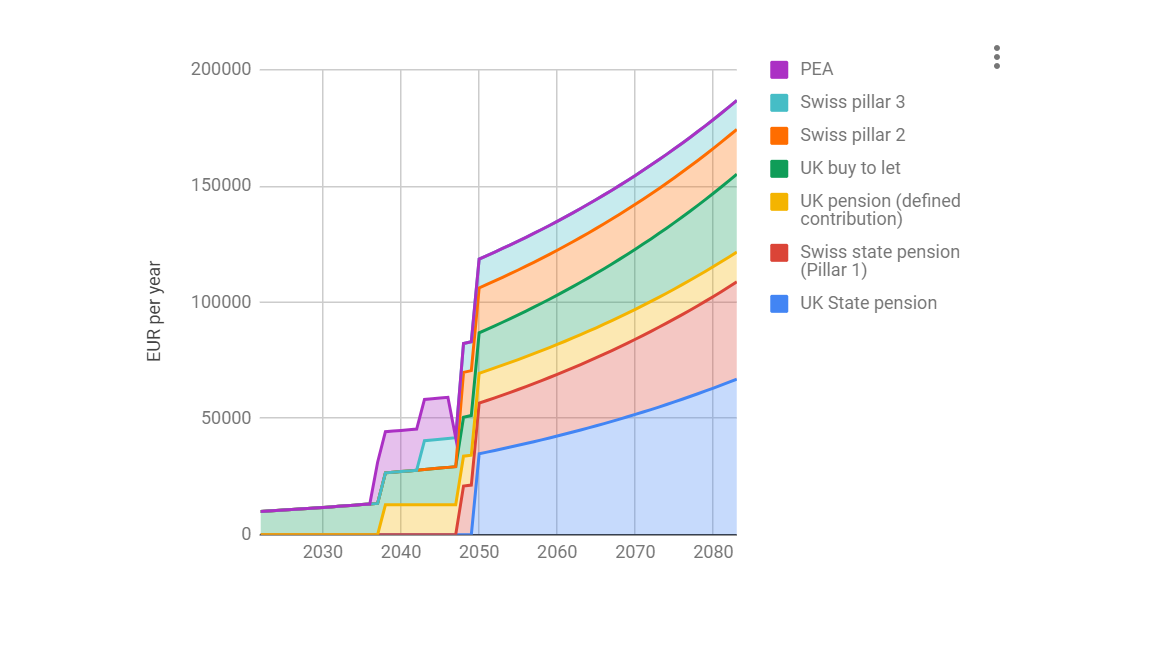

I’ve often wondered how you know when you’ve got enough in pensions so you should prioritise money that you can access before 65. I decided to do a calculation to get a feel for things.

I assumed that for a basic existence I need 50,000 EUR (I live in France) to fund my lifestyle with and assumed 2% inflation. Around my standard retirement age I would need around EUR 87,000 per year. This is for my family, not just me.

Then looked at what I would get from state pensions (pillar 1 in CH and a similar UK scheme); pillar 2s (based on the regulated annuity rate); then some assumptions around growth for the various pensions that I have some control over (pillar 3s and similar UK schemes). I looked at when they would become available and compared the various incomes with the spending requirement for each year. All adjusted for inflation.

My calculation showed that after the standard retirement age, the pension savings I already have are currently a little higher than I would need. Obviously if investment returns are lower, state pensions get worse (very likely!) or I decide I need more money then things change. Obviously I’m not able to stop contributing to most of these retirement accounts so there is an increasing buffer being built in.

I also have some post tax investments. these would be used to cover the period between retirement and early retirement. I have included no estimates for any future saving I might do. I will of course continue to save money.

Most important things from this analysis from my perspective are that:

a) pillar one type schemes are great and if you have the choice to contribute voluntarily in more than one country (as UK citizens do for example) then it could end up covering a really big part of your retirement needs.

b) There seems to be a real risk of over saving in pensions. Chasing tax efficient saving could end up with a very well funded retirement but leave a big gap until you can claim it.

c) Once you’re fairly sure there is enough in the post normal retirement age pots it’s time to really prioritise investments that can be accessed before traditional retirement age.

Note that UK state pensions look massive because the assumption is that both my wife and I get a full one each and that they remain indexed to inflation. Lots of uncertainties.

One remark from my side: if you exit from the workforce before “traditional retirement age” you’ll have to move your Pillar 2 to a Vested Benefit Account and you’ll have to cash it (no monthly “pension”).

Pillar 3 you’ll have to cash in any case.

The possible growth (or decline…) of these 2 instruments (P2 and P3) is therefore linked to the way you decide to invest them and your disinvestment (withdrawal) plan. Imo for RE in CH the only “guaranteed” income flow you can count on is P1.

This is interesting, are you allowed to join the Freiwillige Auffangeinrichtung BVG even if you definitely stop working ? Looking at their factsheet it is not 100% clear to me…

a thing to pay attention to seems to be that you have to subscribe within 3 months after you leave your last employer’s P2

I’ll have to dig into this in order to understand if it’s worth it

I guess you already checked this out, but: As I understood the EU agreements, the country you retire in (or worked last) will collect the other countries contributions. The agreements do not foresee voluntary payments once you have left the country, as is the case in CH where you can only join the voluntary pillar if you emigrate to outside of the EU.

Post-Brexit you can do this again in the case of the UK, but if you have an entitlement from both CH and UK before Jan 2021 it might be worth to get some professional advice.

I agree, this is a significant risk. While I expect only some reduction in the amount (in real terms), it seems likely that the entitlement age gets pushed to the right.

I look at the question from the opposite angle: if I RE what is my annual spending and what is the amount of assets (including 2 pillar) I need to support that at a conservative “SWR” (Safe Withdrawal Rate)?

If you retire early with a long investment horizon you will almost certainly be better putting 2P in a vested benefits scheme like VIAC or FINPENSION as returns should be higher. So I count on this as an asset in the above calc

Then all that is left is UK state pension and 1 pillar. Personally I don’t count on these because I plan on the safe side and also for simplification but you are right they do represent a fair amount

The problem trying to forecast future incomes is inflation and related to that Fx. As you point out uk state pension looks weird in your chart - currently it is max £9 k/yr. Would future governments allow it to grow by so much as your chart suggests in CHF terms(?)

The federal council adjusts pillar 1 every two years based on equal weighting of LIK and a salary index, if I remember correctly.

2 Likes

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.