A VT holds probably less than 1% of each of those companies. So basically Wirecard was a loss of max 1% last year and CS will not fail totally so quickly.

That is the beauty of index investing, 7000+ companies for less than a buck. You can’t do much better. Best return per unit of time I would say.

200k in IBKR in VT + 40k in VIAC in Global 100 gives you what, 6.7% Switzerland overall? No issue there.

Currently all stocks in the world have a combined market cap of 90 trillion USD. Wirecard had a peak market cap of 20 billion USD in 2020, that’s 0.022% of the global market. Them crashing down to 50 million market cap hat literally no impact at all.

This was not my point. I was arguing that 40% Swiss equity in a global 3a portfolio is too high. You simply cannot assume that all 3a investors have other assets to bring down the Swiss exposure to 7%.

You can still personalize your strategy to a very large extent, if you really don’t like the preset options and you don’t have assets outside 3a.

That said the preset options are already way better than anything that was available just 5 years ago…

I don’t understand your repeated argument.

It has already been mentioned several times above that you can adjust and customize the strategy (both in Viac and Finpension) to hold as little CH as ACWI (or even 0).

So you can keep the market cap weights, or whichever you want pretty much, both outside and inside of the 3rd pillar.

Those who do the “default” allocation are likewise informed about the distributions, so they can work with that info accordingly (e.g. outside portfolio rebalance).

Sure. Was absolutely not disputing that. Rather expecting it.

