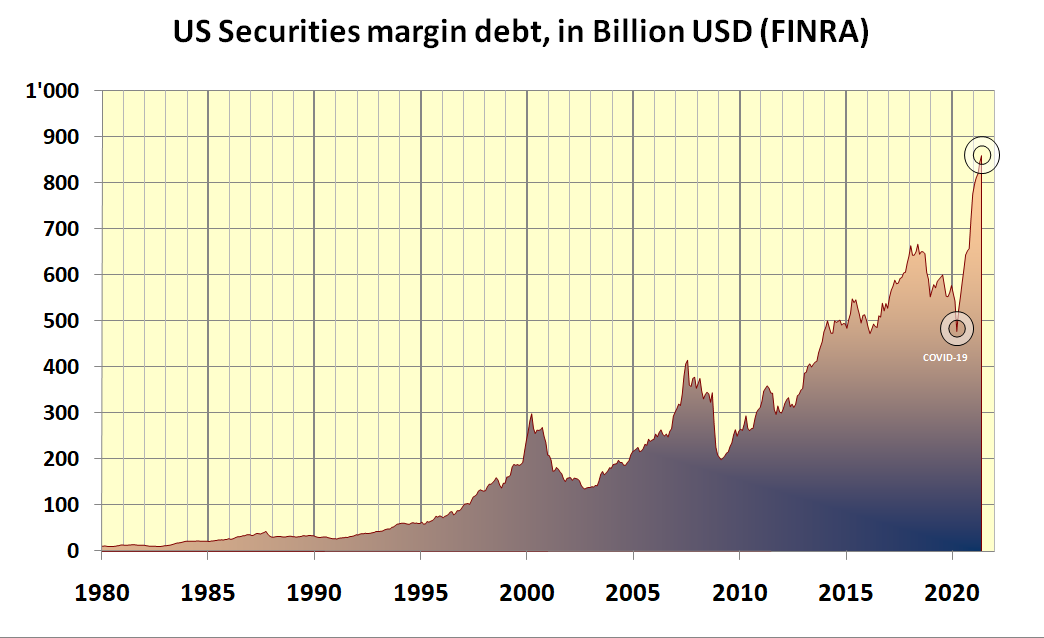

So, how deep down the rabbit hole are they and will other banks follow that move? If financial institutions are endangered once again and customers see their credit scores reduced (meaning higher interest on their credits) and get driven toward more risky (and more expensive) forms of credit, potentially margin loans that could be called even in a moderate stock market correction, how more tense are we making the stock market and how much self-reinforcing effects are we building in it so that bad things can funnel worse things quickly?

Cutting liquidity goes opposite to the current policy of central banks, I’m curious to see what may unravel out of it. We’ve already had the Archegos-Crédit Suisse adventure. I’m not ready to act upon it but my bet is that a market correction is near.

Edit: to make my thinking more clear: tightening credit is one of the trigger of stock market crashes. I don’t like where this is going.

Maybe we should see that in a more positive light.

In light of their sales and lending practices (in addition to the pandemic) and subsequent scrutiny from regulators and the government, I am not hugely surprised.

After all, Wells Fargo are the guys that recently opened up millions of fake accounts/cards without customer consent. And who knows how much toxic waste of credit is hidden in and behind these lines of credit?

Last year, the lender told staff it was halting all new home equity lines of credit, CNBC reported. Months later, the bank also withdrew from a segment of the auto lending business.

Reason:

In 2018, the Fed barred Wells Fargo from growing its balance sheet until it fixes compliance shortcomings revealed by the bank’s fake accounts scandal.

They are just now allowed to participate in the lending bonanza. There are signals to worry about a market crash. This is not one of them.

It would make sense for it to happen eventually in any case, haven’t had much correction in a while (and covid was exogenous). Good luck if you know when tho

Often the trigger is a series of rate hikes, and that doesn’t seem to be near, right now.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.