my wife (mid 30s) will stop working around February of 2025 and will probably be self employed late 2025 after few months of break and I’m thinking about how to optimize her exit.

I am considering:

Buyback of her 2nd pillar (20k) to reduce the tax burden for this year (-7.5k in taxes)

Maybe another buyback (20k) in January 25 (-6k due to lower income)

Transfer her founds to the vested benefit account of FinPension and invest in a global equities fund there until retirement.

by my calculation, across 25 years (until pension), with a fixed 5% return of the fund, taking into consideration 0.49% costs for FP and 0.07% for VT, I would have

60k by investing 20k in Finpension

41k by investing 12.5k in VT

The buybacks seem a good approach and it doesn’t include the wealth tax reduction.

Am I missing something?

Does this seem a reasonable plan?

What would happen if she goes back to work? Does she need to transfer everything back to the employer’s fund? even if she works part time?

You need to think about following scenarios and then decide

if she goes back to work with employer, most likely she would be asked to move back all funds or lie about VB information. So you need to be sure what is probability of that happening

You need to also think about where exactly you will be located when you will retire. Because that would determine lumpsum withdrawal taxes from VB accounts

what if Swiss government increase the lumpsum tax? How sensitive is your optimisation against Withdrawal tax rate

By “buyback” I assume you mean buying further into her pillar II?

At any rate, when she quits, move her pillar II into two different vested benefit (VB) accounts. You can split them any which way you want, half half, 1/3 and 2/3, etc.

If she indeed doesn’t go back to work, you’re in totally fine legal territory and she can withdraw the two VB accounts in two different tax years, profiting from a lower progressive tax than if the entire sum in one VB account is withdrawn in one tax year.

If she goes back to work as an employee you can decide whether to move the money from both VB accounts or whether by the time you somehow forgot about one of them. That way you won’t even have to lie.

Note that you’ll have to live with the volatility of the funds in the VB account(s) as there is no downside protection as with pillar II. This has several effects, regardless of whether you do the “forget one” approach or not and I would carefully think about the asset allocation in the VB account(s):

if the market tanks after moving the money from pillar II to VB account(s) and doesn’t recover by the time she goes back to work as an employee, you’ll realize losses in the VB account(s) as there is no downside protection as with pillar II

if you take the two VB accounts approach with the intention of her “soon” – within, say, less than five years – going back to work as an employee and forgetting about one VB account, you can take more risk in the one you forget and probably want less risk in the one you don’t forget, protecting against downside in the shorter timeframe

I think you have not accounted for Lumpsum withdrawal taxes. Right?

20 x (1 + r) ^25 = 60 , if r = 4.51%

But you also will have to pay lumpsum tax at time of withdrawal. You should account for that and use the marginal rate.

