A friend of mine works at this 2xIdeas company that creates funds aiming at delivering 100% return in 5-7 years. They basically follow the global MSCI ACWI Index (large and mid caps) and use a Warren Buffet style approach to identify the 400 best companies from the 4000 mid to large Cap companies. Then they select 100 stocks for the fund that should help outperform the index. Every quarter they review the fundamentals and tweak the allocations a bit. So far the (short) track record since looks good.

They transparently communicate why they do what and they are long only. They are fully aware of the fact that Tesla investors made a killing in 2020 and yet they believe in the long-term returns of solid companies. To me it sounds like the boring VTI/VWRL portfolio but better.

Why hang in there with companies who are past their prime when you can weed out the ones that don’t have what it takes and focus on the good ones in a way that offers the same risk profile as if you had invested in VTI/VWRL? 1% TER sound expensive to us but I kinda like the approach. They have outperformed the MSCI ACWI index by almost 9% for the last 6 years.

On the downside I think it is a bad time to get involved now. I feel the peak is approaching. And 1% TER is high. If these guys are confident in what they are doing, they would charge only 0.5% and take their margin whenever they do their over-performance magic. What do you think about it? Snake oil or real deal? 2Xideas Library Fund

This statement goes against the efficient market hypothesis. Investors want the highest risk-adjusted return for their capital. So an apparently “unsexy” company has a price that should reflect it. If these guys are not doing anything magical, but follow a few well known and publicly available indicators, then this should be priced in.

Their approach of starting with a full index and “weeding out” the worst companies actually sounds similar to Fundsmith, where they opt for a positive selection based on the indicators.

If you’re afraid of a coming crash, it’s the badly managed rotten eggs that will crash the most, so actually it would be a good time to invest in a fund that tries to weed them out.

That being said, I still don’t get it how such funds manage to beat the market. Why is it so easy? Or do they take more risk than the market average?

Interesting point, and I think I agree. Elon Musk, however, shares a different opinion and he said short selling is a vice disguised as a virtue. He also said short selling originated in the times when you knew your shares are coming on a different horse which is a few days away. So in order not to wait, you sold something you didn’t (yet) have on you. But today’s short selling can be used to bully a company into the ground (as was being done to TSLA in the past). Again, I think I don’t agree with him.

I’d say it’s common sense. We want the highest returns. There are millions of people analyzing stock market indicators, smart people writing algorithms that exploit market inefficiencies. You’d think the market would be efficient at least to a degree. Or that the inefficiencies are not consistent and easy to spot.

Yeah that’s very well put. That’s what comes to my mind when I see a chart, where fund X return looks like an amplified version of S&P 500. You can pocket higher returns for years until something totally unexpected happens.

Wouldn’t it be better to just identify the best company and skip the other 399? Diversification only makes sense if you can’t find the stock that will have the best performance, but as they think they can, why bother with more than one stock?

Why is a artificially high stock price a problem for us that needs to be solved by short sellers? I heard this argument a lot but I don’t understand it. If I think a stock is overvalued I just don’t buy it.

I totally get why people are short selling stocks, but do we as participants in the market or a society need it?

For me the main purpose of the stock market is to provide a exit strategy for investors and that companies can acquire new capital. As a side effect I can invest in businesses and that’s great, but a lot of the other stuff that evolved around this is imho just because of greed and hurts the economy more than it helps.

I think there aren’t incentives to figure out the mispricings otherwise. E.g. if you think something is a fraud or will fail, you can’t put your money where your mouth is, and it might encourage bubbles.

I guess 1 company might be all or nothing, and 100 companies might offer a risk profile that is more representative of the whole group of 4000 companies

Apparently the risk measure is pretty much like the whole index.

When I think about any group there is always a normal distribution of different traits. Company success is not like a random game of dice. It’s more like poker, where good players have a better chance of winning. Could even be like dart, where physics rule. Having a good product, a good business model, sizeable differentiation from competitors, loyal employees - it all contributes to success. Not a random game. It makes absolute sense to me to find a pattern in a group and split it in a preferred and non-preferred part. And revisiting the decision every quarter would help me to fix any issues my previous choice may have caused.

It might open a whole other lot of can of worms to talk about ESG. Well performing companies would not make the cut of the 2Xideas fund, if they are controversial, vice-oriented or contribute to global warming. Yet they are part of VTI/VWRL…

If you agree that an average Joe does not know any better about the price of any stock, then you would agree that buying any stock at its market price is as good an investment as the other, right? And weighting by market cap allocation is logical, it spares you rebalancing and it’s the most popular way. So why are you not convinced by VT/VWRL? I think you posted your concerns already, but without explanation.

