@bamboo has already given a good explanation. I would summarize the core point again: You get the discretionary (low) interest, because you will get that positive interest no matter the actual returns from the funds’ assets. Even in crisis years, you are entitled to this return (except that at some point the fund will need remediation measures, which usually would be temporary higher contributions for the same benefits)

However, you are mentioning your fund is offering different plans. That sounds like the newer “1e plans”, in which case you are fully entitled to the market returns (and risk) with your “Überobligatorisches Sparguthaben” (which is also why your fund likely does not publish a formal discretionary interest rate).

Thanks! There was something mentioned about 1e on the website. I will ask my boss. But the whole company has to take the same plan and I don’t believe I can convince my boss to take 50% stock. Only then the returns are at least not terrible.

@dom.swiss

May I ask where you found the info below. This is my case exactly and I can’t find any info on it. Much appreciated.

If ever returning to work in Switzerland, you will have to transfer “obligatorisch” amount from the “Freizügigkeitsstiftung” into your pension fund and you can again make annual voluntary contributions to top it up (edited: this works also in e.g. UK). Save again on income tax, potentially not paying much of it until retirement age if you play this game in your mid 50s.

I learnt since that much is a question of discussion/negotiation with the pension fund. As we may be talking about a bucket size that’s larger than the mandatory part, the pension funds are at liberty to make their own rules, as long as the mandatory part is managed according to federal law(s). Tell them what you would like to do and document their reaction here (I have not yet taken up new work myself )

The pension funds says buybacks are AOK. However, at the bottom it says that tax deductions depend on the (vaud) canton allowing it. I ve gotten three different answers form the canton. i) you need pay every thing you withdrew back (haha) ii) you can buy back up to 20% of your salary iii). It’s up to the pension. Problem is if the make a big buyback and it’s not accepted by tax authorities then you don’t get tax break and you can’t take the money out again until retirement or leaving CH ie hello 0.1% interest:)

Ahh, 3 opinions in 1 canton alone, 26 cantons in total… ZH tax department is quite relaxed in many regards but I will yet have to test them on substantial (50-100% of salary) successive annual pension fund buy-ins after age 50. Does anyone in this thread have practical experience with this?

Well, I actually had a lawyer to check this. There is nothing in legislation that says you cannot do the buybacks (of course the pension must approve first ). Tax authorities may try any say this is tax avoidance (manipulation, since you use the buybacks twice) in which case you may have try and negotiate and ultimately go back to a lawyer. But you should be able to do it. Lets see what happens in tax 2021!

Great thread. I am in the camp to buying into pillar 2a to lower taxes because 1) my time horizon to early retirement is 2-3 years, then travel and withdraw in tax friendly country and 2) yes pillar 2a is low return but also risk! I mentally view it as bonds ( which I deselected because tax advantage of pillar 2a)

One question to your sequence @swiss.com, why do you need to move to a foreign country right away once you quit your job? Could you not remain domiciled in CH, then once you have passed the 3 years lock-in you move to a foreign country that does not tax pension contributions? In fact, once you leave CH, does that not trigger automatic payot of the uberobligatorisch part of pillar 2a??

Using this old but related thread to post my topic/question.

Situation

Mid 40ies

A few years to FIRE (say 2 to 3). Will stay in CH after FIRE.

Currently relatively high marginal income tax rate (>30%)

Also relatively high Vermögenssteuer

In recent years pension fund/second pillar has compounded at lowly 1-2%, which I expect will stay the same for next years.

I will not need “free access” to the assets in my pension fund until 60-65 y.o.

Shall I buy into pension fund / second pillar now and in the other years till FIRE? It will be to the Zusatzvorsorge (which is the überobligatorisch as I understand)

After FIRE I would transfer my 2nd pillar funds to Viac and Finpension (their 2nd pillar solution is called Valuepension), one for the obligatorisch part, the other for überobligatorisch, to limit risk (a bit) and also to simplify withdrawal in seperate years. I would choose a relatively high % allocation in stocks (let’s say same as my approx stock allocation of total NW ~70-80%)

So

I believe (after FIRE) my money in second pillar will compound at approximately the same rate as out.

The lower compounding of my pension fund money is limited to 2-3 years (until I FIRE), thereafter the return is approximately equal to money outside my pension fund/pillar 2.

I have a significant tax saving now, much higher than a few percent p.a. x 3 years.

Would the heirs get the full amount paid out from what is in the Viac or Valuepension “pot”?

