Hi!

I wasn’t not sure, if I should start a new thread or ask my question here, since the title is super fitting :).

I am also new to investing and am trying to figure out a suitable portfolio for me. I like the Boglehead approach…

On this site I found some nice portfolios using ETFs. They seem to always use the same fund source. Is this some fee optimisation? The rebalancing might cost less, when using the same source?

Does anyone know more about this?

Yes you’re right I had a wrong number in my mind. Compared to a many different brooker and IB was definiticely a cheaper one. Still with low money invested TW is a convenient good choice in Switzerland in my point of view. With referrals you only pay 0.25% fee. TER with my portfolio is 0.15%

Let me chip-in. I started investing for the first time ~2 years ago and after evaluating many options I decided for TW. Through research I knew that IB and other options were cheaper after reaching a certain amount of money invested (there’s actually a good post in this same website), but for me personally TW had a lot of advantages:

IB is cheaper only if you are ready to lump-sum invest large amounts. With TW you can use dollar-cost-averaging and the fees are included in the 0.5%. Since I wanted DCA for the peace of mind it gives me (I know that lump-sum is actually better, but it was my first time investing and with DCA I feel more confident in case of a big crisis). With TW I can DCA relative small amounts without paying exorbiting fees.

At the time I wasn’t sure if I was ever goint to pass the threshold were IB and other brokers are cheaper than TW, and even if it was, it wouldn’t have been for some years.

TW gave me the confidence also regarding taxes. I had never invested and had no idea how to file taxes, and no one to ask for (without paying). With TW I get a document and instructions for how to file my taxes.

The company made me a great impression. Before investing I have sent an email called “2 questions about investment start and fees”; it ended up being a 50+ email conversation about all the questions I had. The support was amazing in answering all my questions, and it continued even after I invested with them. The guy from support even invited me to grab a coffee, and I was only investing the minimum to join them, I am not a big fish or anything like that.

If you want you can create your own portfolio (it’s what I did), I asked them a list of their ETFs and picked the ones I wanted in their app. My total cost is 0.61% if I am not wrong. In my personal opinion ok for my situation described above.

TW definitively helped me pull the trigger on investing for the first time by giving a lot of confidence. I can not recomend it enough if you are in a similar situation. If you are a seasoned investor with relatively high amounts to invest, ready to lump-sum it, then go with IB or other brokers. If you’re relatively new, want to DCA and/or in general don’t plan to invest that much, then TW is a good alternative, at least for starting out.

p.s. if anyone is interested write me for the referral, someone already mentioned it, it’s 50% off on 1 year of fees, so only 0.25% + your TER.

I submitted by mistake before finishing writing.

I know this is mustachianpost, but still not everybody is ready or able or willing to lump-sum invest huge amounts. I just shared my experience with TW, I think it might be useful to someone.

Read my last sentence: TW was good for me in my situation and I believe is good for anyone in a similar situation, which seems to be the case for azreal. That is, if you are a small investor, starting out. If you’re a seasoned big investor than IB is definitively better.

Correct me if I’m wrong, but the reason we are on this forum is to learn and share the best practices of managing our personal finances.

I also started with True Wealth, although with only a demo account. I also created my own portfolio. Looking at it now, I managed to underperform SMI, MSCI World and MSCI ACWI all at once. Lucky me I didn’t go live with this portfolio.

This forum as well as bogleheads convinced me to invest individually. First with CT (expensive comparing to IB, but oh so intuitive and easy to start with). I guess you can go with any broker you chose. The main contributor to your future wealth is your savings ratio and spending habits, not broker choice which is only the final touch.

If you are below 25 the threshold is even lower (3$/mo maintenance fee), I did not do the math but I am pretty sure it is below the minimum balance of TW.

I also started with TW and then started investing directly with Saxo (genius move I know, but I rejected IB at first cause I though I could not invest with an US broker). I later moved both over to IB.

@Kilbim

I think TW is a good choice for someone who just wants to turn a risk dial and put some money in, if you already went through the trouble of picking your own assets you might as well do it yourself.

Don’t you pay a lot in fees?

It depends on what is your “small amount” obviously, but if have a portfolio with 5-6 different ETFs and you want to invest in all these each month you end up paying a lot with most brokers. BUt I don’t know what IB charges, so it might be low, even for small amounts (lower than 1000 CHF a month)

I just bought my first stock 58 of VT for the time being and I plan to buy some amount at fixed intervals.

Do you suggest buying every month or maybe like once every 3-6 months?

I’m still trying to understand some things in the interface:

can I buy fractions of shares? I found myself with a few CHF and a few USD after converting USD.CHF and buying the shares

can I see the fees that were paid for my purchase of the ETFs?

It’s exactly other way round. IB is much cheaper. Normally I pay few bucks (max $2-3) for my monthly transactions (including forex costs which are ridiculously high in all other brokers and banks).

As others have said - fees can run down to 0.35/transaction (with tiered pricing).

