Good question. The short answer is no, it wouldn’t be legal. The slightly longer one is: technically, you always calculate the pension according to the fund’s plan rules first (which may use a lower conversion rate, or a combination of two or more), and then you check to make sure that it’s not lower than the mandatory minimum (calculated using BVG salary definition, BVG retirement contributions/credits, BVG interest, etc.). If it’s lower, you legally have to pay the minimum one.

For those cases to occur though, you not only need a salary that has always stayed below the BVG maximum (roughly 86K), but the actual pension plan rules have to be very close to the BVG minimum benefits as well (e.g. ‘contributions’/credits of 7/10/15/18). This is how some pension funds (so-called fully-insured solutions) can get away with using 3 sets of conversion factors as I mentioned above—some pensions will “bite” the minimum, but not all.

Speaking about the conversion rates, if the pension plan states a conversion rate for mandatory and a conversion rate for over-mandatory, I assume they must stick to that at the retirement day? Interest earned each year is another story. It’s only guaranteed (enforced) to be minimum 1% for the mandatory part.

I’m sorry I didn’t go through the whole thread up to the beginning to understand where the discussion about the conversion rate came from.

Depends how many years out you are asking about. By reducing the überobligatorisch Conversion rates, overall conversion rates have reduced steadily the last 10-15 years. Every few (say 5) years the conversion rate for everyone is reduced.

Usually the pension plan will give/work out some solution for those close to pension age (say 58 yo and up) some Übergang/stepwise reduction, so their expected pension doesn’t drop 10% a few months before going on pension.

I’ve seen them magically boost the pension fund of such almost-pensioners by 10%, so that when they drop the conversion rate by 10%, the neo-pensioner still gets the planned pension. For those younger than 55, it’s sorry, you just have to save more, but you have enough time.

Edit: above is only my experience with my pension fund, every pension fund (and there are many) will be run differently. The trend to lower conversion rates (of Überobligatorisch) is pretty common though.

Thanks, I thought it’s not possible to change the rate without the collective agreement of insured employees. This is all BS if neither the annual interest nor the conversion rate is protected by the contract.

I wonder if it’s possible to request a lump sum payout of the over-mandatory part, letting them to convert only the mandatory part to a pension, but I’m rather skeptical, most likely they’ll say “if you want some lump sump payment we will draw it proportionally from mandatory and over-mandatory”.

I don’t know what is more likely statistically, I just know different P.F. handle part-capital-lup-sum part-pension differently. Some take capital from Überoblig first (favours you), others take capital proportionally out of oblig & über-oblig.

This bonus interest was to “compensate” for a future lower Umwandlungssatz/conv. %?

This bonus was out of the PF reserves?

Or the company paid into the PF?

Did the older employees (55-65) get more bonus interest than you?

Pension revision: The first part of the pension revision has come into force. Partial early withdrawal or partial deferral of the pension is now possible for everyone, allowing a gradual reduction in gainful employment. Anyone who works for a salary beyond the reference age can now choose whether to pay pension contributions on their entire income or not up to the exemption threshold.

