Hello to everyone! I’m new here. Hope that my contribution will be of value to the community.

First of all I would like to say THANK YOU to all of the Mustachians in this forum. It is one of the best comprehensive gatherings of serious and well informed people who respect each other!

I’m currently in the phase of finding out whether a 3a pillar is something worth consideration. @Nugget: great spread sheet! Really useful and at a glance vehicle.

I might be wrong, but I think the option of 3a pillar depot (i.e. with VZ) should not only consider tax savings compounding over the years vs fees vs non-3a-investments, but also:

the cushion of 1200/6768 = 17% immediate return on the 3a annual amount should be very much considered as a premium.

annual tax savings should be invested in your broker account immediately (1200 CHF @ 5% avg.)

in the nearest future (most likely) there will be more products available on the market (low costs, better ETF baskets available, etc.). One should not forget that switching between 3a products is possible and should be relatively cheap. The securities will have to be sold though.

swapping from one 3a product to another one in the future with a stash of money x already sitting in your 3a account will boost your CHF returns assuming the product you will be swapping to is cheaper and offers other benefits (otherwise you won’t be swapping anyways)

agree with @hedgehog (one of the past threads on 3a pillar) that the tax benefit is being slowly eaten away by the fees over the years of continuous contributions and hopefully positive returns. If the tax savings are being looked at as separate savings which can and should be invested, than it won’t happen in 8 years or so. According to my calculations this sad break-even is reached after some ±20 years.

I think practical implications of this issue is that it’s better to first achieve FI and then fund 3a rather than the other way round. With Vanguard @ IB we can get faster to the FI number, and then we can continue investing in 3a to optimize taxation (especially the wealth tax). But I’m not really sure if 3a makes sense at all for Mustachians. I continue investing into the @_MP’s recommended 3a fund, but I have serious doubts about it.

Exactly, I have run the number multiple times and only if you are in the high-end tax bracket 3a would make sense. Moreover, with the 3a pillar, you are locked. The state could increase the withdrawal taxes, remove the option to withdraw 3a to buy a house or start a business or remove the option to invest 3a in stocks.

