Hello everyone,

I got the ok from the bank before signing the contract to buy a house (rogito).

I have enough liquidity to cover the rest, but I’m wondering if it makes sense to use one of the third pillars (around 34k) that is sitting doing nothing in postfinance (not invested). If I understood correctly the taxation will be the same now or at the retirement. So I can keep 34k invested (with IB).

Another option would be to use the liquidity (divesting from IB) and move the 34k from Postfinance to Finpension (99% invested).

Unless there are drawbacks I don’t see, the first option gives me more flexibility.

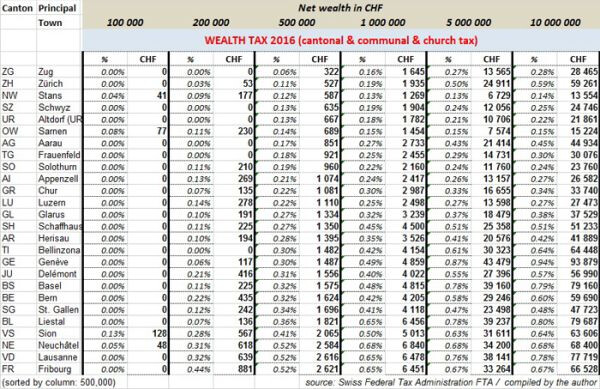

First question: are you living in a tax-expensive or cheap canton?

Looking back at time I and my wife were buying an apartment, I think I should have used minimum cash and maximum 3a for the downpayment. Now I am planning to use only 3a (and maybe 2a) to gradually reimburse the mortgage.

Using 3a for the downpayment is a wonderful opportunity to collect tax deductions and then withdraw 3rd pillar before you are 60. Because of the progressive taxes, you have to withdraw 3a in as many tranches as possible.

Using 3a and leaving IB:

Pro:

Invest with lower fees than 3a products

If you withdraw 3a now, you pay lower taxes than after your 3a investments have been growing for 20+ years. UNLESS maybe you are moving to a canton with much lower taxes before you turn 60 and start withdrawing 3a normally.

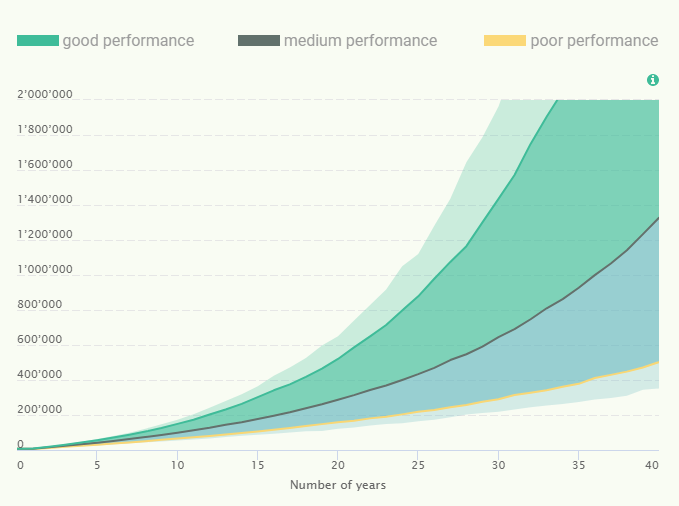

An extra ~1% of annual compounding over 40 years can be huge.

Note:

I assume 40% marginal tax rate on 2% dividends and a wealth tax of 0.5%. Play with the numbers as you like - I am in Suisse Romande.

I ignore the immediate tax savings at marginal tax rate (~40%) of contributing to a 3a since I assume you are continuing to contribute annually regardless.

Counter-arguments:

I assume identical gross returns from taxable vs non-taxable investments. You may disagree since 3a has some limitations on allocations.

Cashing out lower amounts of 3A reduces your tax. For example, VD is about 5.6% for CHF50k withdrawal vs 12.7% for CHF500k withdrawal.

Not sure if I follow this. For dividends you pay taxes, but on 10k they are like USD 50, so I guess you cannot sum the percentages,

As you mentioned wealth taxes are going to be a bit more difficult to calculate, but in my canton I pay not that much after 200k (last year CHF 250 for every 100k after the 200k)

( Note: VT is 0.08% TER)

Yep, I use Finpension

Exactly, the main point is the flexibility to easily change the strategy during the years.

Or during a market crash, I can potentially save a quite good amount of money.

For example, $10k of VT paying 2% in dividends per year is $200. This is taxed at marginal tax rate, assuming 40% would be $80 in tax (0.8% of $10k).

Sure, wealth tax is situational but can add up to a lot if you own all your assets in taxable real estate + equities as they compound over many years. My canton of Vaud is notoriously bad where its easy to get to 0.7% per year in wealth tax just by owning a basic apartment and some ETFs.

True, they are good at reducing fees! Hopefully VIAC/Finpension get more competitive over time and converge to such low rates.

Risky thinking, many try to time the market and most miss out on long term trend upwards + pay high fees to their eager broker. Anyway, you can change your allocation with VIAC on a weekly basis if you are confident

Although, I would recommend leaving at ~100% equities. Over a 40 year career its not unreasonable that your CHF6.8k a year goes to CHF1m.

That makes sense, thanks. Let’s also consider the 15% you can get back.

Very true I’ll try not to do it, because you can be wrong, you need time and it’s not stress free…, but it’s tempting to save some -20%

Micheal Burry and Co. are scaring me a little bit

March 2020 played quite well though

I started quite late with 3a and unfortunately (those are going together) also quite late to do FIRE, but the good thing is that I live “frugal” by design

So we are talking about 34k of 3a ( I have some more with FinPension, but I won’t touch those).

After also your help with calculation, I don’t think it’s going to make a big difference.

Note: To retire at 40 is not going to workout anymore for me

This is just a rebate for US WHT. e.g. VT pays you $100 dividends, US government withholds $15. When you file Swiss taxes you fill the DA-1 and show you have paid $15 to the US. The Swiss government says ok you owe us $25 rather than $40 then.

Either way, you pay your marginal tax rate (assuming 40% here) in taxes.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.