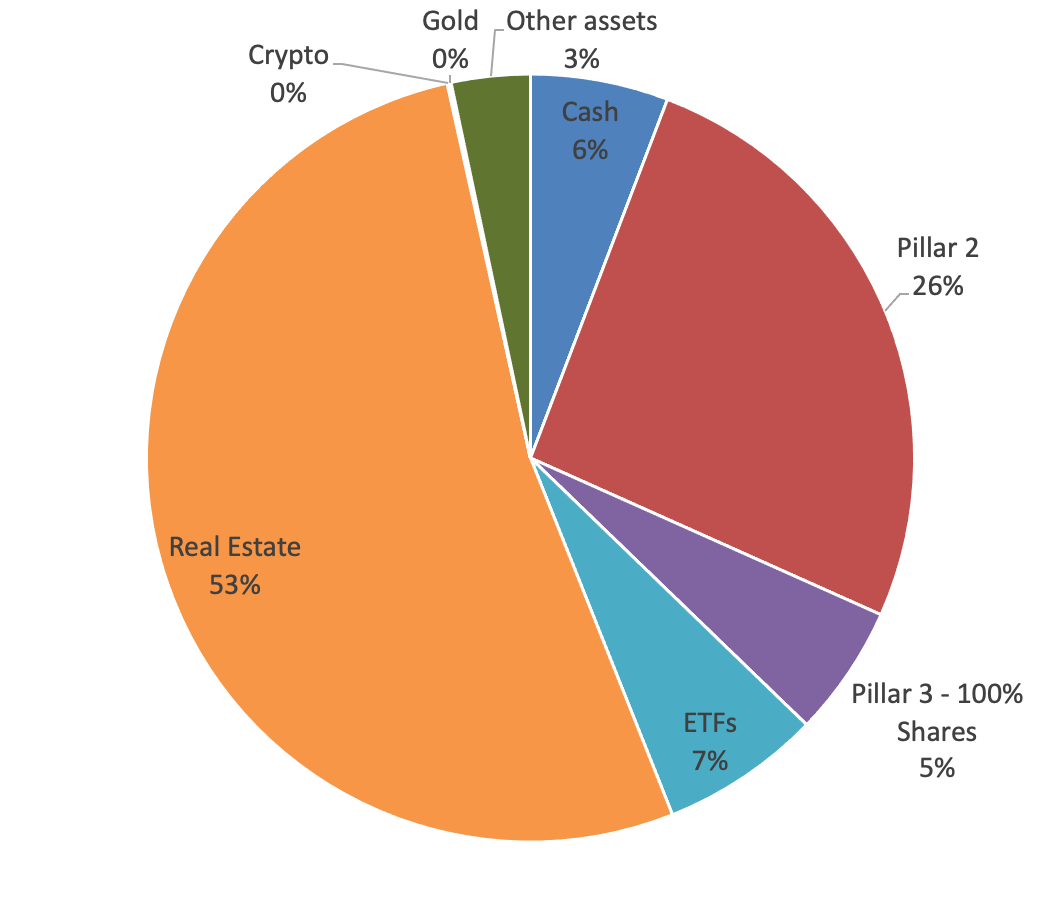

Hey guys - as I originally created this thread I wanted to quickly ask for another opinion. I recently posted my actual net worth in the respective thread - it is 1.8M at the moment. What I realized when comparing my net worth to others is, that a significant portion of the money is stuck with real estate, specifically with our primary home. Now my question:

When calculating my FI number by using my expenses I need 2.4-2.6 Mio. Now how do you assess this when close to 1 Mio is locked in my primary home? Do you think I need to add this 1 Mio and target 3.4 Mio to ensure I have an appropriate withdrawal rate? Obviously the plan is to keep the primary home + I would also be required at some point to further reduce the mortgage when I want to pull the plug … (current value of the mortgage is also 1 Mio)… what are your thoughts around that “issue” with a primary home? Because the money will always be locked there…

Maybe you can share this calculation to make clear what you are doing.

All you need to do is work out how much you need year by year and work out how much in assets you need to generate income and capital drawdown to meet those year by year expenses without running out.

Consider your own home as an asset, assess the actual market rent you would pay for living there and add that to your expenses (since you would have to cover it if you sold the house) as well as the asset’s returns (minus all costs incurred). That means you are willing to sell it if the need arises which, with the 4% rule, is a scenario with real chances of occurring (probably not the most likely but it certainly could happen).

Exclude it of the “ad-hoc net worth” number you’re using to assess FIRE and not count an additional fictive self-assessed “imputed rent” expense. Costs actually incurred for the home, including taxes and amortization (accounted for as a cost since it goes toward something you don’t count as a proper asset for assessing FIRE purposes) should be properly accounted as part of your yearly expenses when assessing your FIRE number.

Edit: in your specific case, since you seem not to be very liquid, I would also make a specific assessment regarding if your liquid assets can carry you to normal "pre-"retirement age (or another situation that would allow you to tap into your 2nd and 3rd pillars) before pulling the trigger.

I would consider the net worth of this asset = 0 ? Or am I misinterpreting something ?

If you have the usual 20% downpayment than you can take that value (or re-evaluate the difference between home current value and mortgage) and consider that amount as part of your net worth…

But also considering that such amount is not liquid and you do not plan to sell.

I’d follow @PhilMongoose 's advice and calculate how much you need to live and where you are planning to extract that amount (selling assets, dividends etc.)

Thanks guys so far for your valuable feedback - appreciate it. Here are my thoughts / comments:

Well - classic calculation, looking at my current expenses (approx. 8’000/month after tax) that I believe we need at a minimum multiplied by 12x25… for us going abroad to FIRE is not an option. We’d like to stay in CH and also in our house - life is perfect as it is and I’d just enjoy FIRE for peace of mind if at some point I’m not in the mood to work anymore or just reduce the workload (which is not possible/worth it in my current role).

Liquidity is not a problem in the future, free cashflow is between 70 and 100k - it looks like that today because we’ve paid 160’000 over the last 3 years into pillar 2 & 3 instead of reducing the mortgage (yes one could say we should have put the pillar 2 piece into ETFs as well to get more interest but we did that to be on the safe side in case there is a need to pay back a huge chunk of the mortgage immediately).

Well not really - the real estate is valued at 2 million whereof 1 million is debt… so if I’d sell it I would have 1 million in cash - it is basically 50% paid off. However, that million is just stuck and there is no real way on how it could generate a return except that living there is cheaper as if we would rent a similar place… so you could say I currently save 30’000 a year on rent, which is 3% interest on an annual basis on that 1 Million… So therefore I think following Wolverine’s logic makes sense:

Makes most sense to me - which means I’d need to add at least 2’500 CHF to my expenses to get to around 4’000 as it would cost at least that amount to rent this property. So overall we’re then at 10’500/month which adds up to a FIRE amount of 3.2 Mio. With our current savings rate it takes about another 10 years to get there… oh well

On the plus side, that number is only 600k-800k higher than your previous one and you get to keep 1M of worth in your assets. That’s a 200k-400k instant (mentally accountable) gain.

Another way of looking at it. The trinity study suggests that if you own bonds and stocks and the expenses you withdraw from them are >4% p.a., there is a more than insignificant chance you will run out of money within 30 years

Your house is not generating an income so your expenses would all have to be paid from withdrawals from bonds and stocks. If annual expenses are >4% of their value you would have a problem

The house will probably increase in value by more than inflation over 30 years so downsizing etc. could be an option

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.