Most other banks/institutions often delay increases by large amounts of time (decreases by less time), overall it should be more predictable with a setup like finpension (similar to a money market fund).

(viac/truewealth will likely adjust their rates downward)

I expect remunerated cash (not 3a) to be always 100% available. And yes, I also don’t like and don’t have time to keep opening new bank accounts, and some people even less.