Not picking on you specificaly, but generally. The math is super easy. Excel or GPT it.

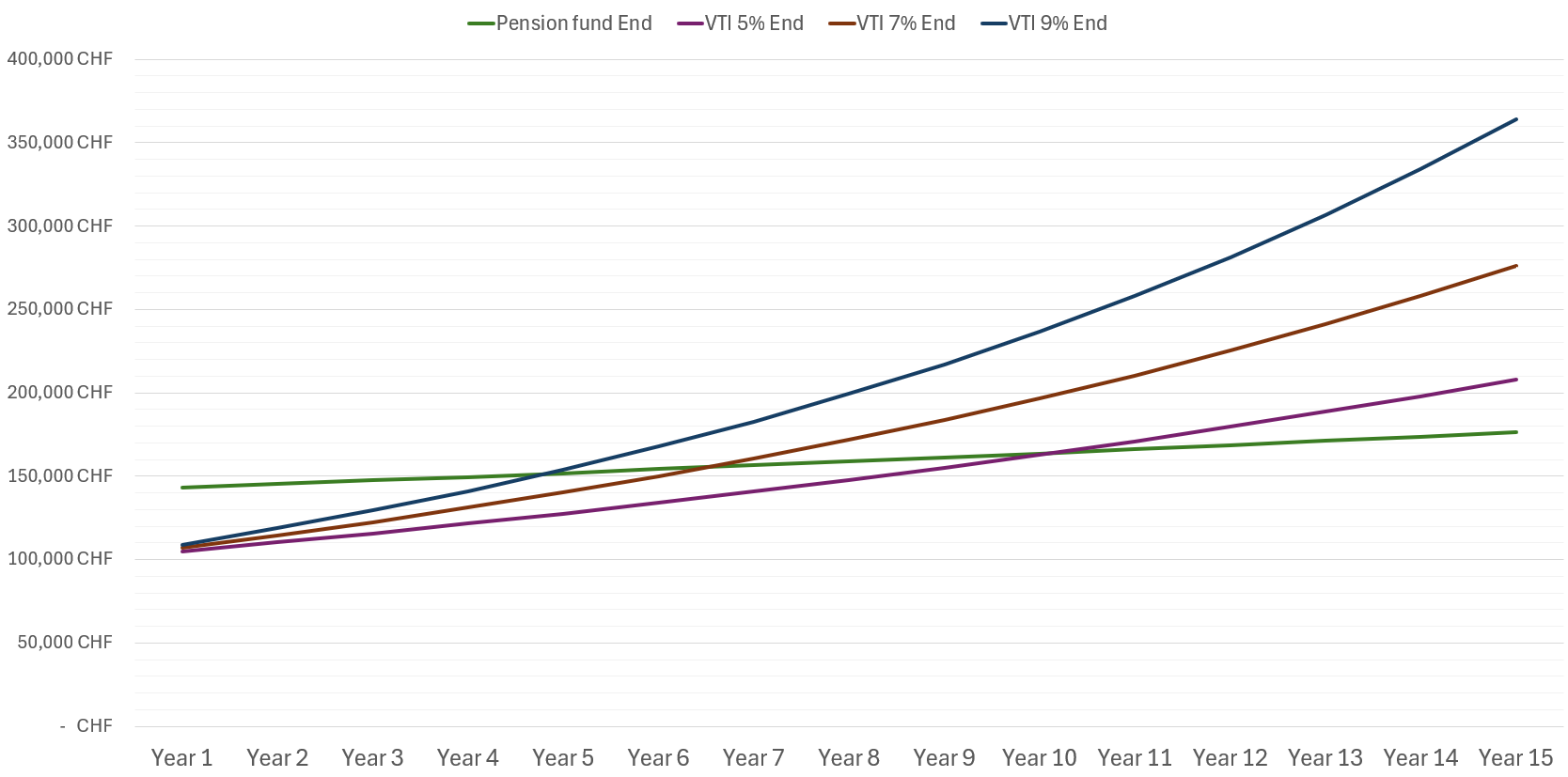

Take one time 100k CHF lump sum. Pensionskasse performance of 1.5%, SP500 performance in CHF of 5/7/9% anually. 41% margin tax rate (hence higher start for PK funds year0). Crossing points at year 5 for 9%, year 6 for 7% and year 9 for 5%. Now make your own assumptions on performance - and NOT in USD but in francs. Add savings on dividend taxes in PK, add savings on 0.3-0.4% on wealth tax in PK. Add savings of using PK funds as pledge for realty. And all your models for stocks assume steady return each year, good luck with that.

Yes, 2nd pillar usually sucks longer term. Sometimes it can make sense. If you are in your 30s and nothing about real estate to live in, invest elsewhere in most situations.

Still not sure what to do. My pension fund has a Deckungsgrad of 140% and will reduce it to 120% within the next 3-4 years. They already gave 9% interest for 2023. So 20% distribution + market returns will probably lead to 6-7% for the next 4 years. No risk and tax free.

I could do big purchases to profit from that. But I‘m 33 and won‘t see this money for ~30 years.