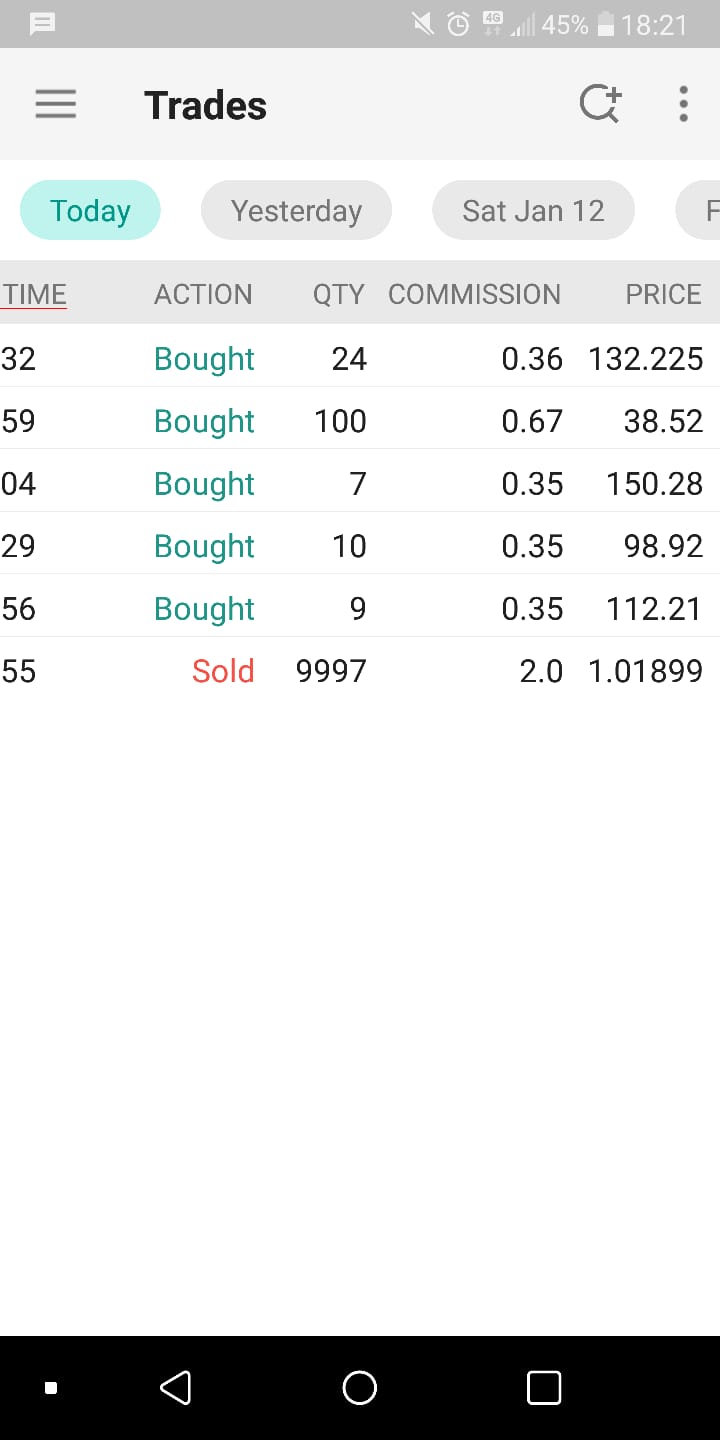

I just yesterday bought 10k worth of shares of 2 ETFs (VTI, VEA) and 3 individual stocks - and below are the fees.

(bottom one is from CHF-USD conversion)

Not as far as I know. Just leave them until your next buy in.

Yes, in your “Trades” section of the app, as below.

At the moment my equity portfolio is made of VTI + VXUS. However these ETFs are not available anymore on DEGIRO and I’m trying to replicate the same exposure with european funds.

(The reason I’m not simply switching to IB is that I’m far away from the >100k necessary to avoid fees on IB, and 120CHF per year are too much for me, and more than the difference in TER. Also, I’m not 100% sure that IB won’t prevent US ETFs as well in 1 year).

For the US I thought that Vanguard S&P 500 (VUSA), although with much fewer stocks, should give me similar exposure to VTI with low TER.

Is there anything similar to VXUS that is available in Europe and that mustachians recommend? EIMI looks good for EM, but anything for non-US developed markets?

Which multiplied by 12 months anyway ends up being 120CHF per year. At DEGIRO most of these ETFs are commission-free. With the tiny size of my investments this ends up being more than the difference in TER between european and US funds.

Once a month comission free, then more expensive than IB, also if used for European funds. And don’t forget 0.5% currency exchange fees on Degiro … and the commision free list is not that interesting IMO.

If you insist on Degiro, stick with Vanguard VWRL. You can get additional exposure to world small caps with VIAC, but you have to keep in mind that VWRL follows FTSE All-World Index, while VIAC has MSCI index tracking funds.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.