Pointing out you are comparing different things is weak?

At the end of the day, past performance is no predictor for future performance.

Pointing out you are comparing different things is weak?

At the end of the day, past performance is no predictor for future performance.

I‘m not even arguing against that. The factors go in that direction als well.

I don‘t think however you can say everything else than US stocks and CH stocks is mispriced by the market (meaning overvalued here). Disregarding whole markets.

There will never be full market efficiency and never full market inefficiency. Grossman-Stiglitz Paradox - Wikipedia

I guess the key question is, HOW inefficient a market is and if there is a cost effective method to exploit those opportunities systematically.

A mutual fund charging 2% must really outperform to cover the cost and beat the index. I think thats very hard for large caps in developed markets.

I guess cheaper funds or active ETFs focussing on small caps or emerging markets may be able to beat net of fees over longer periods. But then again, how to pick the right ones?

I do not believe “hobby” stock pickers beat the market consistently selecting the appropriate benchmark, factoring in cost, etc. Not even talking about the additional time spent managing the portfolio…

The real question is, are there products out there which consistently manage to outperform net of fees? I have been looking at dimensional fund advisors products recently and was quite positively surprised about the track records of small cap equities. Not sure though if/how to incorporate in my portfolio (VT only for my equity allocation currently)…

The challenge I have is that there isn’t an easy way to reduce US allocation without going for multiple ETF strategy. I don’t use US ETFs anymore so VXUS isn’t interesting

Hopefully ex-US ETFs will gain traction soon. It seems right now it’s only EXUS which is executing this.

MSCI World ex CH ETF would be great hopefully someone (UBS) launch it

It isn’t complicated - Avantis and Dimensional have SCV ETFs available through IBKR (AVUV, AVDV, DFSV, DFIV; and Avantis even has a UCITS AVWS one).

Its more in terms of weights, rebalancing intervals, thresholds etc.

So far not a topic with VT only…

Thoughts on portfolio diversification: bought 10% ZGLD a month ago, plugging USD dividends into BRK.B as usual, holding cash to plug into VWRL, hopefully in the next 4-5 months.

