I am not saying you should squander money but it would be a bit of shame if you built all this wealth and then didn’t really use it . Isn’t it ?

1 Like

I guess you need to consider it a bit like insurance or an emergency fund. These you pay or have on the side and is in effect ‘wasted’ but you need it to take care of emergencies or other contingencies.

So building up a big retirement fund to take care of longevity risks is the same. Though I guess you could take other routes such as buying an annuity. But maybe you’d also consider that wasteful if you die early or because you can’t pass any of the funds to your kids.

1 Like

Probably not very helpful to most of you but I’ll still offer my perspective.

It would be gut wrenching to experience that 50% drawdown in price.

For augmented drama imagine that this drawdown happens in the first couple of years of your retirement, let alone your first year … (“dear former boss, can I please have my job back? Pretty please?!?”).

I know backtesting suggests things will turn out fine (most of the time …) but I’m personally psychologically not wired for handling this.*

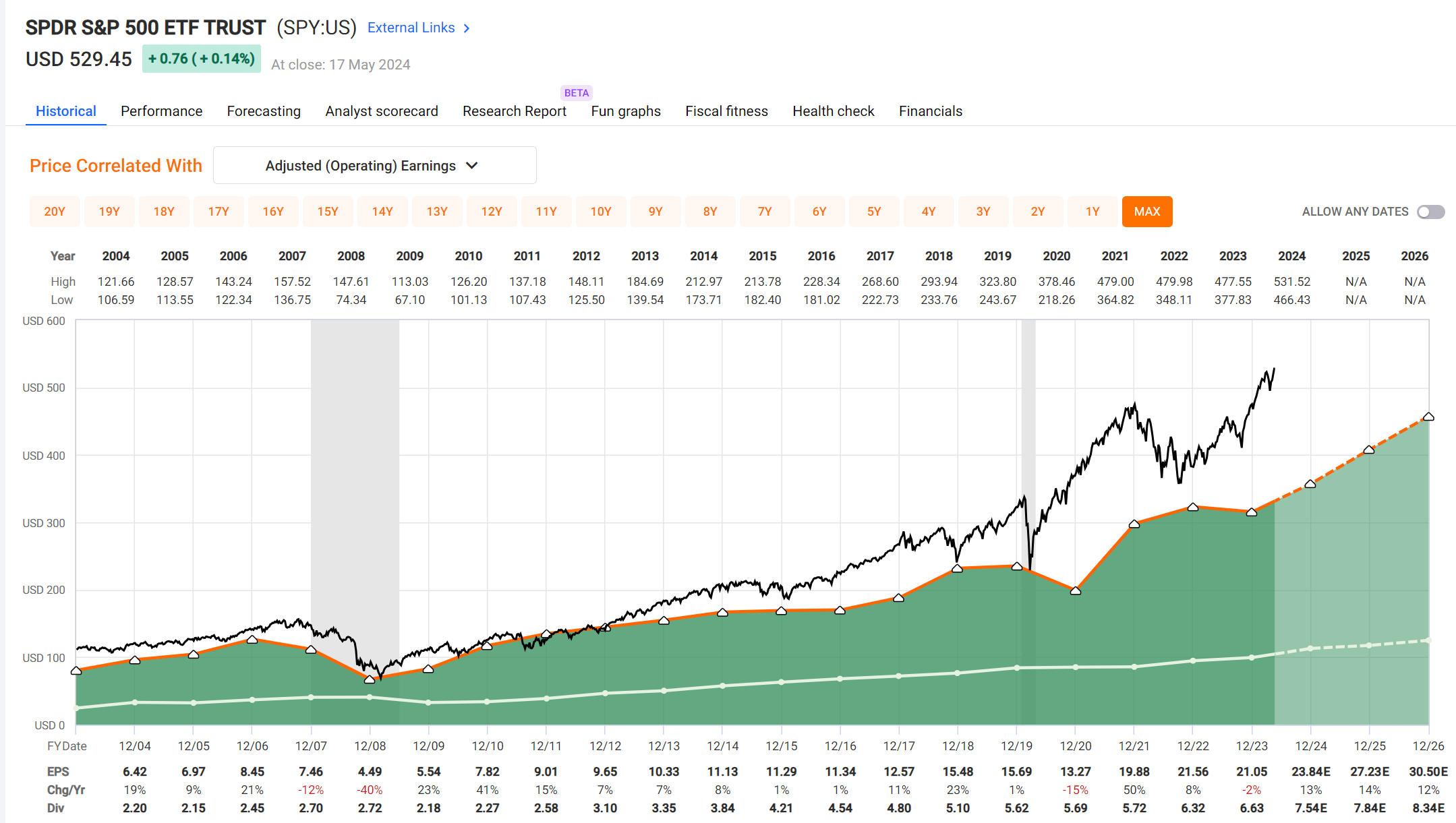

However, I only partially agree with your thesis that dividend cuts are in the 20-30% lower range for such an extended period. Even the S&P 500 handled things mostly fine from a dividend perspective (SPY: 20% dividend cut in 2009 followed by a 4% dividend raise in 2010. Looking at the most recent recession (and S&P 500 price drawdown) in 2020, there was no drawdown at all in dividends. So, steadily growing dividends for the past 20 years or so:

)

This is exactly why I’m pursuing my strategy of mainly living off the cash flow returns from my assets. Those are much more steady than price.

