Sorry. I started the talking about bond-inherent problems (applying to any interest rate), as many newbies may not be aware of.

(I’d love to read a @Julianek-essay about this)

And @Cortana I think missing a higher interest rate at roughly the same risk is actually an opportuity cost or a loss

Pre-2008 you would google “obligationenliste”, find a PDF from some Swiss regional bank with a bonds catalog in various currencies, pick your ISINs.

Excerpt from an old binder:

Nestlé Finance International 5 3/4% in AUD

Toyota Motor Credit corp 6 3/8% in AUD

Kingdom of Sweden 5 3/4% in AUD

There was a currency risk but until 2008 for instance the AUD/CHF rate was quite stable, around 1.

I want to add that it also makes sense for foreign investors from countries with positive interest rates to buy bonds with negative interest rates because the negative interest rate turns positive after hedging.

Esisuisse has a total sum of 6 billion. If a bank pulverizes more than that when it goes belly-up, you’re not guaranteed anything and have to queue up with everybody else,

It’s a risk that I take, by diversifying between banks and staying below 100kchf, though.

I agree, it’s not enough to cover the default of a big bank, but you don’t end up randomly in the queue even when the 6billions are over. You still have priority over most of the other creditors.

Above 100k diversifying banks is certainly a good approach of course.

Why not parking cash at one of the 21 Kantonalbanken mit Staatsgarantie? Assuming they start with negative interest rates at 100k, you still have roughly 2 Mio that you can hold. And it is diversifying if you are afraid that the canton of Zurich may go belly up.

Classic literature does suggest bonds as combination with stocks. I am not in general against this theory. However I did move out of bonds around 2018 when VIAC’s Daniel Peter said they’ll not offer bonds as «you’re almost guaranteed to get negative returns in the future». I was surely influenced by friends and people on this forum doing the same.

When looking at the performance of US bonds don’t forget the exchange rate…last year for example it had a very significative impact on returns.

Pure performance however was not the point of holding bonds in a classic portfolio, it’s the inverse correlation with stock, with lower volatility and (small) guaranteed returns.

Now that the guaranteed returns are negative and the inverse correlation is not clear anymore I’m not sure the assumptions are still valid.

I think that at this point bonds have become a purely speculative asset, not much different than gold. It might still make sense to hold some but I wouldn’t be comfortable with a large allocation.

I have about 5% of my wealth in bonds, 15% in cash, the rest in stocks.

I own BND and VETY. I am reading all I can to try to understand if I should put some more in bonds. But these interest rates, I see very little upside… And a potential rather big downside.

I think it is safe to assume the rates will not increase for a while… But is the risk worth the 1-2% return you usually get on such assets? I do not need that much cash at all, I can survive a long time without selling anything… Should I increase my bond exposure, maybe corporate bonds?

The only upside is that the ECB or the Fed lower short-term rates (unlikely) and increase their QE. In any case it’s a very risky bet. If you want to buy bonds, prefer short durations like Buffet does (max 2Y iirc).

Wow you have Eurozone bonds with a dividend yield of 0.14%, you are quite adventurous my dear Myself I hold VUTY since end of last year and I find it already enough for my risk appetite. At least it as a dividend yield of 1.42% but like you I am also wondering what is best…

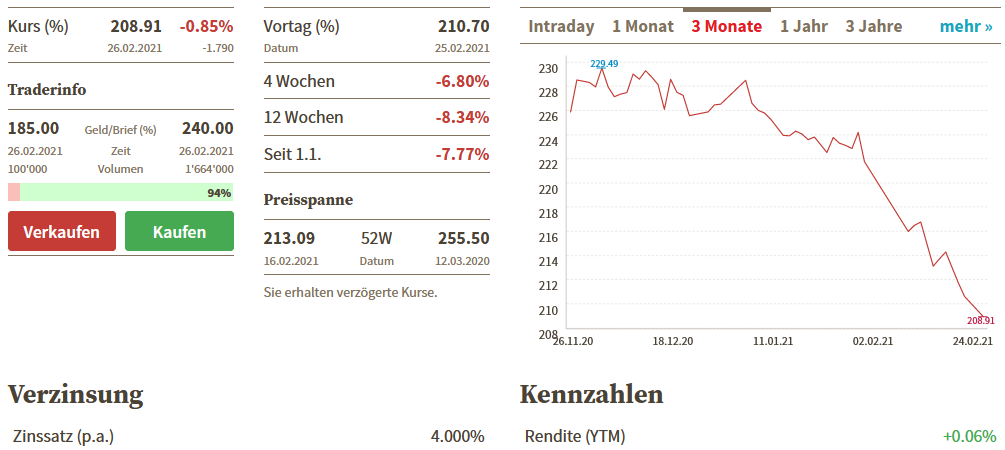

Thanks for pointing toward the terrible YTM of VETY. Seems that is negative right now at -0.2%.

I will liquidate this as it seems very foolish to keep it at this price.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.