Yes (market value less what you pay, if gifted 100% taxable). But with ten employees, your plan would not work anyway (capital reduction is paid out to all shareholders equally, just like the divided). You are an employee, and as such don’t really have improvement potential by use of the company’s capital structure.

You will have to calculate that for your specific case. In general, until the recent tax reform, it would have been beneficial in most cantons to pay out a dividend. This has changed a bit, and paying a higher salary now might be in fact the better solution. This is true at least in a long-term setup and when optimizing pension fund contributions. For a one-off payment, dividend is likely still the preferred way to go.

OK, but the dividend plan would still work, right? I buy 10% shares in the company I work for, then I am eligible for 30% reduction on income tax. But the dividend would be distributed according to the ratio of share ownership, right? So all owners would have to agree to payout a certain amount of income as dividend. So for me to get my 10% of the total dividend, the others would also have to get their 90%.

The question remains, if the savings would be big enough for it to make sense. After all, if 10% shares cost 100’000 CHF, that’s 100’000 that could otherwise be in the stock market, so the alternative cost is already high.

Right… As if I know how to do that

Anybody can recommend somebody I can hire to do the calculation for me? My accountant is too incompetent to trust her…

No. To clarify (seems you misunderstood @Cortana’s initial input): You will only get preferential taxation (discount) if you own 10% of a company on the dividends of said company, not on the income that this company pays you.

Sorry, your reply confused me. Let’s go again step by step and you tell me which step I’m wrong.

The company decides to pay dividend to its shareholders.

The dividend is paid a fixed amount per share.

The income from this dividend is recorded on your tax declaration just as the dividend from any other stock, or an ETF, would. And you pay income tax on it.

If the percentage of your shares in a company exceeds 10%, only 70% of the dividend income is taxed. I guess it’s a special cell in the tax declaration?

So in order for this to work, all shareholders would need to agree to payout very concrete proportions of their respective incomes as dividend instead of salary.

Well, my former boss used to say the first step to optimize taxes isn’t a tax consultant, but a good accountant.

But seriously, you can figure that out yourself (hiring someone separately likely costs you the full saving on that one-time CHF 50k taxation).

First, the easy part: Use the tax calculator of your canton to figure out what the taxation on the dividend option is. If you feed that correctly (realistic scenario to get the proper marginal tax rate), and if the canton’s calculator allows you to easily mark this as a dividend from a qualified participation you already have scenario 1.

Secondly, the harder part: Figure out the total (marginal, so typically without pension fund contribution) social security contributions (both employee and employer) on that income is, plus again with the tax calculator your income taxes on it. This is a bit tricky if you want it to be very accurate because social security contributions change depending on the total salary. You then credit this scenario 2 with the tax savings you will get at your company for paying out this salary.

All correct. Sorry then, seems I misunderstood your second to last post.

And yes, it’s a special box in the tax declaration where you clarify your shares of that company as qualified participation (Qualifizierte Beteiligung).

For state taxes, this will reduce taxation to 70%, and for Zürich’s cantonal taxes this will reduce taxation to 50%.

The thing is the company will have to pay taxes on the amount paid in dividend and not in salary, so it is not magic.

What’s more, because the result of the company is higher, the non-distributable general reserve will grow.

And finally, I read that the AHV/AVS has the right to consider part of your dividend to be considered as a salary if the said salary is under the usual salary. From BGER 145 V 50 :

Gewinnausschüttungen ([BGE 141 V 634] E. 2.2 S. 636 mit Hinweisen). Von der durch die Gesellschaft gewählten Aufteilung zwischen Lohn und Dividende weichen die Behörden nur ab, wenn ein offensichtliches Missverhältnis zwischen Arbeitsleistung und Lohn einerseits und zwischen eingesetztem Vermögen und Dividende anderseits besteht ([BGE 141 V 634] E. 2.2.1 f. S. 637). Rechtsprechungsgemäss werden deklariertes AHV-Einkommen und branchenübliches Gehalt einerseits, sowie Dividendenzahlung und Aktienwert anderseits zueinander in Beziehung gesetzt, um zu prüfen, ob ein solches Missverhältnis besteht, und zu bestimmen, ob ein Teil der ausgeschütteten Dividende als beitragspflichtiges Einkommen aufzurechnen ist ([BGE 141 V 634] E. 2.2.2 S. 637).

