Yes, but the 1.047 was calculated by adding the 0.95% to the CHF amount today, to simulate what we’ll actually get on Monday.

So I expect Yuh to be better than Revolut on Monday, but barely.

By todays standard Yuh is much worse than Revolut (1 CHF equals Eur 1.037 vs 1.045).

→ note that this is on a weekday. Revolut (Free) is worse on the weekend.

I get regularly confused about all these different fees, but I guess we will have it black on white on Monday when we see what the apps will show in the final fees.

Not anymore

At least from next month. I got an email about it. They don’t say what’s the interest on the private account, I suppose 0 (always the pessimistic possibility if nothing is said).

Positive: You(h) can move around your money as much as you want, probably last second when you need to pay something. Totally cumbersome for most, though.

Unfortunate, but still better deal than Neon which has lower interest rate and also only on the ‘Spaces’ part (same as Yuh now with the ‘Savings’ part).

Personally I prefer their solution over an overall lower interest rate, but agree that most people will miss out because they dont put it in the savings part.

?

That’s exactly what they will do. Have it only on the “Spaces” part, just that they name it “Savings” or so. Also to be pedant, you can move back and forth only 20k chf per month on Neon where apparently you can move an indefinite amount on Yuh.

Now there is a free* insurance on mobile phone (“Yuh Pocket”) etc. if you buy stuff with their debit card; insurance valid until the end of the year. They didn’t disclose how it will change after this, but write that it is “Not binding afterwards”. You can activate it for free now via a form.

Not sure what I should think of this. I for sure won’t pay for a smartphone insurance etc. but if its free then why not use it. But on the other hand it seems quite untransparent whether you will automatically then be enrolled and you have to cancel the insurance otherwise you pay etc.

Yuh in my view lost it. They started to introduce complexity, as a way of milking their customers more. One example is this new Yuh Pocket insurance (who gets / uses this?)… another one is that they now only pay interest on savings pods.

Spent the last few days sending money back and forth to optimize the interest. This is just nuts. Is there a decent alternative anywhere?

I’m fine with it for now. I have my emergency fund there in the savings part and in the other I keep ~500.- at the end of the month. That is 5 CHF lost in interest over the year.

Not that much of a hustle and still better than the interest you get at Neon or other similar banks that you can actually use for your daily life (unlike things like WillBe bank etc).

The alternative would have been to just lower interest rates overall. So I think for us “aware” users, their strategy of getting money from the “average customer” that doesn’t care is actually beneficial.

I’ve got email and also in-app notifications.

New rules since 01. July.

See also here:

They don’t say it that prominently on their website now. They just say that you can earn 1% with the saving options (before they were making big claims that you get 1% everywhere).

Its not nescecarily one feature - its the overall complexity. How many people actually get where to find your Pillar3a for example? Yuh seems to think that complex was good - think that this was a deadly mistake. Especially when combined with bad comms. I nearly missed the announcement on „savings in pods only“… so they nearly produced a pissed off customer.

Good thing they hide it, as I wouldnt recommend the Yuh 3a anyway

Personally i dont find them too confusing though. You can literally ‘play the app through’ (i.e. see ever possible thing you can do in the app) within 15 min by clicking through all options. Try doing that with UBS or similar, they have way more features IMO.

Main thing that is missing from Yuh for me are monthly statements in .csv or any tabular format. They only have PDF which makes budgeting very annoying.

I think they indeed have issues there. I know also someone who didnt get an email, while I got email + pop up when I opened the app…

An excellent opportunity to sell and transfer your money to a real broker?

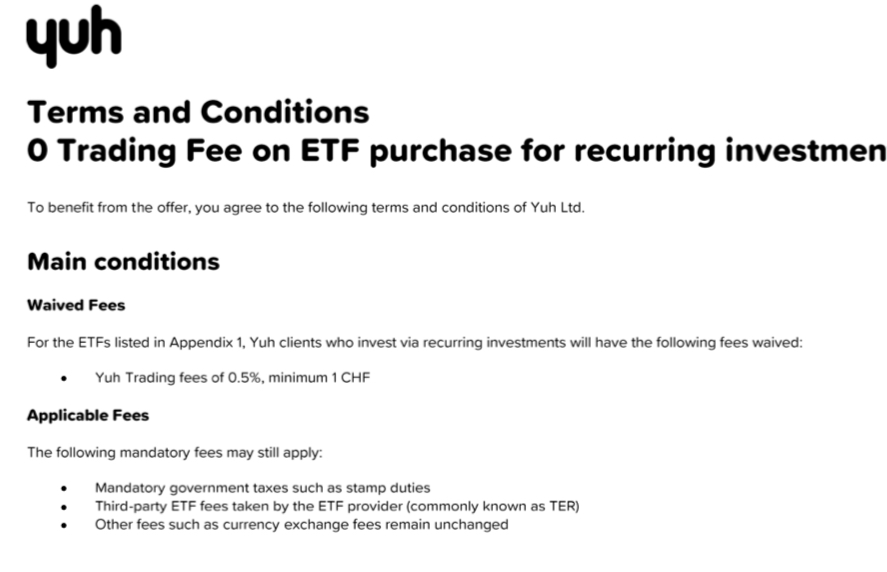

6 ETFs, no trading fees

Seize the golden opportunity to grow your ETF portfolio. We’ve selected a stellar line-up of CHF-denominated ETFs to make sure your investment journey is not only fruitful, but also a breeze. With shining stars from major ETF issuers such as iShares, Vanguard and Invesco, we welcome you to your very own financial paradise, where each move is designed to build growth on stable ground.

Our A-list of ETFs with 0 trading fees

Large Cap: World

VWRL: Vanguard FTSE All-World UCITS (CHF)

High Dividend: World

VHYL: Vanguard FTSE All-World High Dividend Yield UCITS (CHF)

Large Cap: Developed World

IWDC: iShares MSCI World CHF Hedged UCITS ETF Acc (CHF)

Large Cap: Switzerland

CSSMI: iShares SMI ETF (CH) Dist (CHF)

Nice to see lower fees, but it’s not that attractive even we have the 0 trading fees for e.g. VWRL right?

For VT you pay a tiny amount of fees per trade at IBKR and it has a TER of 0.07 vs. 0.22 at VWRL, and this not even looking at the tax advantages due to reimbursements of WHT.

Would you recommend using this new Yuh Sparplan to anyone? Maybe yes because of simplicity/ease-of-use?

That is an optimistic take

Terms and conditions state that it is for recurring investment / sparplan. I don’t think there is any selling sparplan that they offer!

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.