If you have a high marginal tax rate and an exit option (house purchase, early retirement, self-employment) it is a no-brainer to take the tax deduction and 7% return.

My conclusion is that decision to put money in 2nd pillar should be based on overall investment plan. One should consider it as a part of portfolio where returns are lower but more predictable and tax advantaged. At the same time money is illiquid and can only be used for certain things

Personally speaking, I find it very difficult to go all in on stocks. Even though I know their long term potential, I don’t have a stomach to have all my net worth linked to stocks. So I try to balance between 3a, 2a voluntary and Taxable account (mainly ETFs)

In the end investment is not a math equation, it should be a reason to feel comfortable and confident and not worried and sad (if volatility upsets the person).

However if an equation is sought, here is my attempt

F1 = Final amount in taxable account if no 2nd pillar investment was made

F2 = (Final amount in 2nd pillar + taxable account if voluntary contribution was made)

X= amount of contribution under discussion

m = marginal income tax rate at time of contribution

i = net return of investment in taxable account including wealth tax, dividend tax , interest tax etc

p = net return of investment in 2nd pillar

w = net marginal lumpsum tax rate at time of withdrawal

N = number of years to retirement

Yes but what about afterwards? Maybe it’s short-sighted to only look at the next 3 years. This money will be locked and I’ll have to accept whatever return I’ll get in the future.

I have an apartment, but I don’t want to invest my 2nd pillar in it. Doesn’t make sense to save 1-2% in interest and lose out on the return I could get instead.

Self-employment is out of the question. Retirement at least 20 years away.

It was more if you needed it for the 10% deposit. If you move house, you could use it for the new deposit and free up some proceeds of sale. Heck, you work for the bank, maybe they are willing to re-cycle it for you, you pay in from pension and they equity release some of the mortgage back to you.

Or if you change jobs and want to do the VB account shuffle.

In any case, IMO, 7% CHF guaranteed is pretty good. I’d take that over the next 10 years over the stock market. If it is going to continue like that until retirement, I’d put 60% into that as my bond component and have 40% in stocks.

I really have to think about it. Main reason why I dindn’t do it yet: what if I want to retire at 50? Won’t be possible if a bigger part of my net worth is inside 2nd and 3rd pillar as I won’t be able to withdraw any of it for 10 years.

Even if I get to 1 million networth outside retirement accounts and 1.5 million inside retirement accounts. There is a huge risk withdrawing 100k from 1 million for 10 years and hoping it will just work out Of course the 1.5 million inside 2nd/3rd pillar might increase by 50-100% till I’m 60 and then I’m still left with 2.25-3 million, but I could potentially run out of money before 60.

Edit: One solution might be to invest those 1 million in bonds and those 1.5 million in retirement accounts in stocks only (so basically being 60/40 invested in stocks/bonds). But I won’t be able to rebalance.

But if you stop working at 50 you’ll miss 30% of your AHV, right? (15y out of 44) And if you continue working, then you’ll cover your income partially.

@nabalzbhf

You keep paying the required minimum (500 or more) every year to not miss out on years. Then you‘ll get all 44/44 years. I guess my average salary from 20-50 should be enough to get the maximum.

once retired you can easily re-balance. just sell stocks for bonds in the VB account.

nope, because you still have to pay AHV until retirement age and so you will still get those years of contributions. you only really lose out on early years (for those who were not born in CH).

if part of that 100k is mortgage payments, then you can withdraw capital from pension to pay off the mortgage entirely, which then frees up your mortgage payments as additional cash flow.

Or you free up funds to become self-employed. Or in the worse case scenario and you run out of money, you leave the country, cash in the pension and then re-enter the country.

Another risk to take into account is any 2nd pillars purchase after your wedding day will be entitle at 50% by your other half.

It’s a risk to assess or to provision to avoid big surprises at 50 y.o.

That’s the whole point. Make your own graph. On this topic especially people have so many opinions and words yet so few seem to calculate. It’s very straight forward.

The graph does take the margin rate saved - quiting myself: 41% margin tax rate (hence higher start for PK funds year0). Year 0 start of 100k lumpsum is higher for PK. Pension fund growth of 1.5% as noted, using very conservative 1% + 0.5% savings wealth/dividend tax. That’s using my values and assumptions. For a one year one time pension fund contribution vs regular invest savings. If you dont tax a 300-600k yearly income in location XY, likely your tax rate and graph looks different, too.

Edit to add: I added my simple graph as an example, to illustrate two points. First above, use own inputs. Second, yes, in long term it doesn’t make sense for typical 30-40yo. Maybe. Maybe it does Depends on circumstances.

Exactly, it is important to model this out. A simple chart is not fully accurate either as you also have impacts on wealth tax basis of AHV, different rates of tax depending which can change in years because of marriage or children etc. Maybe you even have a more accurate year by year forecast of certain things, returns, interest, salary etc.

That’s why I model everything out in a giant spreadsheet as the interactions are hard to predict. Even a simple question as to whether it is advantageous to stagger pension withdrawals to save capital taxes was not clear cut and had strange breakpoints which showed up in the model, but had no simple explanation as to why a certain number was optimal.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.