I’d like your comment and feedback regarding the following portfolio distribution, this asset allocation is less than optimal I am aware, but takes into account the current state of the portfolio, the goal is to transition to a less biased one (less Swiss heavy and REIT heavy)

Investment horizon: 20-50 years

Home bias: Switzerland

Investment amount: 3M+

Additionally, despite lurking through the forum, the questions that stand are:

US funds are the right choice to avoid double taxation?

Which broker (I know IB is the best choice), but CT seems the psychological best choice?

I am a bit worried to invest a lot in the same instrument type, I understand the advantages of index ETFs but should I also diversify using active funds to reduce the instrument related risk?

I would simply choose VTI + VXUS for US, international and ermerging and SPI or SLI for CH.

US funds are the right choice to avoid double taxation? Yes

Which broker (I know IB is the best choice), but CT seems the psychological best choice? IB

I am a bit worried to invest a lot in the same instrument type, I understand the advantages of index ETFs but should I also diversify using active funds to reduce the instrument related risk? No

Are you currently with a Swiss broker? CT or other? Keep in mind that selling assets with a Swiss broker will trigger stamp duties, currency exchanges and other potentially expensive events. Think about this carefully and calculate if it is cheaper to transfer securities to IB and then sell, or sell and transfer cash. All depends on your current broker. There are no fees at IB for accepting a transfer of securities.

It may also make sense to diversify brokers, so if you intend to keep a home bias, you could leave some of your Swiss assets with your Swiss broker.

VTI + VXUS or VTI + VEA + VWO bought at IB is the best choice, especially considering the value of assets in question. It’s already at a level where TER matters. For this reason also the Ishares US ETFs: ITOT + IDVE + IEMG are worth considering, as they are even cheaper than Vanguard.

Otherwise it might be a good moment to take profits on your Real Estate fund and to ditch Bonds for cash. The interest rates are more likely to go up than down which (in best case) will see the real estate market stagnate and bonds lose value.

Except for REITs and pure bonds, do you have any suggestions?

In liquid assets (excluding real estate and pension funds), yes. Additionally, by the end of the year it should increase by 1.6M € from some foreign real estate sale (which I plan to allocate at a rate of 100k/month, or maybe even slower, depending on how is the market then, to better cost averaging)

Today is a mix of Postfinance for cash, Migrosbank for equities and private banking for other instruments, fees in the last two cases are bad, even though negotiable, what are my protection on IB?

Excellent point.

Good point, better exposure to small caps, I’ll substitute the international equity portion with ITOT+VXUS

A reduction of the portion in real estate is planned, but I haven’t seen many portfolios here using real estate funds, I understand the high fees and the dividend heavy returns, but are there any other drawbacks?

Make sure you don’t exchange this 1.6M to CHF with your bank.

I did a quick comparison with Migrosbank: https://www.migrosbank.ch/de/privatpersonen/konto-und-karte/fremdwaehrung.html

with rates advertised for 250’000 EUR, they will charge you 0.8% above the interbank rate. This is ~15000 CHF on 1.6M. The same exchange transaction done with IB would cost you 25 CHF (yes, really).

If I’m reading this correctly, you are looking at 5M in liquid assets by the end of 2019. For many here, this is already way more than “retirement” level. Are you looking for a retirement portfolio or do you intend to work and just have this stash grow in parallel?

I’m guessing that you also own real estate as your main residency, which in itself could and should be seen as your exposure to the Swiss real estate market. With an additional 30% in a REIT fund, you’re extremely overexposed in this asset class.

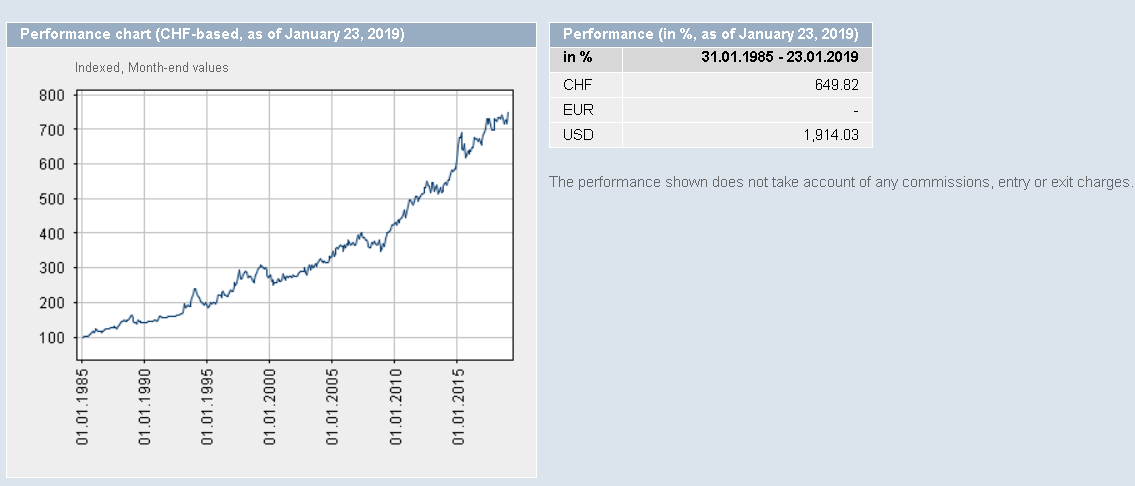

Also, USB conveniently shows only its best period since 2014 and I wouldn’t bet it will continue like that. Look way back since 1998 with data available here:

