I’m curious about your opinion on following. Let’s assume that the person is young enough and/or very risk tolerant and just wants to keep 100% of the portfolio in stocks.

That would imply no need for rebalancing. Which can be simply described as: selling a bit of the instruments which went up recently, to buy a bit of the instruments which were performing worse - in order to restore proper balance in portfolio. Do you think that such strategy would be worse, because of that, taking into considerations possible gains of rebalancing that way?

Rebalancing is not necessarily with stocks and bonds (I guess that‘s what you are refering to, as per the classic asset allocation).

You can have different allocation for stocks to rebalance also. I.e. split VT into its regions (VtI + VXUS for example). Or any other asset allocation stocks/bonds/gold/crypto/whatever.

Other than that: Of course 100% stocks is fine. Most people on the forum probably are.

And 100% stocks is very likely to beat any kind of stock/bond allocation (with rebalancing).

Bonds can serve various purposes, i.e. drawdown protection. More relevant closer to retirement (sequence of return risk for example)

If total return is the only thing relevant for you 100% stocks is sensible.

We need a bit more info on what your intentions are.

Well, I would say that among the classic asset classes (sorry!), stocks have a highest expected return. We are not talking crypto . If you have 20+ years to wait, 100% stocks is an excellent idea.

What is usually meant with a “rebalancing premium” is a higher return comparing to the same allocation, but without rebalancing. I would say it’s a second order effect. The long term investment returns are primarily driven by the percentage of stocks that are in the portfolio - and a capability not to panic sell if they tank by 30%. Everything else is diversifiers.

In this sense, even 80/20 with rebalancing will never produce more return than 100% stocks.

To give you a bit of a background. I’m on this forum since several years and I’m very grateful for all the knowledge and help . However, before I was not investing much (apart from small speculations here and there), because we were saving money for buying a house and doing (big) renovation. Of course, from hindsight, that was a mistake, as I would be much better with investing that money into some Global ETFs and we could have smaller mortgage at the end… but I was not doing it from obvious reasons.

Now, as our house-related project is finished (OK, spending on it will never be finished hehe), since about a year, I have finally started to invest monthly. So far it is very simple - I just buy VWRL. But here is where the question about rebalancing advantages pops out.

OK, I also buy some crypto (monthly too), but I’m not sure if it should be included as part of my long-term portfolio… I guess I’m fine to cash out some gains and move to VWRL, but I won’t be comfortable in cashing out VWRL and moving it back to crypto after it drops. Finally, I have some additional money in ZGLD, GDXJ, ZSIL and URNU, but these are mostly remnants of “old” investments. I will probably include ZGLD as part of my portfolio with the weight of 10-15%, which means I’ll be able to rebalance between ZGLD and VWRL, but I wanted to get your opinion about not rebalancing at all (eg. by being 100% in one ETF).

Sounds good! Of course putting all the concerns about being 100% in stocks and not panicking while drawdowns aside, especially if portfolio grows big (for a given person).

It‘s super fine to go 100% stocks with any new investments from now on, without rebalancing anything.

I‘d still buy stocks, by selling your other assets, in a big drawdown though (say 30%). If stocks are on sale and you have some drypowder laying around I‘d use it. If you otherwise have no rebalancing schedule.

But again, just investing in a world fund from now on and letting that run is super fine, with the caveats that were already discussed.

