Could be, could be not, no one knows. Small size is one of the original Fama-French factors.

The thing is that you decide what portfolio you should have, not the fund provider. Do you want small stocks? – Good. Don’t want them? – Excellent. When you buy an MSCI ACWI you should reasonably expect that the fund matches it, right?

In the end it will not make you much richer or poorer. But my preference goes to index investment vehicles that I can understand and trust to do follow the index. Otherwise there other options, like Avantis funds that do active selection of stocks. Or if you believe in growth, there are some good index options and active ones.

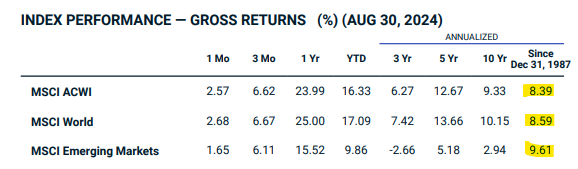

Slightly offtopic, but how does this make any sense?

Shouldnt ACWI performance always be somewhere between World and EM, just like 3 Yr, 5 Yr and 10 Yr?

That puzzled me as well. The only explanation I have is the changing proportional weights of EM and World. The growth in EM took place when it was some 2-5% of the ACWI. So the impact of that growth was less then underperformance of the EM later, when it was a larger share.

EM had its big run, when it was super small (and then became big, like towards 14% and since declining). Therefore its positive effects in acwi were very small over the longterm and its negative effects more pronounced.

But you are not avoiding the chf appreciation issue.

It‘s the exact same fund in usd/eur/chf, it‘s just the currency it‘s displayed in and you trade it in.

Only currency hedged funds, hedge against fx movements, but hedging is not free and comes with it‘s complete set of caveats. Starting at available cheap products.

From the available ucits funds, FWRA or VWRL are available on Six in CHF and you can avoid fx fees then.

Fwra as accumulating and lower ter, is probably the better idea. As you also avoid VWRL distributed dividends in usd, that would need to be converted (or your broker does autmatically for a fee)

If US ETFs aren’t an option, I would go for FWRA as well. 30% less fees than VWRL and a great tracking difference so far (0.15-0.2% better than the index).

Can be bought on neon with 0% fees (except stamp duty) through their monthly savings plan.

VWRA is accumulating. Total return for VT is based on the assumptions that all VT dividends are invested the same day they are distributed and that there is no withholding tax.

But for us Swiss investors in VT, there is WHT, we get it back way later and, depending on income tax rate and deductions, not necessarily in full, and we pay more income tax as the dividend yield is higher.

I know they don’t track the same index, but still: is VT worth it?

I think in order to answer the question if VT is worth it, we need to think about future expected returns

So , let’s assume -: there is no small cap premium. This means investor would get similar returns from All caps portfolio vs Large & Mid cap.

I also think we should use similar TER ETFs, to eliminate TER difference. So we should use WEBG

You can play with the calculation below. But my summary is following

PRO for VT -: approx 0.1% performance (I.e 100 CHF per annum for 100K portfolio) assuming 100% DA1 refund

CON for VT -: US estate taxes jurisdiction and related paperwork

So it comes down to how big is the portfolio and how much 0.1% matters. I personally have lost interest in US ETFs over time

Virtual dividends I got from ICTax and the returns from Yahoo Finance (closing price on 31.12.2019: USD 85.93, closing price on 29.12.2023: USD 118.44, 118.44/85.93=1.3784)

I understand but as investors we should focus more on what is expected vs. what has happened. Reason being -: data might show that VWRA outperformed VT after taxes, but that is not what is expected, it just happened due to small caps underperformance. If small caps would have kept at same level as Large/mid, then VWRA should have underperformed

If we want to isolate one factor, like management performance, effect of witholding taxes, currency of the fund, accumulating vs distributing or full replication vs partial vs synthetic, I think using past data is the better way to go, as it provides actual data from the field instead of theoretical calculations based on modelling. In that context, what matters is how two funds react under the same set of circumstances. The absolute results don’t matter, rather the relative differences (or similarities) between the two.

In this case, the indexes would need to be the same, though. I’d also like to have similar replication methods though perfect comparisons don’t exist and the line has to be drawn at some point with qualifiers applying to the results.

I would like to invest a few thousand francs per month in a world ETF at Swissquote (I prefer a Swiss broker). Which world ETF can you recommend?

I think it makes sense to choose a world ETF that is listed on the SIX and traded in CHF in order to get the ETF flat rate and not pay any exchange fees (0.95%). Am I right? The VT, which is often recommended in this forum, would not be an option, right?

In this case, VWRL, FWRA and SSAC, for example, would be considered. Are there any others that you could recommend? Whether it is distributing or accumulating is less important to me. What is important to me is that the world ETF has performed best in the past and hopefully will continue to perform best in the future.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.