Please search the forum before asking these questions. This has been answered many times here , here , here , here , here , here and here.

So, once and for all, the quotation currency of a security is not important, what matters is in which currency the underlying business is having revenues/paying costs.

Otherwise, if i follow your thoughts, you would be happy holding on Nestle because the stock is quoting in CHF, right? That would be forgetting that Nestle does an immense majority of its business in India, and by holding it you have a big exposure to the Indian Rupee.

But you know what? Why don’t you do an experiment? Why don’t you check the closing prices of VWRL, both in CHF and EUR since the beginning of the year, and compare it to the EUR/CHF rate since the beginning of the year? The fx rate has already moved a few percentage points.

Depending on the results,

if it really does not matter, then you settled the question for good

if otherwise it does matter, then you have found a cool arbitrage opportunity

For holding an equity ETF like VWRL, you can put it much simpler:

What matters is what the underlying stocks are, that the fund is holding. Period.

A 2.91% stake in Microsoft is a 2.91% stake in Microsoft. I one stock unit of Microsoft’s is worth a 100 USD on NASDAQ, what would it be worth on the Swiss Exchange, given an exchange rate of 100 USD/97.50 CHF?

The answer’s 97.50 CHF.

If you could get it for 95 CHF on the Swiss Exchange, you should buy as much as you can - and at the very same time sell for 97.50 on NASDAQ. That’d be risk-free profit - or otherwise called arbitrage.

Have you?

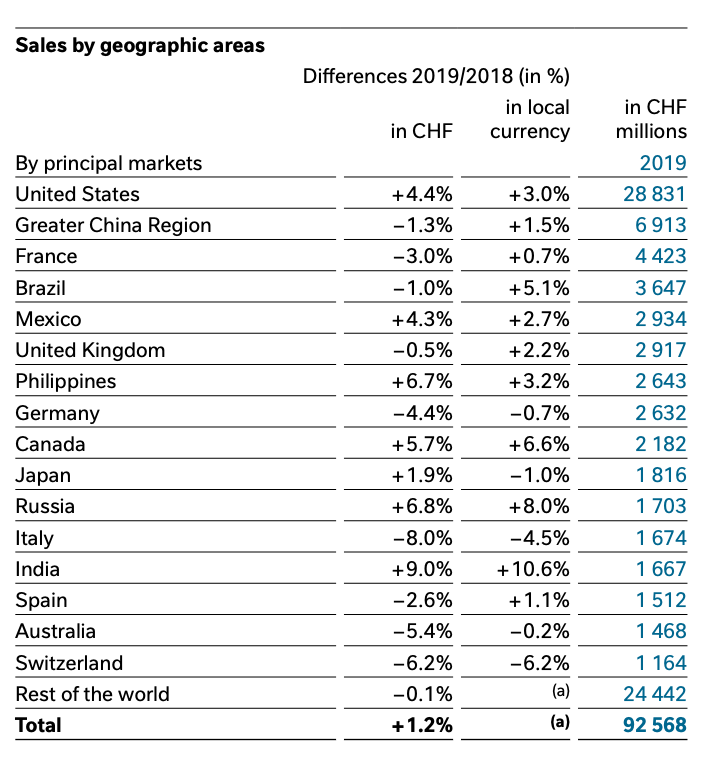

This “immense majority” seems to be about 1.8% of worldwide group sales.

That’s still more than the 1.3% they making in Switzerland.

Thank you for beeing patient with me. I’m trying to explain to you where I’m struggling.

I never questioned the second half of this statement. I’m struggling with the fact that there are currency conversions involved and that the quotation currency of the security (here USD) are not equal to my functional currency (here CHF).

It is argued that the currency risk does not reside in the report currency and the quotation currency of the security/ETF. Alright. It is rather the exposure of the cash flows of the underlying companies to other currencies.

If it’s like that then why is this only relevant for corporate entities and not for individuals like myself? And I should not worry about converting CHF to USD now, buy VT and in 20 years sell VT again and convert to CHF? This I call cash flow as well.

At least for dividends payment I guess this is relevant. Cuz it’s cash.

Scenario: CHF/USD 1:1. 2 USD dividend = 2 CHF = 1 apple.

Scenario: CHF/USD 1:2. 2 USD dividend = 1 CHF = 0.5 apple.

You are “converting” your currency into the underlying asset currency anyway even if you don’t convert it.

For the dividends it is the same as selling part of your shares.

You ARE taking the risk you don’t want to take when you buy the assets, no matter the currency you buy the ETF in. Maybe itis easier to understand from this angle.

As long as you are living in Switzerland, you’ll (most likely) be earning in CHF - and have most of your costs in it as well.

You should not worry about exchange rates, if and given you’re absolutely 100% sure and dead set on buying VT - and nothing else.

If it’s price were 1000 USD in 20 years, in the year 2040, it’s price in CHF would be… 1000 USD multiplied by 2040’s exchange rate for CHF to the dollar. Why should it be anything else? It’s the same stakes in the same companies - so if a dollar is worth 0.5 CHF in 2040, VT on Swiss Exchange would cost 500 CHF.

You might want to worry though about exchange rates for the fact that VT is mostly made up of American companies, and the U.S. market and costs are heavily overrepresented in VT.

Thanks a lot. I might see some light at the end of the tunnel. Still need to process all the replies and provided links.

I guess to some extent this isn’t easy to avoid. Looking at the table from @Julianek the even the big Swiss shots are heavily exposed to non-CHF currencies. I assume we would see similar pictures for all SMI members. If one wants more exposure to CHF then I guess one could only invest into Swiss bonds or Swiss real estate companies, with all costs and revenues bing generated in CHF.