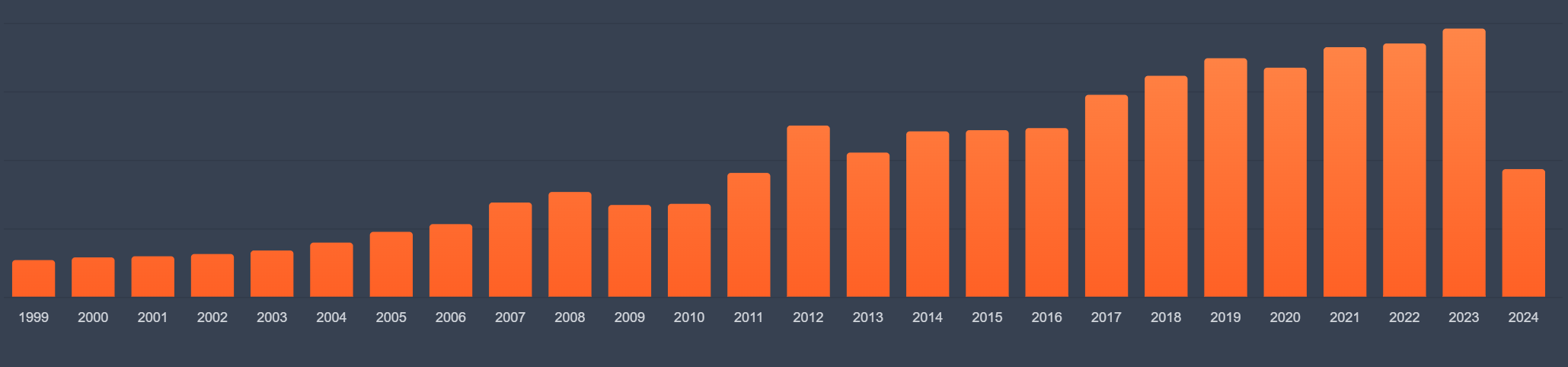

If I had bought my entire portfolio in 1999, this is what my cash flows from the portfolio would look like:

Three drawdowns in cash flows from this portfolio:

-

-12% in 2009

Great Financial Crisis (GFC).

S&P 500 retreated 50%. -

-16% in 2013

This is actually only technically a drawdown: it’s explained by the Capital Southwest Corp (CSWC) position in my portfolio. They paid out a special dividend in 2012 (which is why the total dividend income grew 38% for the entire portfolio compared to 2011). CSWC went back to their normal dividend in 2013.**

Without the special CSWC dividend the total 2012 portfolio payout would be in between 2011 and 2013’s portfolio cashflow. -

-4% in 2020

Pandemic.

S&P 500 retreated a little over 30%.

Psychologically, I’m able to deal with such occasional income drawdowns. A 12% income drawdown like in 2009 would still feel annoying, but it wouldn’t wake up my lizard brain. Maybe cut on planned vacations that year, make your coffee at home, curse a bit but actually mostly comfortably just deal with it?

I’m assuming you are asking which asset classes do you hold as a retiree (versus, which asset classes do you hold as the market tanks 50%***).

To quote Jason Zweig:****

To make my answer more concrete:

- I would initially keep my portfolio composition as it is now (or slightly before retirement).

- I would gradually reduce risk as I grow older:

- across asset classes I would shift from stocks to bonds (assuming bonds will keep returning acceptable returns and not go back to ~0% real returns as since the GFC until recently).

