Thanks for pointing that out. I had a wrong understanding of how fictional dividend distributions and taxable value at the end of the fiscal year interracted (that is, I thought there was an interraction while there is none).

1 Like

Depending on the perspective¹, you could call it a loan, yes. However, whatever you call it, it results in reducing the expected DA-1 delay loss from e.g. 7% to roughly the risk-free rate of currently 1% without any downsides, as far as I can tell.

Hence, I would say it does affect your calculation. In my opinion, it means that (at least in ZH) there is no point in calculating a 7% p.a. loss for DA-1 as it can easily be avoided for the most part.

¹ I might argue that it’s unfair practice of the tax office and they should credit both Swiss withholding and DA-1 to the tax bill with a value date of either end of September or end of December of the tax year. With the low interest rates here, the difference is typically not all that significant, though.

No, that’s not the same. You can do that, of course, but that would be investing with a (small) leverage which comes with additional risk while my method doesn’t add any risk (as long as the estimate is not higher than the actual DA-1 credit).

The amount may be small enough that you don’t mind the tiny leverage and the additional small risk but conceptually it’s quite different from my method with regards to investment risk.

Sometime back I checked WEBG was not in Ictax. Most likely because it’s a new ETF and would need to report its numbers to Ictax at end of their financial year (which is December)

I guess same is true for WEBN.

justetf.com has a field that describes it (I think)

Tax Status

Switzerland No ESTV Reporting

But this ETF was started this year, so there was nothing to declare so far. There are many reports (actually from @Abs_max ) that funds were included to ictax after a simple request.

Yeah.

I guess I should ask Ictax team about adding WEBG because I actually own it.

This one should be easier because it distributes dividends anyways.

1 Like

Update

ICTAX told me that WEBG is now registered for 2024 course list.

However since there is no info received yet, no data can be published

4 Likes

Good to know. I guess that if they have added WEBG, then WEBN which is the same but reinvesting should be covered too right?

I mean, what they want to know, which is dividends generated, is the same value for both. If not, I’ll ask them to include the brother etf.

Yes they most likely will add it because I think WEBG & WEBN are part of Amundi ICAV annual report which comprises all of the ETFs from Amundi domiciled in Ireland.

Just FYI -: WEBN was launched in June i.e. different point of time vs WEBG. So maybe they are two different ETFs. It should not matter but thought to let you know.

Hello,

I have a question that may seem basic or obvious to you, but could someone point me to a reference site or a way of finding out in which currency ETF dividends are paid?

Specifically, my question is whether WEBG SW (SIX Swiss Exchange) and WEBG GY (XETRA) dividends are paid in USD or whether WEBG GY (XETRA) dividends are paid in EUR.

My research has been in vain so far, as all the sites I’ve found indicate that WEBG has not yet paid any dividends.

Thank you in advance for any replies.

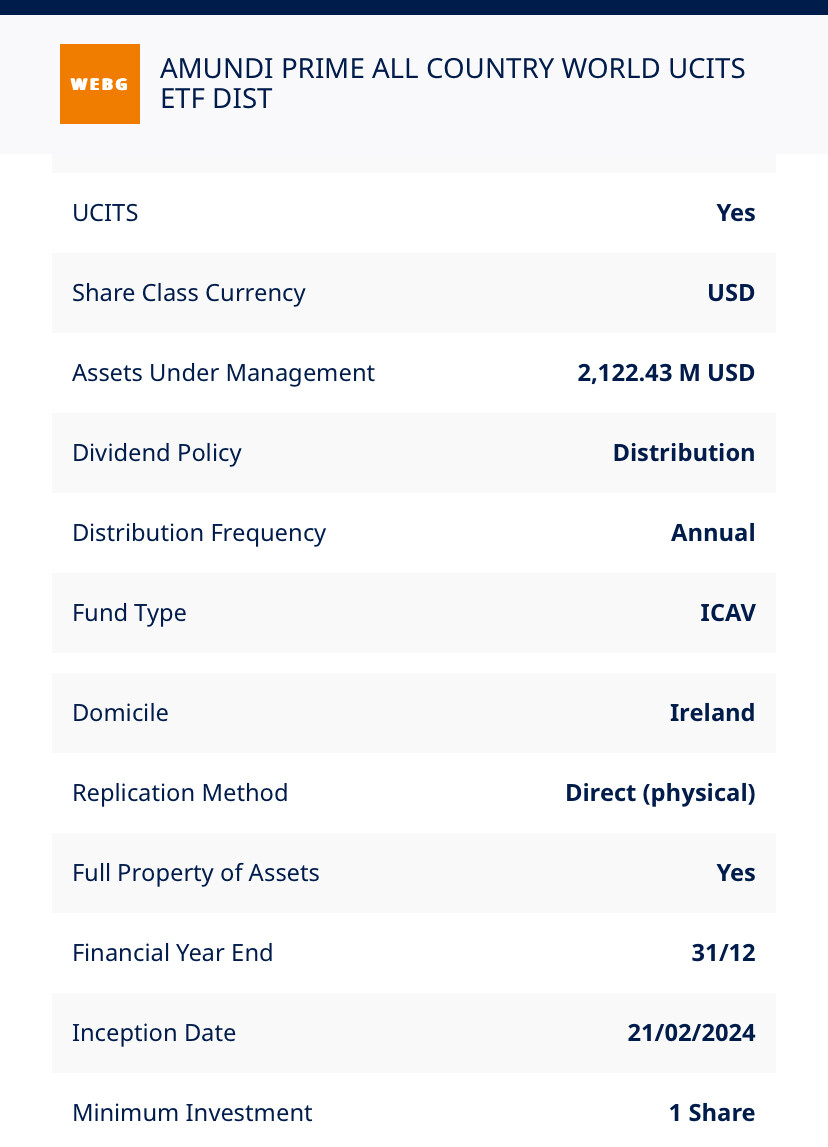

Most world ETFs pay dividends in USD because dividends are paid in base currency of fund. Atleast it’s true for following.

WEBG

VWRL

VEVE

It doesn’t matter which exchange you buy the ETF because ISIN is same

P.S -: best place to find this info would be in fact sheets. Look for share class currency

4 Likes

You can look this up on justetf.com, under the section “Basics” they list fund currency and, under “stock exchange”, the trade currencies.

1 Like