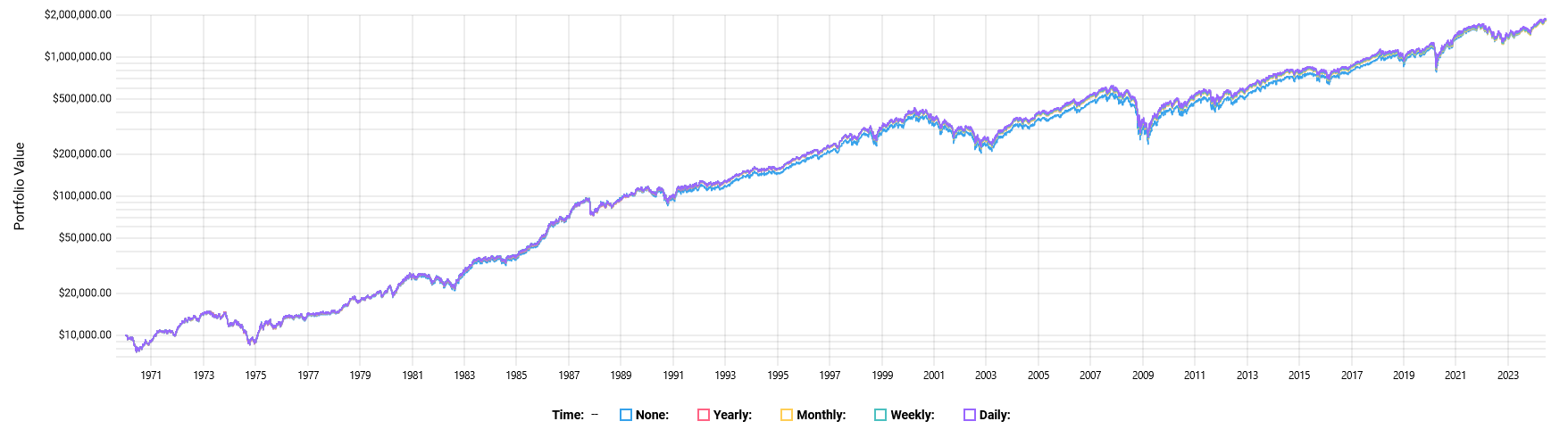

Representative of what rebalancing does, I made 3 graphs with testfol.io. I use simulated assets since there are no ETFs in 1885. This does not change the qualitative result.

Each graph covers one case with one allocation:

#

correlation

return

asset1

asset2

1

correlated

similar

60% VTITR (US stocks)

40% VXUSX (ex-US stocks)

2

uncorrelated

similar

50% VTSIM (all stocks)

50% KMLMX (a managed futures strategy)

3

(uncorrelated)

different

50% SPYTR (US large cap stocks)

50% CASHX (3 month US treasury)

Each graph has 5 portfolios. They only differ in their rebalancing frequency, which in order is: None, Yearly, Monthly, Weekly, Daily

Rebalancing lowers your return, but also lowers volatility and draw downs. High frequency is not that important and can make it worse. With no rebalancing the final allocation is mainly the high returning asset.

Nice assessment, I’ve done similar for fun. It’s a pity the third generation usually destroys any accumulated wealth, otherwise someone with long-term commitment could, in theory - build gazillions of wealth over time. Also the really deep rich families etc who have generational wealth for centuries have it tied up in depreciating/illiquid assets/castles etc.

I like to remember a comic episode where Scrooge McDuck laments that his profit is inexplicably dwindling. They find that the problem is that he already has all the money there is and is earning it faster than it’s being produced. I can’t remember how they solved the problem in the end, though.

Rebalancing is mainly applicable if you want to keep your assets diversified amongst asset classes or regional allocation

If you buy 100% VWRL then it would automatically keep rebalance itself to match global market weight cap.

So if you want 100% stocks then you obviously don’t care about asset class (bonds, real estate, gold, commodities, crypto etc) diversification and hence you don’t need to worry about rebalancing anything as long as market weighted stock allocation is fine for you

Only point I think you should keep in mind is that Stocks are best performing asset class based on history. And since they are considered more risky, they also tend to deliver premium returns. But this is theory , real life can be different . So just be mentally prepared for that. And all is good

Damn you voice of reason! Yeah, you make a good point though.

Though it’s still an interesting thought experiment, I think CSSPX had about 50bn when I first bought it, now I see it’s at 78bn. How the scheisse did it grow so much? Is this all retail?

I read somewhere about a neighbour of Buffett, he put 10k with Buffett in 1965 and never sold, that’s worth 165mn today (10k in 1965 was probably the cost of a small house in Nebraska…). Sounds so surreal yet the numbers check out. The anomaly is BRK, a compounding machine, given index funds are a fairly (50 years) recent thing, I guess there weren’t opportunities for low risk compounding over a very long period of time in the past. If index funds continue existing there’s no reason this couldn’t be done.

I’d also wager that some of the deep wealth rich would drop a lot more coins if turned upside down than Bezos, Gates etc who have their fortunes tied to single stocks.

I plan to leave some securities to my kids and tell them to basically never touch them until I’m dust.

Even close to a retirement, if you are flexible with the point in time, when you rebuild your portfolio from the accumulating to the spending mode, an allocation close to 100% might be a good idea. If things go not exactly like you want, you just need to wait, but there is a big chance that you will come ahead of a less aggressive allocation.

Sure, this means that my main “asset” is the mortgage . Jokes apart, I’m including it in my net worth of course, but for portfolio considerations, I tend to think only about financial instruments.

If you have a mortgage and if you want to change your asset allocation and reduce risk I think one of the most effective ways is to pay down some debt.

Holding cash or bonds would imply funding the banks’ spread. Holding gold whilst being leveraged does not seem attractive either

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.