Thanks for your answers, really appreciated. I tried to chew all of those tax-related topics, but I guess I was at the end lost in the jungle of the comments.

I think my situation is pretty simple, like at any other expat’s here in Switzerland:

Now:

Tax residence CH

Permit B (started the second 5 years in 2019)

Income below 120k

Savings rate between 40-45%

Plans:

No plans to buy a property in CH (only outside of CH, maybe in the next 5 years)

No plans to buy into the 2nd pillar

Stay for the next 15-17 years here (planned 13-14 years to FIRE)

Retire outside of CH

Savings:

35% 3rd pillar

42% US stocks (mainly VTI)

23% cash

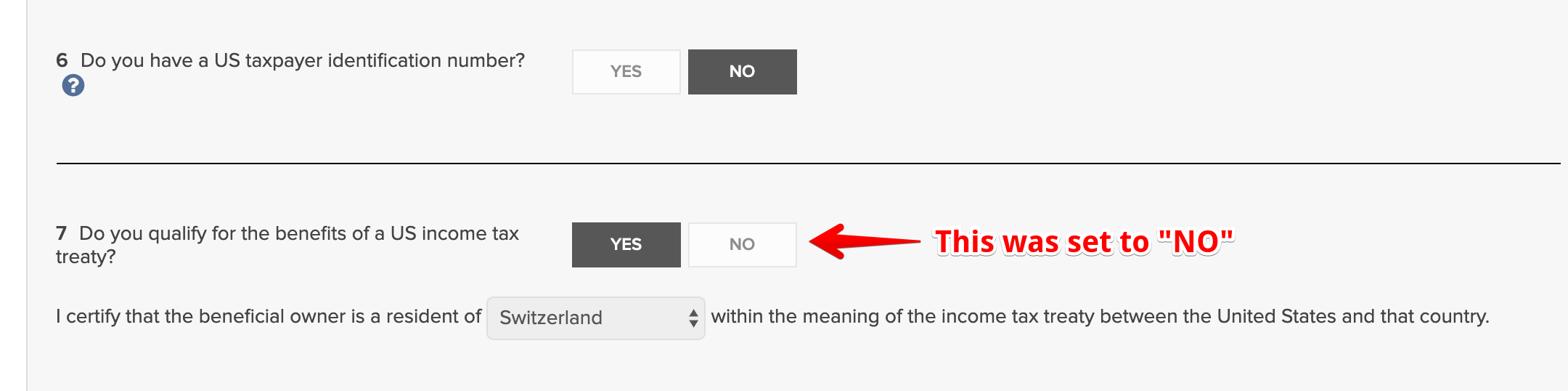

I want to keep it simple, and don’t want to overengineer it. But with the time as my portfolio grows, I just want to keep my withholding tax on my US dividends as low as possible. (I’ve already tried to file the W8-BEN at InteractiveBrokers, but they told me I’m fine. But I can still recognize 30% withholding tax on my dividends at IB)

You should double check this, as they basically already take care of the 15%, and only 15% is taken from your dividends.

I believe that you registration process (stating you are not a US resident) kind of “counts” as that W8 form, and is handled accordingly.

I certainly have only 15% taken away from mine.

On B permit why do you have to file taxes if below 120k income? Isn’t that detrimental when living in Zurich (where the city tax is higher than the cantonal average)?

(that said if > 5 years in CH, with a German passport the C permit should be a formality due to reciprocity agreement).

No it’s not fine. If you’re swiss resident you just declare this fact with W8-BEN and they must withhold only 15% per swiss-US treaty. File a ticket and demand them to fix it, you have a right

Okay people here’s the point that really grinds my gears.

Let’s Say you reach FI (Quit your job, just live form your assets). In my case stocks and you still wanna grow them. In my simple understanding they will automaticly classify you as an “gewerbe mässer wertschriftenhändler” because you can’t fullfilly point 3. (You are not emplyed anymore. You fill that with your taxes)

You do not depend on the profits from trading your securities in order to finance your household expenses. Rule of thumb: the profits from trading should make up less than 50% of your total net income during one tax period.

