Very targeted question,

Where in the ZH tax form can I insert maintenance work done to my property? (I have the receipt with the description of the work: painting, insulating window, polishing the floor, etc)

Very targeted question,

Where in the ZH tax form can I insert maintenance work done to my property? (I have the receipt with the description of the work: painting, insulating window, polishing the floor, etc)

The quoted statement is wrong. Foreign dividends are taxed in Switzerland for Swiss tax residents. Foreign withholding taxes will be accounted for as per double taxation treaty rates via DA-1 but foreign dividends are still taxed here.

Targeted answer

Go to Liegenschaften, click the row with your property where you declared the value etc. Go to section „ Unterhalts- und Verwaltungskosten“

Normally you can claim Standard deductions . But if you want actuals, you can uncheck „pauschal“

Thank you! That worked

You may also want to check what else you can add.

I understand that if you use actual cost instead of flat rate, you can also deduct things like building insurance.

Non-refundable foreign withholding taxes, that is.

If you are eligible for a refund of (part of, or conceivably all of) withholding tax from the country of source, you can‘t list that part in your DA-1 to receive a Swiss tax credit on it.

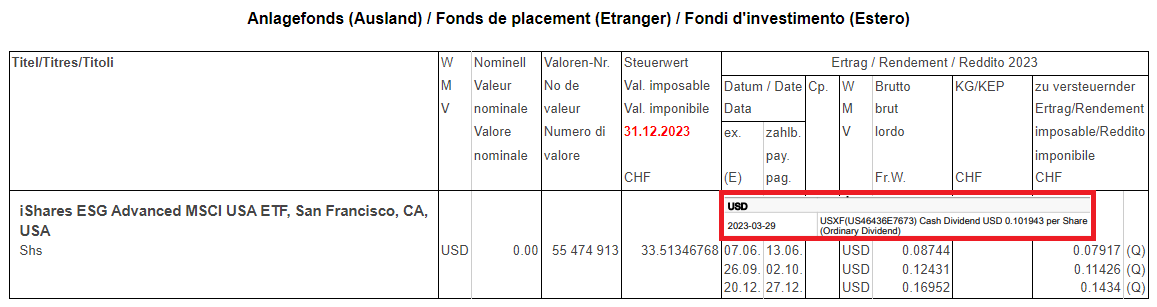

I think I found the error. ICTax is missing one quarterly dividend on this particular ETF USXF.

Therefore it underestimates the annual revenue by 0.102 USD per share.