Fundsmith has already sort of done that for you with the exception that they simply and only invest in the stocks they have selected and no indexes For large caps check the Fundsmith Equity Fund (Fund Factsheet | Fundsmith) and for small and mid-cap check Smithson Equity Fund (Fund Factsheet | Smithson).

Thank you both. Indeed, Fundsmith uses similar wording as 2Xideas: No Nonsense, No Shorting, No Market Timing, No Trading, Just a small number of high quality, resilient, global growth companies that are good value and which we intend to hold for a long time, and in which we invest our own money. Even the costs are +/- the same: TER 1.05%

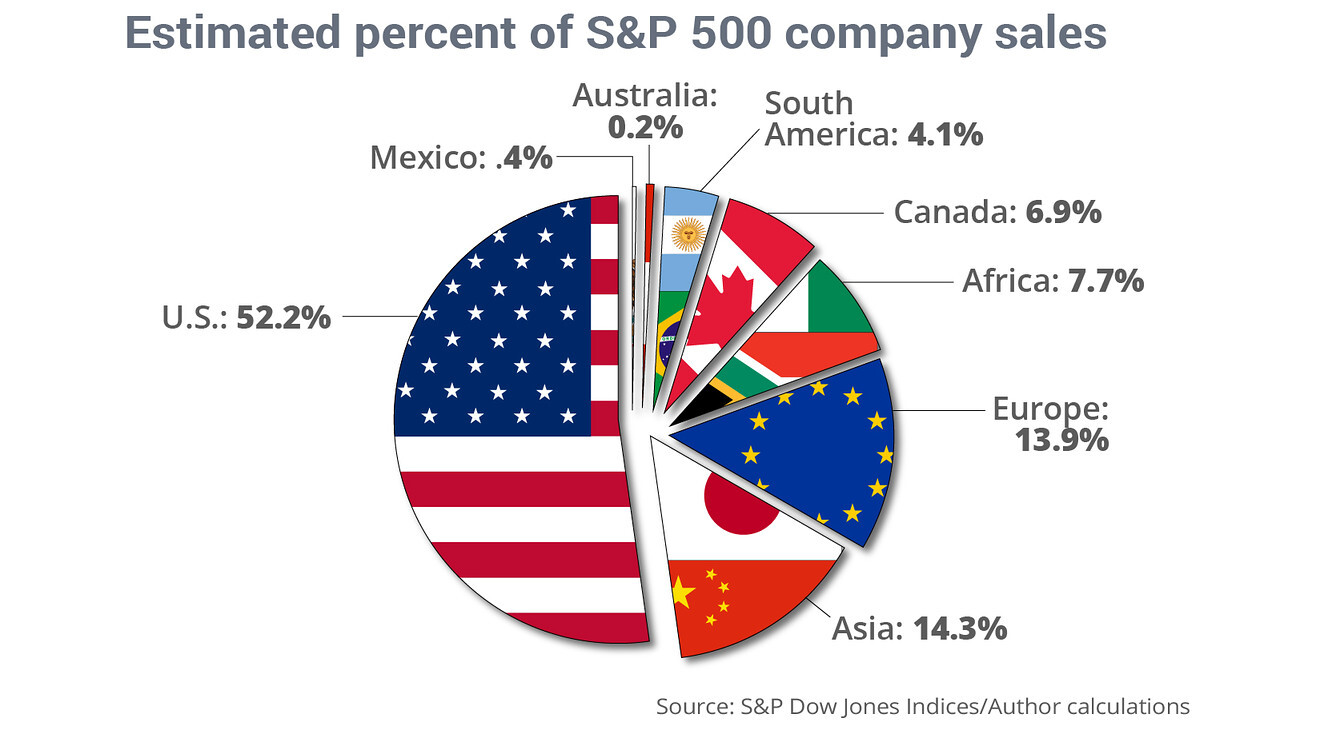

I guess the answer would be convenience. Also I think trans-national companies are often domiciled in USA, because it’s the largest stock market that grants them access to capital etc etc. They do a lot of business outside of USA, but the headquarters is in USA.

But would you agree that holding VT is not far from optimal? OK, a bit much USA, but it’s not like the risk is so bad. After all, these corporations could flee USA and change domicile. I don’t know how often it happens that a stock switches from NYSE to LSE, but for an ETF holder there wouldn’t be much difference, or?

This example comes to mind:

“In 2016, Allergan’s planned $152 billion merger with Pfizer fell apart after the Obama administration changed the tax rules to [make it more difficult for American companies] to lower their taxes by using mergers to shift their headquarters overseas. Since then, Allergan, an Irish company whose business is primarily in the United States, has been exploring either a sale or a split.”

This was blocked soon after another high-profile company moved outside USA or did something similar successfully (I don’t remember which one).

I guess there was fear that this would catch on & so the “concept” was “stopped”.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.