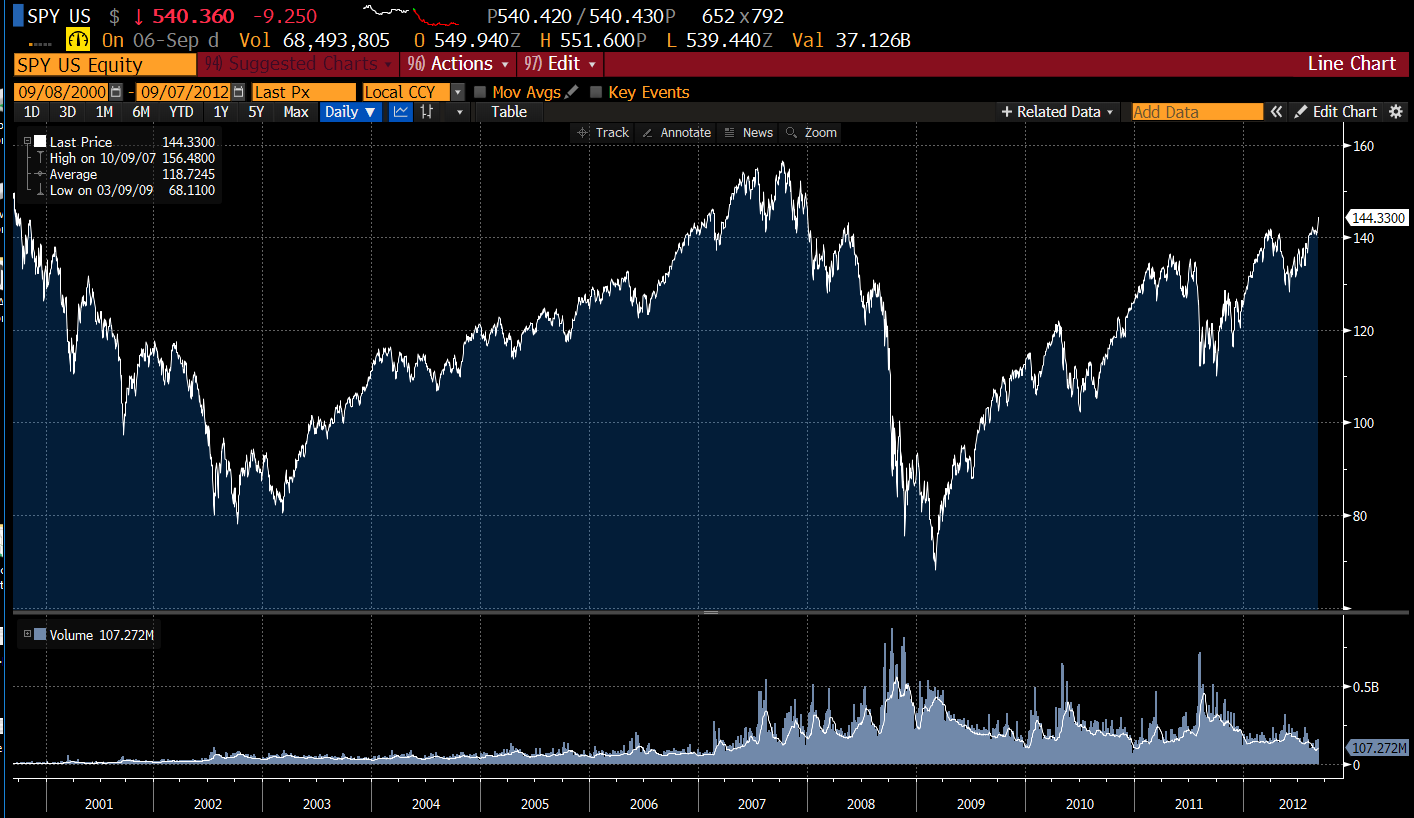

And you also have to account for the volatility risk in your VB account(s): if the market just entered it’s equivalent-to-2000 year by the time your 10 year withdrawal window starts, good luck with picking when you want to withdraw. E.g. the S&P 500 from 2000 to 2012:

You can only hope that the run-up until your potential first withdrawal year (60) was really nice.

Because it won’t really get better for the subsequent 10 years, but occasionally a lot worse.

However, if you take a 10’000 foot view, regardless of the nitty-gritty details discussed above, it seems obvious to me that with a long enough time horizon you can take quite a bit more risk in your VB accounts than your Pensionskasse ever can.

I generally dislike macro kind of views, but I’ll here spill some anyways:

As mentioned, in summary, you can take risk personally in your VB accounts that the Pensionskasse just cannot because it has obligations that you don’t have.

Some of these obligations:

the Pensionskasse needs to manage monthly cash flow needs of others over your investment horizon of 20 years

not only do they need to satisfy those cash flows needs, but a portion (the “obligatory” part) has fixed conversion returns (“Umwandlungssatz”) – currently 6.8% – determined by politics regardless of your fund’s returns* or market returns at the time of those fixed payouts

the Pensionskasse also needs to provide a guaranteed positive total return of currently 1.25% on your contributions (while you’re still contributing) – again for the obligatory part – determined by politics, regardless of your fund’s or the market’s returns*

Note that your guaranteed return is always positive – regardless whether it’s 2008 or 2020 or 2022

the Pensionskasse needs to be flush with cash for those who choose lumpsum payout – again, regardless of market highs or market lows

All these constraints don’t really matter to you if your pillar II type money is in a VB account and your time horizon is 10+ years (modulo your volatility risk at withdrawal time).

You can take more risk and get potentially more return with a VB account, but don’t ignore the higher volatility risk (or adjust your allocations the closer you get to withdrawal time)?

* The Pensionskasse can compensate for that by providing lower returns on the überobligatorisch part of the insureds’ capital, but they still have somewhat fixed cash outflows every month.