(see link below for the hole paper)

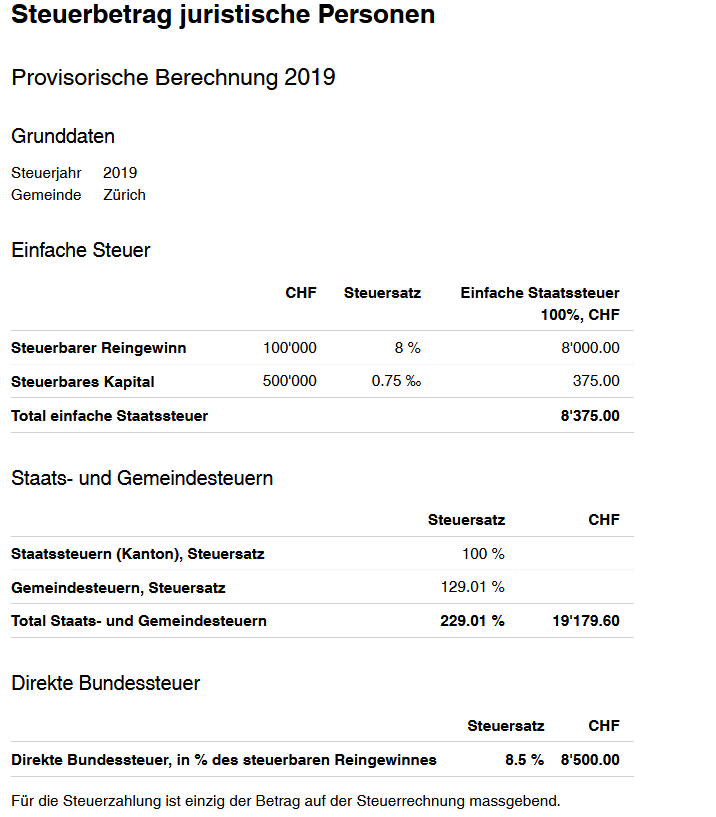

Therefore you will be professional trader. Which means you have to pay taxes not just on your capital gains, also on the market value of your stocks.(stocks gain in value,. Obvioulsy you pay taxes on the assets. See attached bsp.

Extract form the 642.11 Bundesgesetz über die direkte Bundessteuer

1 Steuerbar sind alle Einkünfte aus einem Handels-, Industrie-, Gewerbe-, Land- und Forstwirtschaftsbetrieb, aus einem freien Beruf sowie aus jeder anderen selbständigen Erwerbstätigkeit.

2 Zu den Einkünften aus selbstständiger Erwerbstätigkeit zählen auch alle Kapitalgewinne aus Veräusserung, Verwertung oder buchmässiger Aufwertung von Geschäftsvermögen. Der Veräusserung gleichgestellt ist die Überführung von Geschäftsvermögen in das Privatvermögen oder in ausländische Betriebe oder Betriebsstätten. Als Geschäftsvermögen gelten alle Vermögenswerte, die ganz oder vorwiegend der selbstständigen Erwerbstätigkeit dienen; Gleiches gilt für Beteiligungen von mindestens 20 Prozent am Grund- oder Stammkapital einer Kapitalgesellschaft oder Genossenschaft, sofern der Eigentümer sie im Zeitpunkt des Erwerbs zum Geschäftsvermögen erklärt. Artikel 18 b bleibt vorbehalten.1

So every year you pay (in this example zürich) 0.75 ‰ every year.

And if you have a good year, your stocks go up you pay 8% on your earnings. maybe you could do something with building reserves (Rückstellungen) in an up year and reduce your income that way. And in a down year you could free the reseves (Rückstellungen) them up???

In addition the 10.25% AHV.

So you should have some cash on hand for that, that you can’t invest.

I’m no tax expert but this is the way I’m seeing this as today.

No, this conclusion is definitively wrong. It only means that you are not guaranteed to not be classified as a professional trader, i.e. the tax authority might want to have a detailed look into your activities.

However, with the typical FIRE mind-set / buy & hold strategy you will definitively face no issue with your tax status. If you are in the grey area, doing quite some trading but also not overly sophisticated, you simply face a higher level of scrutiny, but the outcome of the judgement will/should be the same independent if you are retired or not (so it is probably easier to slip through the cracks if you are still employed).