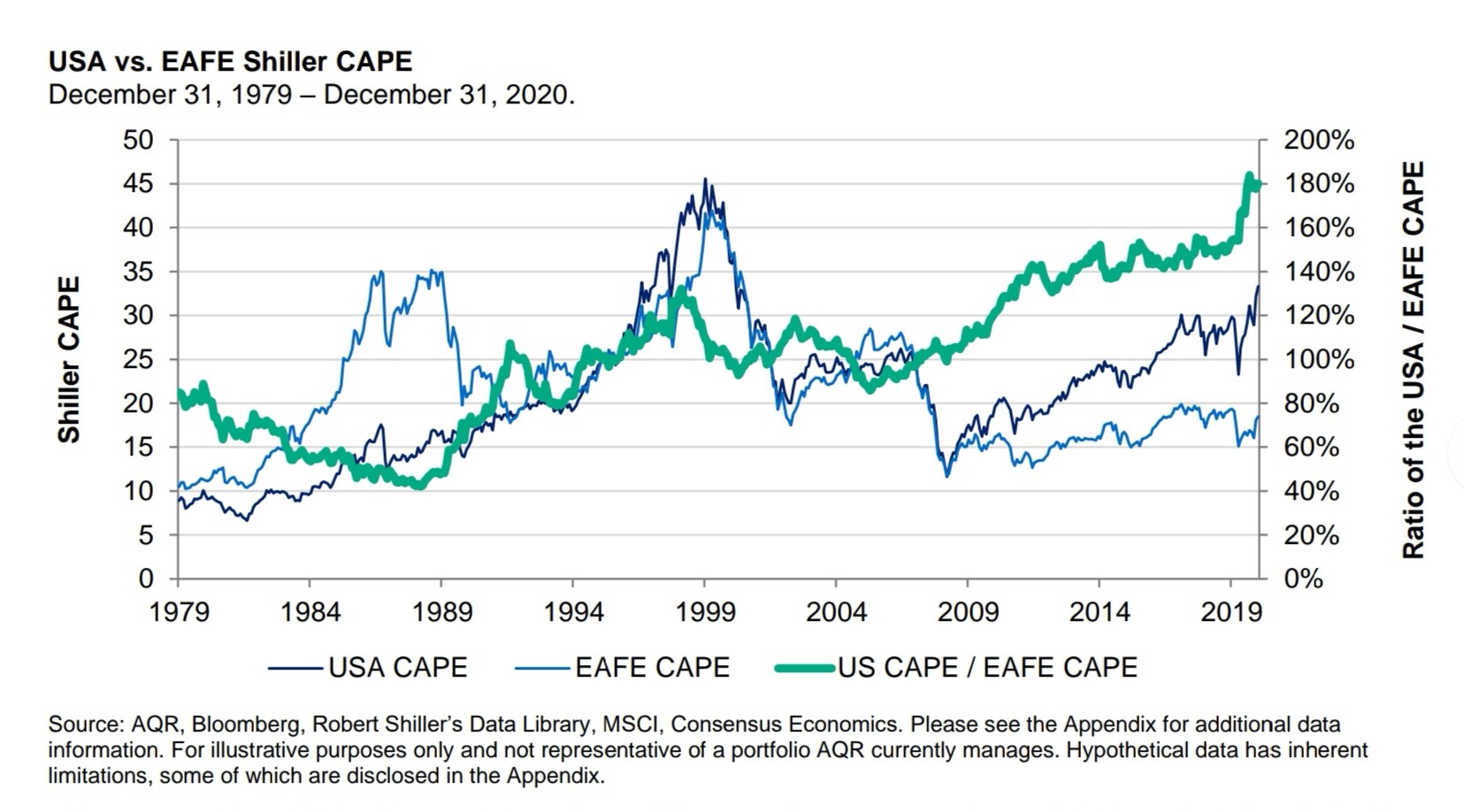

So what’s the take-away?

If the U.S. is not (that) fundamentally superior, then it is overvalued relative EAFE markets.

Investing 101 tells you to that overvalued investments have lower expected returns compared to overvalued ones, all other things equal. So doesn’t it seem reasonable to underweight U.S. stocks and overweight EAFE stocks, relative to a market-cap based allocation.

Sure, the divergence in valuation may last for a long time, and of course it may be hard predicting if and when valuations will converge again. But any guess on that is as good as any other. So underweighting overvalued markets (and vice versa) now seems sensible and (at least in theory) to offer some additional downside protection.

To me, the explanation(s) don’t support allocating one’s investments strictly by market cap.

Is this inflation adjusted return? The USD lost value at quite a high rate(around 3% compared to the chf) so I was wondering if this was already taking Inflation into account.

I’m always wondering what’s the best way to compare these returns. Should they be normalized considering average salary per household per country, cost of life etc. Like you can compare a Swiss guy investing one time 100 usd in 88 in the MSCI Switzerland vs one american again 100usd in 88 in MSCI USA. But what do you use as a basis? 100 usd in chf equivalent would have had a different purchasing power than 100 usd in america in the 88. And the resulting total sum after 33 years may have different purchasing power. Should we look at similar fractions of average salary in 88 to invest the same sum?

In the end you want to know how worse off is somebody in CH vs USA. Can he buy less stuff after 33 years than an american who invested similarly?

I think the easiest way is to compare everything gross in USD returns. MSCI Switzerland had an avg. return of 9.04%/year since 1994 in USD and 7.20%/year in CHF. So summarized something like (in USD):

P/E valuation is not the most important determinant of investment return, ROCE is. I strongly suspect US companies had higher ROCE in the past 20 years vs. Europe

"If you were a great (and long-lived) value investor who bought the S&P 500 at its low in valuation terms, which was in 1917 when America entered world war one and it was on a P/E of 5.3x, and sold it at its high in valuation terms in 1999 when it was on a P/E of 34x, your annual return during that period would have been 11.6% with dividends reinvested, but only 2.3% p.a. came from the massive increase in P/E and 9.3% (80% of 11.6%) came from the companies’ earnings and reinvesting their retained earnings. "

Just a quick update on why I originally started this thread. My pension fund didn’t ever ask for the money, despite knowing there was more when I left the company. It seems that they don’t care.

Those 18k increased to 23k since I invested it in ValuePension 10 months ago. If I get a 5% real return in the next 40 years (when I turn 70), I’ll have 160k real. This small part of my assets will turn out to be quite a nice bonus in my retirement.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.