In worst case, one can still withdraw and reinvest in same scheme in taxable account. It would only mean that lumpsum tax would be low.

Let’s say VB was invested in MSCI world. And it tanked by 20% just two days before the withdrawal. Value before crash was X.

Following should apply

Pay lumpsum tax on (X- 20%)

Reinvest in MSCi world

Wait till it recovers

Now, the key problems that can occur are

if the process of selling and buying is a lengthy process and many weeks / months are lost.

This doesn’t change the fact that equity investment is volatile and one needs to be careful and always willing to keep the money invested for rolling 5-10 years at all times.

… but I would say the … ahem, worser worst case – worstest? – is when you ~immediately need to start consuming from that money you withdrew at the time you withdrew?

Certainly not how I would plan for things to pan out, but it’s always hard to plan for things in the future, especially if they’re a couple of decades in the future.

Don’t think it matters that much, if the returns in VB and taxable accounts are similar. Taxes and compounding are both a multiplication over the initial amount and those are commutative.

I think point-in-time this is true, but over longer periods of time compounding also works wonders in negative ways – taxes, fees – that might surprise you, even if the differences seem small (say, a 1% fee, or, in case of taxes, a lot of percent taxes on income or even a few bips on wealth).

But taxes would have been higher if market didn’t crash. So actually it’s not really a loss.

Let’s say VB before crash was 100K

After crash it’s 80K

Lumpsum tax 10%

You pay 8K tax instead of 10K which would have been applicable if market didn’t crash. You invest 72K back into MSCI world and wait for it to go to 90K to break even.

In both cases you would need 25% increase in market to break even

80K to 100K

72K to 90K

Yes, it would be beneficial for a crash before withdrawal. Imagine you have a 1’000k retirement account. We have a 1929 style crash that takes it to 200k.

You withdraw and pay tax on only 200k (say zero) and stick the amount into a taxable account. It recovers back to 1’000k and you end up with 1’000k in a taxable account in the end!

That’s plenty of time for a new retiree to start to draw down on depressed assets and not participate fully in the recovery. If such a crash happens not at retirement but a few years before, chances are we’d loose our job/our clients too and be forced to retire early with less assets than desired and them at a depressed level.

Of course, this is a matter of global allocation and not 2nd pillar specifically. I just thought it beared reminding as we joyfully consider that crashes just before retirement are something to look forward to.

Indeed I missed the withdrawal tax, that would increase taxes by 3700.- on a 60k increase in capital assuming that I keep living where I am and 4500.- if I move abroad (assuming not splitting the withdrawal across multiple years).

That would make Finpension 56-55k vs 41k in VT. Still a considerable difference.

Regarding the risks of market tanking before the withdrawal, that would be a benefit from a tax perspective, should probably be reinvested as soon as received and should be treated as part of the overall planning before retirement. I hope that these 60k will be a small part of the overall portfolio in 25 years.

Currently I see the employer 2nd pillar as “bond equivalent” safe assets (that I can’t withdraw), if they are invested in stocks in a VB account, I would as well need to re-evaluate my risk tolerance and potentially increase my allocation to safe assets. Maybe buying in my 2nd pillar

I think that the highest risk is indeed if she goes back as an employee, especially after a market drop as we would be forced to “sell stocks to buy bonds” when the opposite would be preferrable. This is something difficult to foresee, especially since she has no experience as self employed.

I will need to discuss further with her and evaluate all this but the inputs have been really valuable. I still have few months to think it through.

I have a related question on not being employed immediately before retirement (i.e accessing Pillar 2 funds).

It seems to me that if you move your funds to a vested benefit account (and hence away from your employer’s Pillar 2 provider), you non longer have the ability to chose a lifetime annuity and hence would also lose access to the higher annuity conversion rate applicable to the ‘unterobligatorish’ element of the fund? I assume this is the case since I do not expect the providers of these vested benefit accounts to provide lifetime annuities.

Personally, I would like to take some of my Pillar 2 fund and purchase an annuity (especially the MANDATORY part) so as to cover my basic monthly outgoings. I expect that to have this option, I would need to be employed (and hence part of my employer’s Saule 2 foundation) to be able to do this? This would therefore probably prevent me from leaving the workforce a few years before normal retirement and living off other savings.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.