This this my first time posting here, hope I’m doing things properly. If not, please correct me.

My wife and I recently bought an appartement with a CHF 700’000 mortgage at 1.65% 10 yr fixed rate, indirect amortization through 3a. We have made a 10 yr investment plan to get some cash available when we’ll have to renegotiate our mortgage.

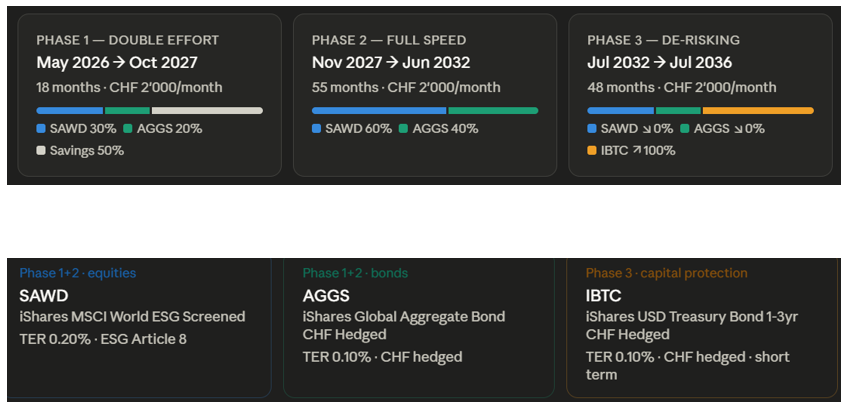

In our budget, we can save CHF 2’000/month without too much effort. In the first months, we plan to put 1’000/months on a bank account until we reach a 30k “safety belt” (we already have 12k there, that’s why this first phase only lasts 18 months in the plan below).

The main objectives of our plan :

Goal n°1 : have some available cash in 10 yr in case mortgage rates go up.

Goal n°2 : outperform the 1.65% cost of indirect amortization with reasonable risk (we are rather risk averse, goal n°1 is more important, we are not greedy)

Here is the plan :

Preliminary remark : this is our first time investing, we have no experience. We started by reading stuff on the web ( “thePoorSwiss.com” website is our main source) and chatted a bit with AI to get more tailored information about specific EFTs.

In case it’s not clear in the picture : during phase 3 we invest 100% of the 2’000/months into IBTC and gradually sell SAWD/AGGS to IBTC in order to achieve a portfolio of 100% IBTC at the end.

Our choice of broker : IBKR

Our questions :

Does our plan sound reasonable/adapted to our goals ?

What do you think of our choice of EFTs (these have been suggested by AI given our strategy but I don’t trust AI so much …) ? Any better suggestions ?

Is there anything or some risks we have missed ?

So far, we did not at all consider fiscal matters (because we have no idea how fiscality works with investment money - we are EU citizens, Swiss residents). Should we take any specific measure ?

Bonds have basically zero or negative yields in CHF, especially after taxes.

Filling your 2nd pillar (pension fund) can be a good alternative to bonds. You can withdraw this money later if you want to repay a mortgage.

Another alternative is medium fixed term notes from banks, e.g. Cembra. The yield is not incredible, but positive, and you get a depositor guarantee up to 100k CHF, twice for you and your wife.

Agree with filling 2nd pillar, the important question is who’s the pension fund provider and how are they stacking up (both in terms of returns passed to clients, and capital coverage ratios etc)

Other than that, any basic diversified index fund a la VT will pay more in dividends than the cost of your mortgage.

I will also suggest adding to pillar 2 - that is what I have done to have some risk free investments before the mortgage needs renewing. The only thing is I think you can’t make volantary purchases within 3 years of an intended withdraw .

The tax savings are significant - my marginal tax rate is around 45% in Vaud, so I more or less double my investment on day 1.

You are risk averse, yes, but you have a 10-year horizon. Putting so much into bonds now is honestly rather sub-optimal. I would strongly suggest putting it into VT. As you get closer to the 10 year you can still change (and then why IBTC, you pay income tax on dividends/yields, I would suggest something like BOXX, there isn’t even accumulating dividend there).

The pillar 3 indirect amortization will be with the bank in question, you can also invest that.

What is your reasoning behind the choice of indirect amortization and the cash set aside for when you’ll be renegociating the mortgage? Do you plan to reduce it then or to keep as many assets aside while keeping the mortgage as high as possible?

I would strongly avoid bond funds with high interest hedged in CHF. The interest is taxable but the interest differential with Swiss bonds shoud become moot due to hedging (I’d still recommend hedging bonds that aren’t in CHF as not doing it would introduce currency risk).

I’m not a fan of ESG as it seems too easy for corporations to game the system. If I really wanted to have a societal/environmental impact, I’d screen companies myself and pick stocks. Otherwise, I’d just not screen at all and support projects that matter to me on the side.

Thanks for your precious advices, the 2nd pillar suggestion is an excellent one ! That was completely out of my scope since I did not know that one can withdraw when renegociating a mortgage (I thought in was only in case you actually buy the property).

