Good evening everyone,

I recently came to the realisation that the product I invested in through my 3a at Raiffeisen was very bad… I even lost some money because an employee told me that sell orders took 30 days to settle and it was done on 3… But it’s another story.

I am in the process of transfering my Raiffeisen 3a to finpension and I opened others 3a by VIAC and frankly (and I am looking for another provide because I don’t want to have more than 100k in the end by each account and to spread the risks) .

I am currently learning the different strategies they propose and I was wondering if you could tell me your advices on what I am thinking of doing (I don’t want to create my own strategy) ?

-

finpension: Switzerland 100 at UBS (13k will be transfered soon so I want a relatively stable strategy)

→ 0.39% fees and ??? TER/buy fees for the funds (I have a problem downloading the factsheets…, the text is not appearing in them)

-

VIAC: global 100

→ 0.41% internal and external fees

-

frankly: extreme 95 active at Swisscanto

→ 0.45% fees and 0.02% TER for the funds

-

yuh (maybe): stratégie “pimentée” but I am not sure because the chosen funds composing their products seem to have high TER fees. But if you have any other advice, I would gladly hear them, thanks.

→ 0.5% fees but pretty high TER/fees of external funds it seems

My global strategy may be too heavy in swiss stocks (Roche, Nestlé, etc) ; what do you think ?

Thank you very much I advance for your previous advices !

Do I understand correvtly that you currently have “only” 13k total in 3a that you are transferring to Finpension now? If yes, I wouldn’t think too much about spreading the risk and accounts into multiple providers at the moment and focus on the strategy you want to take at Finpension. Who knows in a few years there might be many other good providers available to choose from.

A good rule of thumb is to open a second account once you reach around 50k. Personally I have 50k at Finpension 99% invested in a fund tracking the MSCI Quality Index and around 20k at VIAC in Global 100. And I simply fill up the VIAC account until it reaches 50k and then I’ll check again where to open the next account. Try to find something simple and stick to it.

Regarding the question if your strategy is too heavy on Swiss stocks, you need to look at it from a global perspective, meaning considering your investments outside of 3a as well in your strategic asset allocation.

4 Likes

You may be overfocusing on fees. Focusing on recurring fees is generally sensible - but not much when you take it to tiny fractions of a percent, and comparing it across different strategies and funds.

99% quality

1 Like

You should take a look at TrueWealth 3a product. Seems to be a good candidate to me.

Thank you for your answer.

The reason I want to invest early in multiple 3a accounts is to take advantage of the diversification it will give me and benefit from different performances over the very long term.

Your remark about the outside investments is clever, thank you. I hadn’t think about it that way. I indeed invest in other markets and other funds outside that are absolutely not related to Switzerland.

Thank you for your answer.

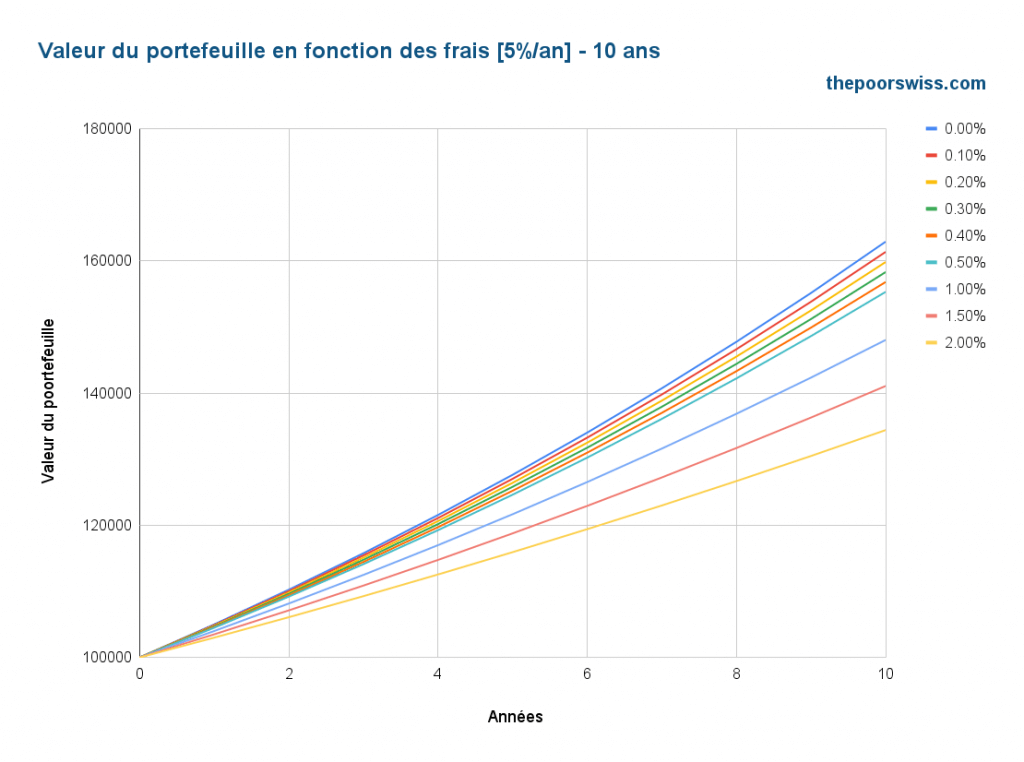

Actually fees can have a heavy impact on performance on long term: https://thepoorswiss.com/wp-content/uploads/2022/03/Valeur-du-portefeuille-en-fonction-des-frais-5_an-10-ans-1024x762.png

The reason I wanted to gather fees on those strategies is to have every information available to take an informed decision.

Looking at the numbers (that have been mentioned so far), we’re talking about a difference in cost of 0.11% or less . As the graph shows, that’s negligible.

Even after 10 years, it’s than the Japanese Nikkei index lost on (a rather normal) single day yesterday.

What advantage exactly are you talking about?

What is the benefit of different performances? The only strategy that brings a benefit is the one that performs best and this is impossible to know beforehand.

2 Likes

{kind=link}