As complicated as this gets, it would make for a good example of another @anon95353169 calculator.

Like entering projected taxable income in the next 10 years (+ canton) and then suggest when and how much should/could be postponed rather than paid immediately.

If you have a salary raise of 5%, it might not be worth to pay the previous year immediately, but you have to wait until 9 years later etc.

However, it gets very complicated and many variables may change within the timeframe of 10 y. So ATM, I would probably not intentionally postpone, unless there are other factors in a given year that prevent me from paying in.

If you don‘t pay into 3a in 2025 and delay it to 2034, you‘re missing out on 2k tax savings that could have been invested and probably doubled in that timeframe.

What about independent workers?

My wife use to make 70k a year and contribute 14k on Viac 60 world.

Will it be capped at 7’500 per year as employees?

We have just bought a house that we are gently renovating the next 3 years. Moreover she is currently pregnant and will reduce a bit it’s activity before the child go to school.

Since we will deduct some of money already as rénovation cost+child care I think it would be a good idea not to contribute for 3 to 4 years.

Maybe just a bit like 300chf a month 100% equities just in case the crazy bull run continues

The independent workers will only be able to buy back the small Pillar 3a contribution for the lost year, i.e. CHF 7258 for 2025, for example. The law makes no provision for buying back more than the small Pillar 3a contribution.

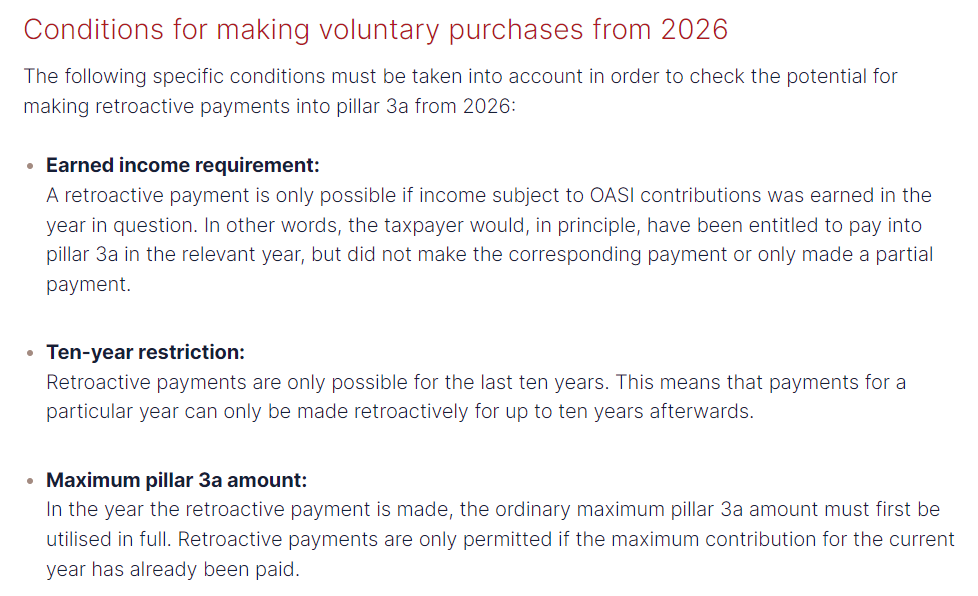

I’m not sure how this works in practice e.g. let’s say I don’t pay any 3a contribution in 2025. Then I decide I want to pay a 3a contribution in 2026. Do I have to pay 2026 contribution before paying the older 2025 year or vice versa?

What if I am not working in 2026? Does the eligibility for the 2025 year rest with the working status in 2025 or 2026 or both?

This seems to undercut one of the reasons for the measure. I thought it would be of most use for those who became unemployed and so couldn’t contribute in one year due to lack of funds etc. and then able to rectify later on.

Unemployment benefits are subject to OASI and you’re allowed to contribute to 3a during that time. So I don’t see an issue (unless you’re unemployed long enough to no longer get any benefits).

But even a short job during semester break solves this. E.g. you work for 1 month in the summer and earn 4k, then you could skip 3a buy-in and wait until end of studies.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.