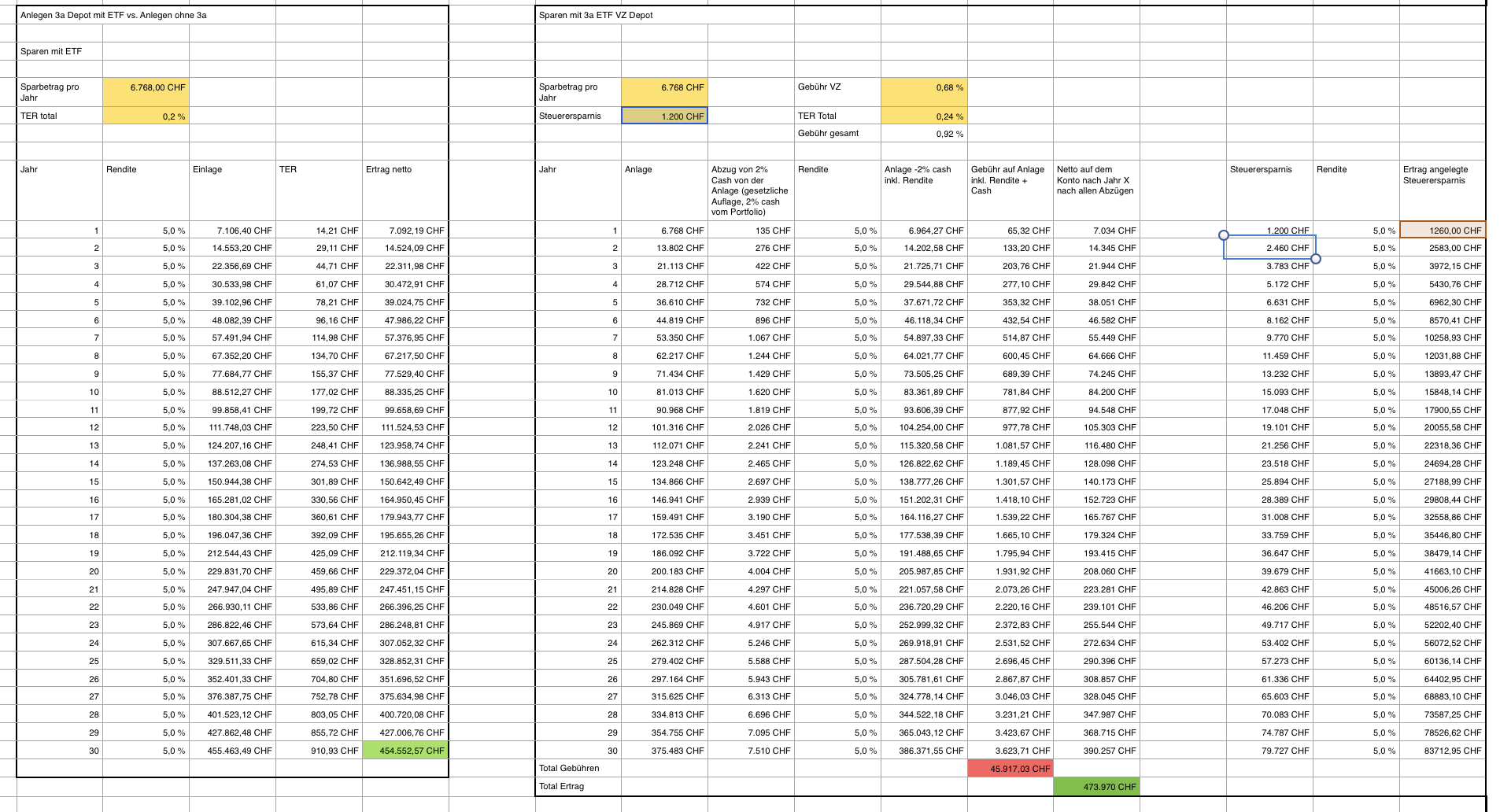

Thank you guys for your replies. I totally get it. I really do One more attempt: I´ve prepared a spread sheet with my elementary school level calculations.

Assumptions:

VZ Total TER (0,68%+ETF TER) = 0,92%. VZ portfolio composition I found in one of the @nugget posts here

Overall Yield 5.0% for (1) IB Depot option and (2) VZ portfolio + investing the tax savings with IB (for comparability purposes)

Tax saving annually 1200 CHF

Total TER of ETF invested with IB depot 0,2%

I do not consider stamp tax, trading costs at IB, Depot fee at IB, dividends (therefore pure capital gains), etc.

Here are my results (hope the picture can be enlarged):

Bottom line is, through “money generation” due to tax saving one can compound OK. Yes, you pay higher fees (in my example around 46kCHF in total after 30 years VZ + ETF TER), but there is 6768 CHF (-2% cash) + 1200 CHF tax savings working for you simultaniously, where without 3a pillar investment “only” 6768 CHF would be working for you. One simply has more money for investing. And after a while you can transfer the stash compounded to a safe harbor - standard 3a bank account with hopefully higher interest rate by then. Please keep in mind that within 3a pillar you do not pay taxes on dividends (to my knowledge), helps the compounding in first place. At withdrawal however one has to pay reduced income tax. I believe it is similar when you withdraw an annual amount x from your IB account at retirement. It counts as income and will be taxed. Correct me if I’m wrong here.

It is however clear that the money in the 3a pillar is locked and accessible only within few scenarios addressed earlier in the blog.

It might be completely stupid to waste time with these calculations, but I (still) believe that there has to be a way to use 3a pillar and currently available products on the market to make it work to your good. Again I think that there will be a better product on the market in the (near) future and swapping from one 3a pillar product to another one is always an option.

Sorry for annoying everyone with this topic again.

Please comment.