With the strong CHF in the back it seems to be anyhow a dilemma for Swiss investors.

Just want to add another thought.

I was listening to an investor with 25+ experience. He was saying that if you’re an investor with EUR as your home currency and expect that Roche will be doing well, then it might be additionally worth to invest in it to benefit from an appreciating CHF as well (of course that’s a bet). Because - assuming your bet was right: price of Roche increased + CHF appreciated over EUR, you sell it and get more EUR back than you invested. Even if the price of Roche would stay constant, you get more EUR back, than invested. I can follow that logic.

What is the difference here to the remarks given by you?

Here currency plays a bigger role because Roche is only traded on a Swiss Exchange in CHF (let’s put aside a small OTC exchange in Germany with low volumes in EUR) and is not traded globally with efficient market mechanisms factoring in every information like exchange rates? And you really can gain or loose “value” because of changes in exchange rates?

If I’m not mistaken VT is only traded in US in USD. Hence, why should we assume current prices are fair and reflect the relation to the CHF properly (given there is no relation when only traded in one currency)?

Pls don’t get me wrong. I don’t want to argue against your remarks. Still trying to understand this topic as much as possible.

The investor with 25+ experience is not mmh very experienced, as his comments show a serious lack of understanding. Try not to follow his logic, as logical as it sounds to you.

BTW Roche trades as ADR’s in New York in millions of shares per day, and the price will exactly correspond to the Roche share in Switzerland every minute of every day.

Percentage of Swiss sales: 1.1% (of Roche’s global sales).

Percentage of German sales: 5.5%

Percentage of sales in rest of Europe: 17.3%

So… a tiny fraction of sales is made in Switzerland.

We can safely assume that ten times this amount is made in EUR zone (or more).

If EUR depreciates against CHF, that big share of EUR sales will be worth less in Swiss Francs - thus lead to earnings calculated in CHF, given the same prices.

What about costs?

Percentage of work force in Switzerland (as share of global workforce): 13.3%

I don’t know about their cost base, but: We can assume that domestic costs in CHF are disproportionately higher (compared to sales). We could, just for the sake of the argument, suppose that 13% of their cost base is domestic/in CHF - same as the share of employees. But then, these 13% will earn more (on average) for the same work than in virtually every other country in the world.

So how is an appreciating CHF beneficial, if

1% of your sales are domestic/in CHF

…but 13% of your costs are (or, possibly, even considerably more)

…that big share of foreign sales will be worth less and less CHF, the more CHF appreciates?

(This is, of course, grossly oversimplifying and just a means of easy illustration)

I get that from the perspective of the company. And this is why internationally operating companies need to do hedging.

My main question yesterday and today was: Why is something that is relevant for companies (when it comes to cash flows and cost base) not relevant for an individual.

I try to make my thinking process more transparent.

My situation: Swiss resident, earning CHF, want to invest money for the retirement phase, most likely will retire in Switzerland, but not clear yet. But let’s assume so. Means: need CHF to cover my costs.

Before I came across this forum I thought: Invest in ETFs which are traded in CHF. Dividend might be paid in another currency, but I can “consume” the ETFs later to cover my costs. Hence, CHF cash in for income, CHF cash out for expenses.

Then I found quite some posts from people in this forum who just convert CHF into USD and buy VT or VTI etc. at US exchanges - at larger scale in the long run. Not everybody was mentioning whether they will retire in Switzerland or not, but some said so. So I was wondering, why they do not bother about the difference in earnings and cost base as I am doing?

After reading all the posts my conclusion is:

1 - The security you buy is traded at different exchanges in different currencies, it will always be like @Bojack stated: Price in CHF = Price in USD * current x-rate. Reason: Highly efficient markets, arbitrage advantages being levelled out quite quickly. Hence, it would not matter if you would have bought the security in your domestic currency in the first place. But…

2 - It does matter for cash. If you leave the world of the “real stuff”. Imagine you (with domestic currency EUR) sold Roche in CHF in March 2015, but you didn’t immediately convert back the CHF into EUR. Then the “Frankenschock” happened. A few days later you really get more EUR back than before. But it can also be the other way around.

As I will put aside money for my retirement, I just don’t want into a big mess, just because I didn’t try to understand the topic.

And for me reading that people mainly invest in ETF in USD even that they might retire in Switzerland sounded counterintuitive to me. My first reaction: They will expose themselves heavily to currency risk. If they want to retire in a country where their cost base would be USD I would’ve not questioned it.

Hope, this makes more clear from where I’m coming from and where my concerns are.

Also remember that once you retire, most likely you won’t have that much stock, but will have cash/fixed income/real estate in the currency/location that matters to you. (the change should probably be gradual, depending on how much you care about the target retirement date)

I am new here, but have a very similar request as you, at best you can help me.

As a broker I have Cornertrader, there I would like to buy the VWRL ETF. According to the book by Gerd Kommer “Souverän investieren” it does not depend on the currency of an ETF. The VWRL costs something in contrast to Degiro at CT, I can choose the VWRL at four exchanges:

At CT, with these VWRL, the currency exchange costs nothing.

I am Swiss with a CHF account. If I pay attention to the costs I would have to take the “Zurich VWRL”, one more point would be the trading volume to choose an exchange… this looks like this: Amsterdam highest: 31384, Milano:3578, Zurich: 3095, London: 238.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.