It is way less impressive with 21.44% over 21 years, so barely 1%/year.

Imagine you had this money in S&P500 since 1998. It would have gained 260% or 12.4%/year in USD or around 8.8%/year in CHF.

There are probably better and more efficient ways to get passive and diversified exposure in Swiss real estate, for example:

I’d be happy to invest with them diversified over several properties.

At such amounts many banks, if you call them, would be happy to stop playing the fool and talk business with you like adults. Spreads won’t be quite as competitive as IB -you’ll be talking to a banker whose time is worth money, not a computer- but definitely not the usual retail ripoff rates

Good luck finding someone competent at Migrosbank. When I was shopping for mortgage, the people I talked to were as bright as clerks in the supermarket.

Both are correct, normally I ask for offers, but pushing the money trough IB might still be the cheapest choice, might even be a good choice to use IB even only for exchange currency at this volumes.

Pricewise probably, but the SIMA is pretty dividend heavy (3-4% yearly currently), average returns for the last 34 years are 6.1%/year, not a terrible deal. Obviously, the returns are eaten into by the income tax. Crowdhouse is an option but the short term forced sale in the next 5-6 years might be more of a hit if the rates go up.

True, haven’t really considered properties in the investment portfolio, I guess logically I should, that would take a bit of number crunching. How should I account for mortgages in portfolio distribution?

It all depends on the expected expenses (my current saving rate on my salary is negative…), MMM would be ashamed, I’d like to improve.

The goal is minimal withdrawal (currently 1% for the next X years, mostly supported by real estate income) while pursuing something fun career wise (pick your job as if they were paying you 0, currently I’m paid roughly 100k), then increasing WR to 3% when soft retiring in 10 years, lots of flexibility.

I reformulated the portfolio taking into account your valuable inputs, and the maybe/who knows incumbent bear market (I’m not timing the market , I’m just being patient) in this:

|Instrument|TER|Allocation|

|iShares Core SPI (CH)|0.1|15%|

|iShares Swiss Dividend|0.15|10%|

|UBS REIT - Sima|0.82|10%|

|iShares Core S&P Total U.S. Stock Market ITOT|0.03|10%|

|Vanguard Total International Stock VXUS|0.11|20%|

|Cash|0|25%|

|SGOL|0.03|10%|

I’d ditch the dividend fund completely and put this into ITOT (and have equal share of ITOT and VXUS). US accounts to 55% of world market cap currently.

25% cash looks like a lot. Also, you might not be able to hold such amounts in CHF interest free in current negative libor environment.

Also think of a rebalancing plan to make your portfolio work long term.

UBS ETF (CH) Gold (USD) A-dis (AUUSI) is 0.23% TER and is listed on SIX in CHF. They also advertise that you can redeem your gold physical. Another (more expensive) alternative with physical gold in Switzerland is the ZKB fund.

With 500k CHF in gold, you may actually consider holding physical bars. With 500k, and TER of 0.23%, your costs are 1150 CHF/year. I guess this is much more than a vault locker in your local bank. Even with spreads on purchase and sale, I think you will be saving money and hold something real instead of paper.

I spent the weekend consolidating all the current positions on a Gsheet (not done yet), and yes very overexposed in Swiss real estate, 1.5M only in REITs + properties.

I also went to VZ for advice (it’s always good to hear other opinions), on top of that started a discussion with several banks because 1.25M in mortgage is coming up for renewal in the next 12-18 months, I can probably squeeze 0.7% for 10 years, which is really cheap money, hopefully, the rates hold just a little bit longer (you can lock in the rates up to 12 months before renewal).

Will wait for VZ to come back to me with a portfolio proposal meanwhile I’ll do:

Analysis of various options in term of costs for holding funds (and opportunity costs tied with mortgage rates), especially negotiable prices, and private banking.

Read further regarding the risks of pure passive investment trough ETF, something so predictable seems prone to risks, I believe a minimum diversification in active funds is necessary.

Stop any further investing while accumulating some cash.

Work on a dynamic withdrawal rate tied with the performance of the portfolio (I’ll crack up Matlab for this)

@959 what did you ultimately land on? any strong insights from vz?

1 Like

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.