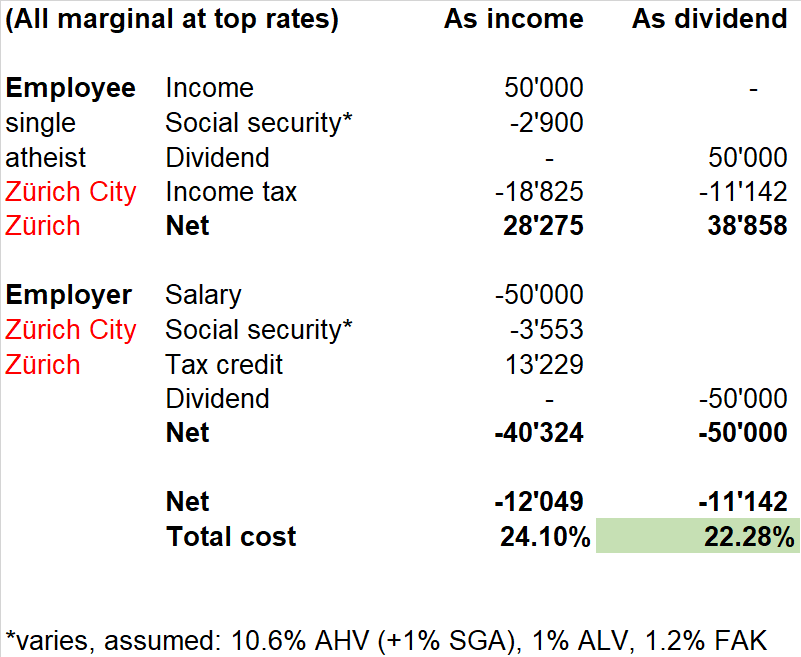

All good points @REandSTOCK. But, I did some math (I’m bored, thanks Corona ). Assume it is completely wrong and full of errors. I’m still an internet stranger, if you want it done properly and explained, you’ll have to pay me