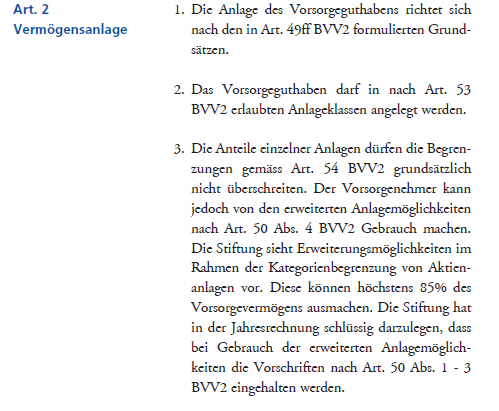

one more add: The T&Cs of VZ talk about max allowable 85% (I thought the Limit was 80%) in stock (Anlagenreglement Art.2. 3. ). Does anyone have an idea on how to reach this percentage?

if they reach 85.000000000001% they have to fix it, afaik. that is why they keep that safety margin of 5%. it was the same with all the BVG45 funds, that legally are subject to a 50% rule, and just use a 5% safety interval.

half a year ago i intensively thought on how to allocate my VZ depot, and the portfolio in my other thrad resembles the outcome.

if they changed anything, please prominently post it here

Are you happy with the results achieved with VZ so far? Do you still think that opening a 3a pillar with VZ was worth it? May I ask what was the return with the referenced portfolio at VZ?

I see two issue with your simulations

-You assume that both investments will return 5%. 3a allows on maximum 80 % stocks and IB can be up to 100%. WIth 100% stock, the IB account will return more than the 3a pillar. I would say 1% more by year.

-3a withdrawal tax is missing. between 4% to 12% of the total capital

My employer’s pension fund invests mere 3-4% in stocks and the main reason they cited me for that is Art. 17 FZG: employees essentially get a free put, the stock market crashes - employer is on the hook to compensate them the losses. I’d take your 50% deal, but double check everything. This is only for mandatory BVG part AFAIK

Another thing is a large portion of pillar 3a has to be CHF hedged and that costs big time with today’s negative interests. Another 1% loss or so for 3a

@Nugget: Are you happy with the results achieved with VZ so far? Do you still think that opening a 3a pillar with VZ was worth it? May I ask what was the return with the referenced portfolio at VZ?

hey castor,

i still believe that within the 3a framework the VZ solution is among the best. however by now i regard my IB/Vanguard depot as superior and stopped contributing 3a.

since i try to be an indexer i don’t particularly look on the returns of my investments. i can dig it up for you next time i check for my net worth calculator…

does it have to be for own use? What if I live in the house for a while and then move out of CH and want to rent it out? I know that for the 2nd pillar they would want you to put the money back in that scenario.

when using 2nd pilla money to buy a property, you will not be able to get tax benefits on additional voluntary buy-ins until you have put back the same amount you took (to fund your own home). Is this the case also for 3a? I mean, if I take out 30k this year to pay my home and then pay the usual ~7K in another account next year, will those be tax-deductible?

Yes, you can take them all out when you leave. So I was curious and asked my pension fund, which assured me that if I leave AFTER having taken the money to pay a property, I would need to pay it back (and supposedly take it out again?). Good to know that this is not the case for 3a though

From what I read and also confirmed by my own calculations, 3d pillar for young people is still losing to the all stock ETF portfolio. This is due to still high cost of it (TER of 0.53%), the cheapest ETF-based 3d pillar today is viac.ch. I think that 3d pillar is in a way a psychological trap that should lead you to think that you save lots of money in taxes this year. It’s a trap of chasing saving taxes today instead of having lots of gains in the future. That’s the classical trick of the financial industry to replace long term thinking by short term thinking.

You’re forgetting to consider that you avoid income taxes on dividends in pillar 3a. Not only swiss taxes, but also US dividend withholding taxes should be 0% for CH pension funds (per 2009 treaty amendment)

Assuming a top marginal rate of say 40%, 2% dividend yield, 45% non-US weight with 15% lost to non-US withholding (actually probably much less, as there are similar treaties with other countries) that the fund wouldn’t be able to recover, it’s slightly beyond breakeven:

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.

One more attempt: I´ve prepared a spread sheet with my elementary school level calculations.

One more attempt: I´ve prepared a spread sheet with my elementary school level calculations.