Please search the forum, this has been discussed before.

One more thing: from what I know, profits from dividends are not profits from trading. So if your ETF pays 2% dividend, then you can sell another 2% or even more, because what I understand as “profits from trading” are capital gains. So if you buy a share for 100 and sell for 400, thats 300 capital gains.

To recap, I see this point as: you might have to pay capital gains tax if more than 50% of your income comes from capital gains (sell price - buy price). Dividends however are taxed with income tax and so they count separately.

The thing I’m not sure about is the way they count capital gains. If I sell a share that I held for 10 years, will they calculate the capital gains from the purchase price waaay back, or only from the start of the year? Anybody knows this?

They simply wouldn’t - this entire “rule” is built around day/short-term-traders, and itself from precedent in the court of law. Selling long-term holdings to cover your living costs is just plain old retirement spending, not an “occupation”.

But in many countries they tax capital gains every year. So if I hold some shares for 10-20 years, or maybe even I keep buying a little every month, then how will they calculate capital gains once I finally decide to sell a portion of it? Do they count it on FIFO or LIFO principle? Do they take the original purchase price, or just the price at the start of year?

Because capital income is not subject to taxation at source.

If you do have capital income, this is subject to supplementary ordinary assessment, and you would have to file a tax return accordingly.

It depends on the jurisdiction and taxation system.

FIFO should be a common principle, Germany has been doing this for years, as far as I know, calculating from the original purchase price - can probably get a bit “messy” if done manually.

I read up on this just recently from published judgements. And indeed most are referring to realized capital gains based on FIFO principle. It is generally you that has to prove the original purchase price, the tax authority will be forced to make assumption if you don’t. Strangely, there seems to be quite some leeway. The tax authority cannot just assume a ridiculously low purchase price and force you to prove otherwise, they by law must assume something reasonable, but it really could just be an assumption and not an actual calculation the judge accepts (of course you can/would always prove otherwise if the estimate is not in your favour).

Then again, no one will try to tax you on something you have held for 10 years.

New user but long time lurker here, this forum has taught me a lot so far!

The time for tax declarations is approaching and I need a complete noob treatment from you since I couldn’t find any detailed guidelines online on how to do my taxes. I did not start a new thread since this may have been asked before and this thread seems appropriate. Here is my situation:

Permit B holder, single

<120k income (Quellensteuer, never did a tax form before)

ZH based

This year I started investing in some standard ETFs (IWDA, EMIM etc.) with Degiro.

I also contributed in a pillar 3a for the first time with finpension.

First, I understand that tax has to be paid on the dividends, no matter if the ETFs are accumulating or not. So, if my reasoning is correct, in a 10k portfolio with a ~2% dividend yield (according to the MSCI World index fact sheet) one would have to declare 200CHF dividend income, and then for a hypothetical 10% withholding tax tariff expect something like 20CHF in taxes, which sounds pretty low. Is this right?

Second, can someone give me a step by step guide for the tax declaration? Do I need to declare my portfolio? Which form/fields would I need to fill in? Where to get them from and where to send them? What tax rates should I expect?

Third, also some guidance on how to claim back the taxes from my 3a contributions would be really welcome.

I’m probably being thick, but am I understanding correctly that capital gains are really tax free? To be extra clear, I bought bitcoins for 10$ and now they are 40k$ a pop, I can sell them and incur 0.- tax due on the 39’990.- profit? Same goes for shares or bonds I bought while living abroad and sell at a profit while residing in CH?

I do think this is correct. But you might want to be careful about the amount of profit you take at once. There is some rules to follow to not be considered a professional trader. If you are considered a professional you might get taxed.

I hope you declared it all the way since back when you bought them, otherwise they‘ll want to know where you have all the money from and potential fines and past wealth taxes slapped on your wrist.

If not, do a self declaration (which you can do only once) before submitting the tax report! This should reduce potential fines for tax evasion

Holding an asset for years does not sound anything like professional trading, we should definitely stop questioning the “but I might get professional status” all the time.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.