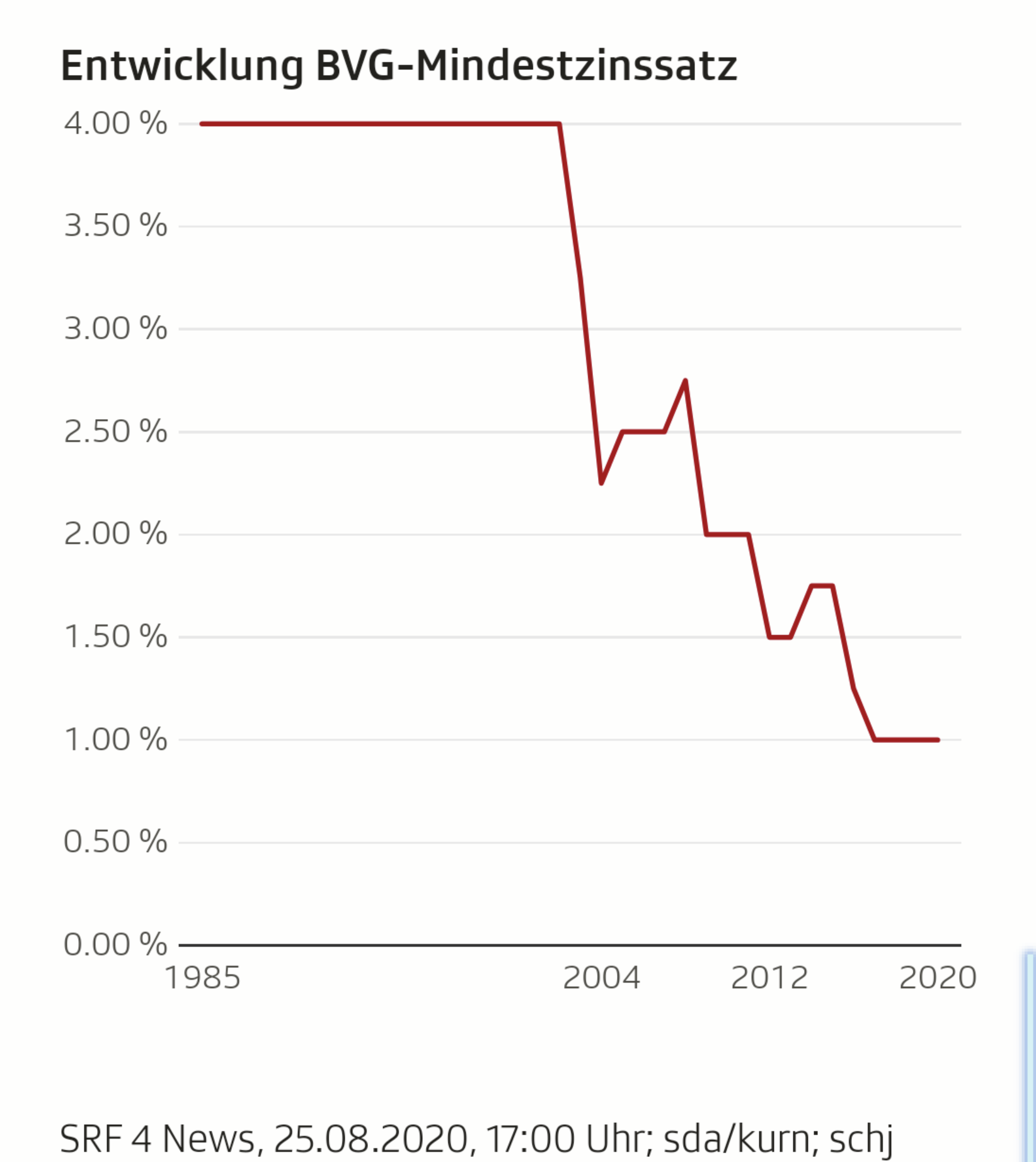

Mindestzins 2nd pillar is 1% currently, and has been for a few years.

Is my “über-obligatorisch” Zins in the past so “special” (table below), because this Zinssatz has always been same or higher than the Zins on my “obligatorisch”?

Is this uncommon? Else I can’t understand/follow @Grog & @nugget 's reasoning here.

Or am I missing something else?

2020 PK 1%, ZV >3%

2019 PK 2%, ZV >3%

2018 PK 1%, ZV 1%

2017 PK >2%, ZV >4%.

2016 PK >2%, ZV 3%

2015 PK & ZV same

2014 PK 3%, ZV 3%

(I’ve changed some actual values to “>X%” for anonymity reasons)

Increase the chances, yes (since it’s no longer under safe harbour rules), likely to be classified, still no otherwise we’d hear about a lot of retiree being professional trader

überobligatorisch assignments affect contributions to the pension fund above the CHF 86400 yearly salary threshold. As you have a high marginal tax rate I assume your salary is significantly above that. Meaning that a significant portion of pension contributions are assigned to the “überobligatorisch” part of your pension capital. I suspect that part is much larger than the “obligatorisch” part with you.

“Zusatzvorsorge” is not a standardized term. Pension funds use it in different ways.

The average interest rate of pension funds for pension capital over the last 11 years is 2.15%. That is for both obligatorisch and überobligatorisch combined.(source swisscanto)

Your PK values look like they roughly match this

Zusatzvorsorge in your case looks more like a 1e pension plan, where employees can invest themselves, but also take the risk. The higher return rates suggest it. Is that the case?

You also mentioned that you only expect the same returns after moving the money from the pension fund to viac, etc. The average performance rate of pension funds over the last 11 years is 4.34% (source swisscanto)

Hi and thank you @capmac for the informative answer , your response shows me that I am misunderstanding things about what is obligatorisch and what is über-obligatorisch and that what my PK calls “Pensionskasse” and "Zusatzvorsorge* is probably not equivalent to oblig and über-oblig respectively.

I didn’t know Zusatzvorsorge is not a standard term either.

I will try understand better how much of my pension money is currently in which pot, based on the PK documentation. And in which pot a buy-in would land.

Then my questions, if I still have any, will be more clear.

What I do know is, that I don’t have a 1e type plan. I’ve read about 1e in the documents, but I’m under the threshold for that.

But I’ll also try to find out why the interest in the ZV is regularly higher than in the Pensionskasse, I’ve wondered about that before.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.

)

)