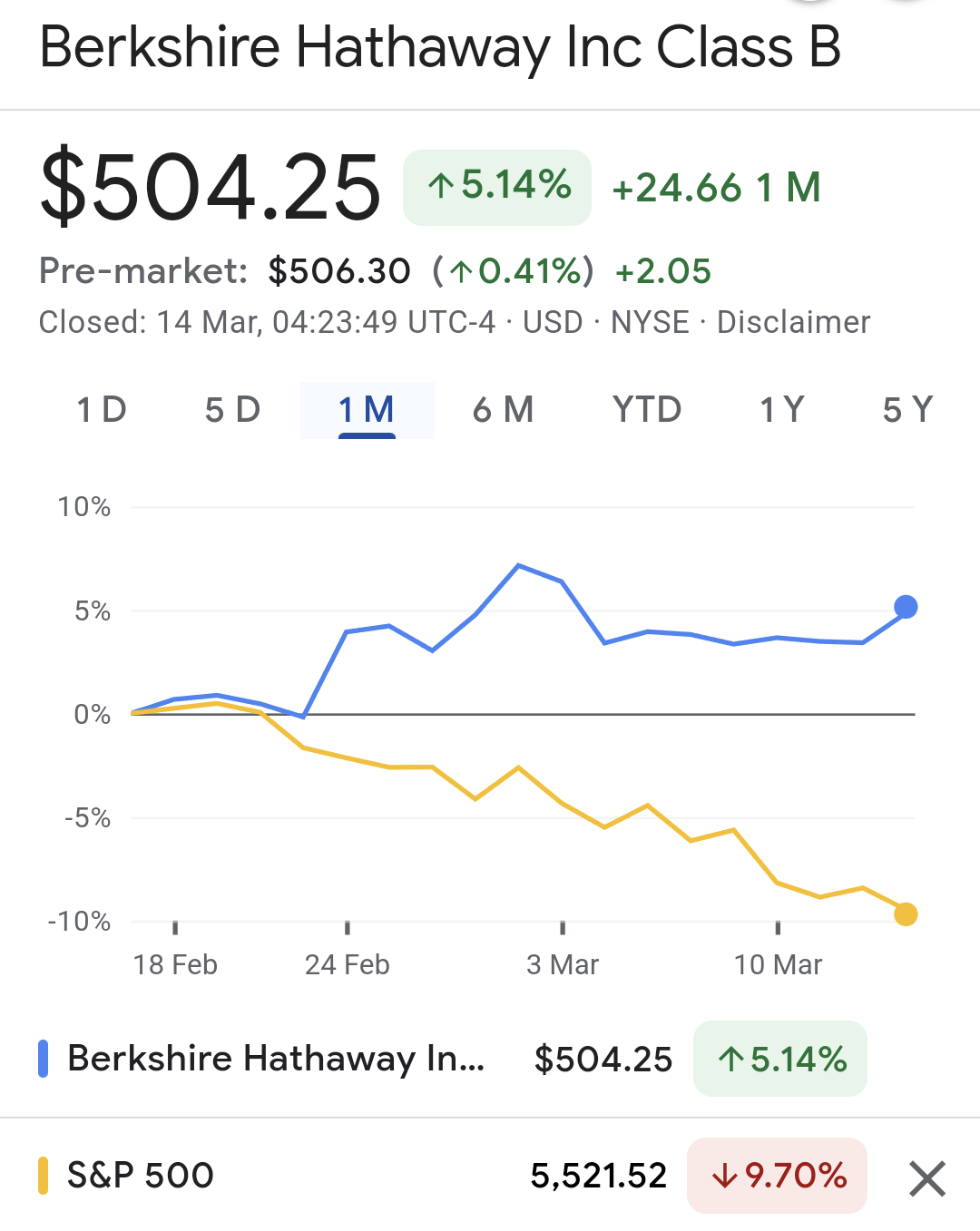

Reddit waking up to the magic that is being a BRK.B shareholder: https://www.reddit.com/r/investing/comments/1jardse/why_is_berkshire_hathaway_moving_the_opposite/

What do people here think of having 10-20% Swiss real estate funds in their portfolio? What are reasons for and against including it?

Arguments for

Real estate is a good diversification method and Swiss RE funds are good vehicle to achieve it. However I think RE funds should also be seen as

a risk asset (like equity) given its volatility.

Real estate tends to be driven a lot by local factors & if Switzerland experiences housing crisis then investing in RE funds can be seen as a hedge against that.

How much is good enough is tough to say. I think it’s best to start adding position slowly and then see. I have about 5% and I think I will try to between 6-10% long term

When I use direct funds, my expected return assumption is the distribution yield & I assume capital appreciation to be same as inflation. This is assuming I hold the funds for significant period of time (20 years) similar to how people hold their own homes for long periods. Any return above that is good luck.

Arguments against

higher exposure to Switzerland. Given that your human capital is derived from Switzerland, Swiss RE could increase your overall exposure to CH. I didn’t refer to 2nd pillar exposure to Swiss RE because where pension fund invests is not your problem, they give you interest in the end and every year and capital is preserved.

There is quite a bit of AGIO in Swiss funds. It’s fine as long as trading happens in secondary markets as participants kind of price the asset. But in the events of fund mergers , this can be an issue for investors (exhibit -: UBS fund merger)

P.S -: I read somewhere that “real” RE capital appreciation in Switzerland has been around 0,9%. Not sure if it was on this forum or another.

Great summary, thanks.

Because you mentioned direct funds: would indirect funds in 3a be better than direct in non-3a?

I think the main advantage of direct funds is their tax structure. 3a is already tax advantaged from income tax perspective.

If one were to choose between direct (outside 3a) or indirect (inside 3a), the main factors to consider are

But I have to say that since higher portion of RE funds (vs global equities) returns are made up of income, shielding them from income tax might be beneficial while keeping equities outside.

So this ETF tracking SWIIT had a dividend yield of about 2.1% last year according to ICTax. Not that different from equities.

EDIT: I thought the 0% TER (usually) of 3a funds could create a more meaningful difference to the TER of their non-3a counterparts in the RE realm which has rather high TER. But 3a SWIIT funds have ~0.75% TER, so no.

I think rather than just the comparison of dividends you should compare the income proportion of total returns

For example if equities have 2% dividend and 3% capital gains, then keeping them in 3a would cause 5% to attract lump sum tax

For RE funds if 2% is dividend and 1% is capital gains then only 3% will attract lump sum tax

In principle a lower total return asset with higher income portion is best suited for 3a.

Yeah. Not much difference.

Can work as a hedge, if you are too concerned about future housing price increases.

In case this is not clear, both, the ETF and the 3a real estate fund, are funds of funds. With the 3a fund you save¹ the 0.25% management fee of the outer fund, but the holdings are exactly the same funds, so you still pay those ~0.72% p.a. for the actual real estate (fund) management.

¹ Well, you pay about 0.4% to finpension or Viac instead, so it’s still more expensive than at a broker outside 3a.

The dividend yield was actually 3.7% last year. 2.1% is taxable and 1.6% is tax-free (already taxed by the direct real estate fund itself).

Edit: This is incorrect as I used the reduced tax value instead of the market value as base. See Thoughts on portfolio diversification [2025] - #85 by justbob

You’re right, I misread the ICTax data.

I think the actual dividend yield is 2.1% as the ICTax provided valuation is also partially reduced. e.g. ICTax value at the end of 2024 is 5.68, but the price on the exchange was ~10 CHF, resulting in ~1.2% (0.12 CHF) taxable dividend yield and 0.9% (0.09 CHF) non-taxable dividend yield on the market price.