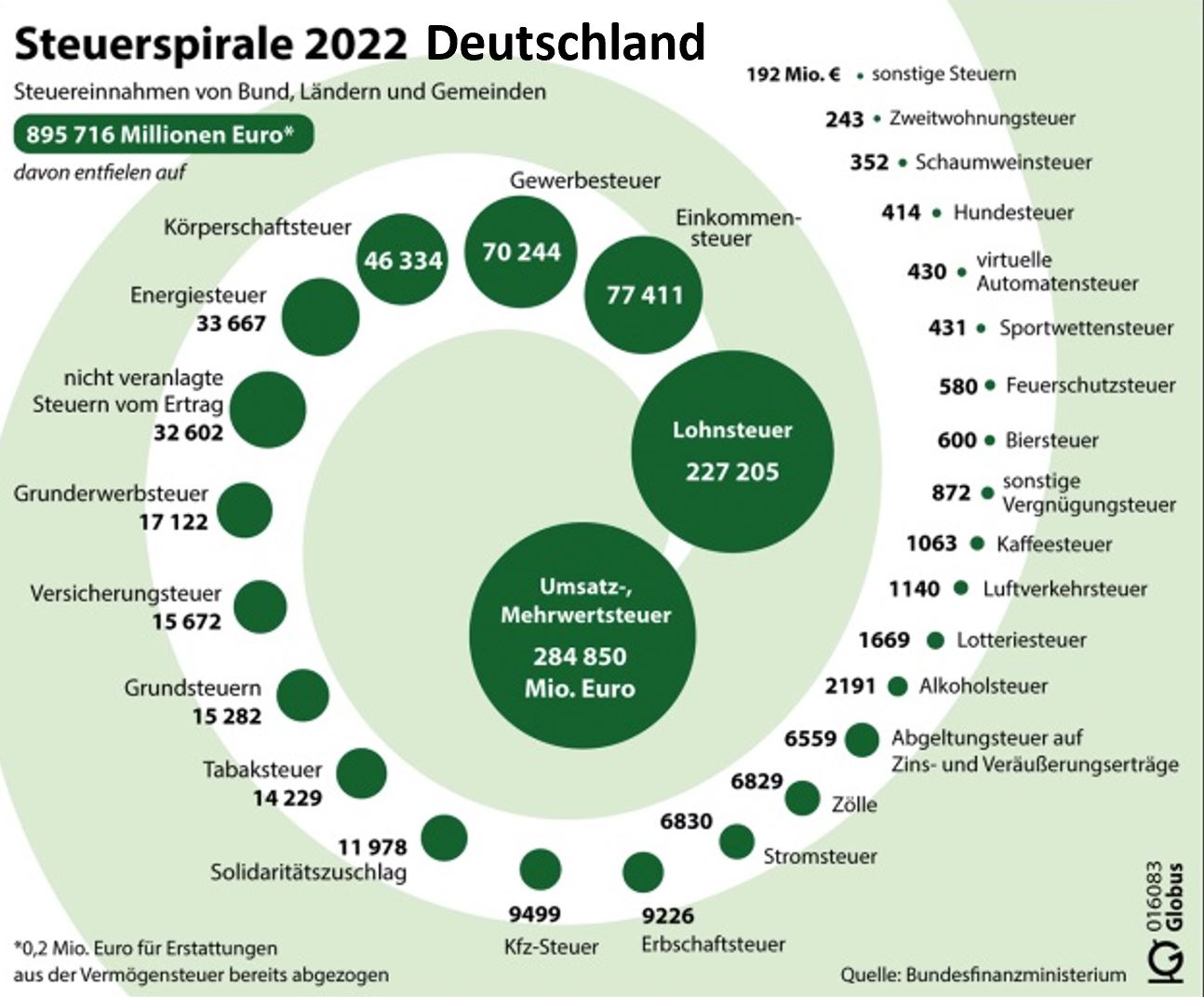

I was curious about these (and the before mentioned) taxes and created the following graph. In 2022, the total tax burden on productive Swiss residents was CHF 156,412,000,000, which is CHF 28,500 per tax payer (assuming 5.5 Mio Swiss individual tax payers and roping legal persons in).

I am using this to argue that an FIRE person is still adding a lot to society, even when no longer contributing with income tax.

In Germany, for example, the VAT has become the predominant tax.

Thanks a lot for the blog post; it is really helpful and clearly organized.

Is there also a post here regarding structural tax optimization for private individuals in Switzerland (I haven’t found anything in the extensive blog yet)?

I don’t mean the typical tips like pillar 3a, mortgage interest, or deductions for continuing education. I mean real (legal) optimization — surely there must be options, right? Establishing a family foundation? Foreign loans, perhaps? Could we brainstorm and crowdsource some ideas here?

Switzerland is pretty nice, there’s no need for weird setup (there are minimal amount of tax deductions which avoids encouraging complicated setup with no economic benefits)

If you want to get lower taxes just move to a low tax Canton ![]()

Edit: to understand why it works this way, swiss courts define tax avoidance as any setup that does not have economic motivation beyond tax benefits.

Source: https://www.walderwyss.com/assets/content/publications/230206-Switzerland-FINAL.pdf

Tax avoidance is constituted if:

a. the legal structure or transaction chosen is unusual, inappropriate, or inadequate to its economic purpose (objective element);

b. tax motives are the only reason for the structure or transaction chosen (subjective element); and

c. were it accepted by the authorities, the legal structure or transaction would lead to significant tax savings (effective element).

A bit old, but Einkommens and Lohnsteuer should be one I would say, and that would make it predominant again for Germany.

It‘s just separately listed in Germany.

Yes, it is basically the same thing but differentiates between what is deducted from peoples’ salaries at the source (Lohnsteuer) and from what self-employed people and people with income from Real Estate have to pay.