- within asset classes I would shift towards less risky positions

- buy government bonds instead of (ETFs of) corporate bonds

- buy US government bonds instead of (ETFs of) emerging market government bonds

- buy lower yield or slower growing but very steadily growing dividend growth stocks instead higher yield but more uncertain dividend growth stocks*****

* While I did buy a large position in VOO in March 2020 near it’s bottom, I was able to do this (psychologically) because I still had a steady work income stream, and the rational argument by my cerebral cortex that markets will recover won over my doubts, even as it was still not an easy decision.

I cannot imagine myself doing the same thing — or a similar thing, like moving out of my bonds and into VOO — when I’m retired and the market just tanked 30% over the course of a month or so. My retired lizard brain would tell my slow thinking rational brain (which still believes that markets will recover) to move over.

(and to be clear: rebalancing from bonds to stocks would be exactly the right move the next time this happens, my slow thinking part of the brain insists on me stating this here while the lizard brain seems fast asleep currently)

** CSWC 2011 dividend: 7 cents per share.

2012: USD 1.94 per share

2013: back to 7 cents per share.

*** To which my answer would be: the same assets as before the market tanked. Since I don’t know when the market tanks 50%, I need my portfolio be in the shape I need it to be if the market actually tanks 50%.

**** This is The First Commandment in Zason Zweig’s The Little Book of Safe Money: How to Conquer Killer Markets, Con Artists, and Yourself.

This is my goto book I give to people who are completely new to investing.

It would also suit many people who feel they are experienced investors.

***** E.g. buy Amgen, Cigna, Coca Cola or Johnson & Johnson instead of buying Bristol Myers Squibb, Capital Southwest Corp, or Legal & General Group Plc.

4 Likes

Exactly this. It is one thing to know what to do, it is another thing to actually do it during armageddon.

Well, this is an interesting chart! Thank you for posting it.

I genuinely wonder if post WWII dividend payout volatility smoothing out is coincidence or whether this is has just been an exceptionally steady dividend payout period in the grand scheme of things (of people looking back at this graph in a thousand years and in mundane economist cocktail conversations they will point at 1980 to 2024 as the one off steady dividend payoff period, an anomaly for a millenium).

Mathematical economists will seek to explain this in hindsight, maybe even Nobel prizes will be awarded over this … ![]()

I would not know either way, though I remain optimistic as a general principle.

My personal lesson is that the hammer I used for this job — FastGraphs — only provides a 20 year backward looking view, which seems … well, it’s within a 40 year trend or so, but going back further, things look at lot messier.

The most messy periods seem WW related, though?

Ah, sorry, I’ve posted about this before in this forum and I feel a little shy reposting it.

Stockpicking portfolio, which is about 3/4 of my pillar I portfolio, which is about 2/3 of all my pillars (I+II+III).

Pillar II is 1/3 invested with my current employer, so downward protected but only growing at 1%, the other 2/3 were, ahem, forgotten in a Freizügigkeitskonto. The assets in the Freizügikeitskonto only just this year made a positive overall return over the past few years. Pillar 3 is very conservatively invested with probably negative real returns over the past few years.

I don’t think there exists a general “formula”.

My personal guidelines would be (if this sounds like investing 101 that’s exactly what it is):

- closely observe your incoming cash flow, see if covers your needs (aka expenses).

- in the hopefully occurring case of income exceeding your expenses

- invest your additional surplus income in reasonable investments

– fin –

1 Like

I’m not too concerned about dividend safety. Sure, in exceptional years such as during covid, you might have a high number of dividend cuts or suspensions.

If you really want to cover part of the income, I guess you could have bonds to ensure some level of income and/or to draw down on to ride out these bumps.

3 Likes

That’s a good strategy to end up wealthier over time. Heuristic: (actual) inflation-adjusted fortune grows when you spend 4/3rds of dividend yield, alternatively 2/3rds of earnings yield.

1 Like

I guess if you wanted to keep it simple/automatic, then maybe this could work:

2 years of expenditure in high interest, t-bill equivalent, MM funds, bonds. you draw from this to spend.

then dividends from the invested 100% stock portfolio pays into this spending fund. i suspect with a 2% withdrawal rate, the spend fund will never run dry.

a variation to avoid having to deal with bonds or low interest is to have a mortgage and have the funds pay into a current account mortgage to offset against the mortgage. then you run a small mortgage with a view to maintaining a near net zero balance.

2 Likes

Always having 2 years in cash would cause a significant cash drag over time.

I’d say that 4% of the pot is ‘insignificant’. With a CAM, you even eliminate that to a degree.