In our case, 2nd pillar filling is particularly relevant : we have only worked in Switzerland for a few years (6 for my wife, 3 for me) and on top of that we emptied my wife’s second pillar when you bought our appartement. So we have a huge margin there. I will ask the pension funds for the figures, but I did some gross estimate and we should have around ~400’000 margin so more than enough to cover the 2’000/month.

Our marginal tax rate is not as significant as @clueless ‘s one (kids, wife works at 60%) but we are around 25% which is still significant.

So overall, its a very nice investment : zero risk and once the tax reduction is included the return is very good. Thanks a lot for the tip !

The last thing we have to decide now is what to do during the last 3 years when we can’t touch our 2nd pillars anymore.

It all depends on how interests rates will evolve.

Today rates are low :1.65% is easily outperformed by investing on my own with close to zero risk (as pointed out by others, 2nd pillar once tax reduction is taken into account is much better than 1.65%).

In 10 yrs, I don’t know how rates will be. If rates are low, I don’t touch the mortgage and go for another 10 yr. If rates are high, I want to be able to amortize as much as possible (that’s why I want the cash to be available).

Yeah I know there’s some greenwashing and ESG is far from being reliable. But at least it excludes the “very bad boys”.

You are absolutely right and that is a good point to raise. I did some research and according to Raiffeisen we can get reimbursed the tax we have paid when we have withdrawn if we pay it back within 3 years. That’s already something. The amount we have to pay back is 35k. I’ll check with my fiscal advisor how this can be optimized.

No, for every 1 CHF invested in your 2nd pillar you “immediately” get back 0.45 CHF, or 45%.

If they were doubling it would mean a 100% marginal tax rate, which is absurd.

I don’t think the whole ending at 100% treasury bodns thing makes sense. Others already chimed in why foreign high yield short term bonds are suboptimal tax wise, also you are at teh mercy of the US and its debt problem potentially.

I don’t liek ESG screening at all, also quite expensive for just an msci world. Missing emerging markets as well.

I’d go for an ftse all world or ACWI etf, cheaper ones available including emerging markets. MSCI world is 70% US and an ACWI at leats brings that down to 60%. Diversification should always be the number 1 goal imo.

I don’t really get the whole 10 year timeline thing. Do you want to pay back as much as possible from your mortgage at the end? You said you want to have “cash available" in case rates go up.

Why not build a resilient pottfolio, that you could draw from to offet higher rates? Think of the 4% rule (you can go higher here then easily, due to no risk of ruin), but use that to supplement your rate.

If I were you I would make a resilient portfolio allocation and just keep at it.

Like just make a 60/40 and keep that throughout. Seems in line with your risk tolerance. Maybe add some more diversifiers, like managed futures (DBMF ucits etf) 50/30/20 stocks/bonds/managed futures is a common approach. Those have their own pecularities though and you need to do your homework if you wanna use them.

Rebalance regularly.

For every CHF 1 of income (within the marginal tax bracket), you can either pay CHF 0.45 in taxes and invest it in a taxable account, leaving you with CHF 0.55, or contribute it to pillar 2 without paying any income taxes. Your investment in pillar 2 would be 82% higher on day 1 than if you invested in a taxable account. Compared to a taxable investment, that’s not too far off from doubling. That’s ignoring withdrawal taxes and different return expectations, of course.

But it seems you hadn’t considered the 2nd pillar option when you took your decision. Beating 1.65% returns with close to zero risk is extremely hard in Switzerland:

over a 10 years period, stocks have had negative returns in the past. It gets worst as you keep having new inputs of money to invest closer to the 10 years target.

bonds have very low returns, below 1.65% (10 years yields for bonds from the confederation are currently at 0.431%; CHCORP, an ETF of corporate bonds denominated in CHF has currently a weighted average yield to maturity of 1.01% for a weighted average duration of 4.86 years, medium term notes are mostly at or below 1%).

Under the 10 years timeframe, I would say the only way to consistently outperform the interests of the mortgage are 2nd pillar buybacks.

Thx for your advices.

The idea is now to invest in 2nd pillar (see comments above) : no risk, outperforms the 1.65% of indirect amortization and is available in case rates go up. Yes indeed, the whole idea is to be able to amortize as much as possible in 10 yr when I have to renegociate the mortgage if rates are high (if rates are low, I don’t pay back anything and keep the money in 2nd pillar).

I was ready to take some moderate risks and I thought that it shoudl’t be very hard to beat 1.65% over 10 yr with some moderate risk (maybe I was naive). But now that I am aware of the 2nd pillar option thx to you guys, I’m even more happy that I took this decision. It almost feels like cheating.

Thx for the clarification.

I checked on my 2nd pillar : I have about 260k left of available “voluntary purchase”. It’s more than enough for 7 years at 2k/month. It means we’ll probably not reimburse my wife’s 2nd pillar before a long time. But if I follow your answer properly, we should still ask for the tax reimbursement right ? There’s really no reason not to ask for it (worse case scenario, we never pay back and never get the tax money back ?)

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.