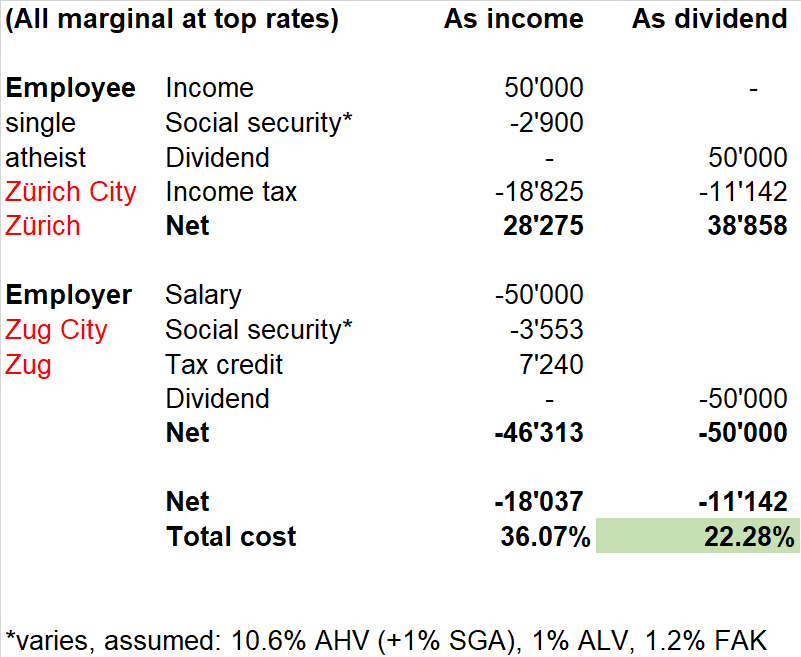

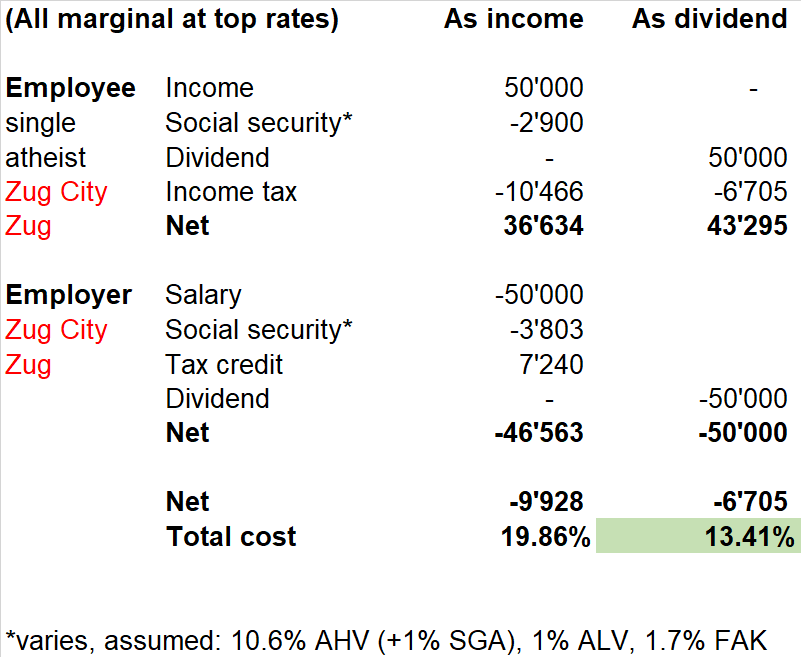

Basically, Zürich’s taxation is comparable (as it should be). If your company is in a low tax canton, the tax credit is too small and generally dividend is most always the preferred way (even if you yourself are in that low tax canton too).

That’s what I was looking for . I was going to calculate it myself, but you’ve saved me some work, thanks!

I’ve got 3 questions here:

Where is BVG? I know that it theoretically isn’t a cost. But I assume that in the dividend option you don’t pay it at all, and in the salary option the employer’s contribution isn’t taxed?

Calculation is for a one-time bonus, therefore not part of BVG / 2nd pillar insured salary. If this payment would be declared part of the contractual total compensation package, it likely would have to be BVG insured.

Tax credit: The taxes the company saves by being able to deduct the salary from their taxable income.

Income tax on dividend: There is none. Of course one could also not have included the tax credit in the income scenario and instead an additional income tax in the dividend scenario, but result would basically be the same (it’s a matter of what you define as baseline scenario).

AHV is 2 x 5.3% for both employer and employee for a total of 10.6%. This is fixed and does not vary.

Correct. I checked it and it’s like you say. But yes, theoretically, if someone has a high salary, like 150k, they could reduce it to 100k, and so reduce BVG. But someone above wrote that the authorities might not accept that?

Ah, so you calculated it the other way round from how I imagined it. In the salary case there is no income, so the tax credit is only imaginary. In the dividend case there is actual income and actual income tax to be paid by the company.

Your BVG insurer won’t have an issue with it (because you choose your insurance level and are way above mandatory minimum anyway). But, your AHV Ausgleichkasse and your tax authorities might intervene, if they perceive the relation of income and dividend to be grossly miss aligned.

It used to be very easy: Pay yourself at least CHF 120k salary and you may pay everything above that in dividend. That still holds true to some degree, but in recent years especially the AHV Ausgleichskassen have defined more detailed criterias (they need the money after all). Specifically:

They now compare salary with the Salarium, so as management member or specialist in high paying jobs that minimum salary might be quite a bit above CHF 120k.

What really triggers them however is the dividend. If you regularly (yearly) pay out more than 10% in relation to invested equity they will look into it. Below that you should be fine, no matter how big the amount.

It is just like with the professional trader designation: There are no hard limits, just don’t overdo it… (and ultimately only a judge will have final say, after the fact).

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.

). Assume it is completely wrong and full of errors. I’m still an internet stranger, if you want it done properly and explained, you’ll have to pay me

). Assume it is completely wrong and full of errors. I’m still an internet stranger, if you want it done properly and explained, you’ll have to pay me

. I was going to calculate it myself, but you’ve saved me some work, thanks!

. I was going to calculate it myself, but you’ve saved me some work, thanks!