The premium for private insurance is ~200 fr per month. In case of RE, 60-70k CHF Net Worth needs to be set aside to pay for this assuming a 3.5% SWR

In my case it is much less than 200CHF per month… around 70-80 with 0CHF franchise in Aargau.

A switch to private costs about 1000 CHF per day

Is it so little? Does it include the costs for an operation and everything?

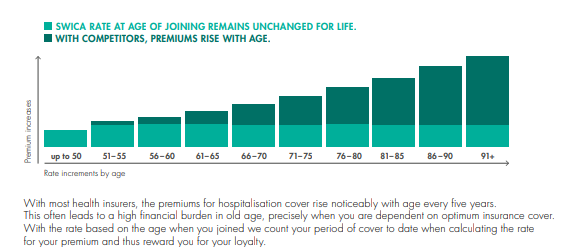

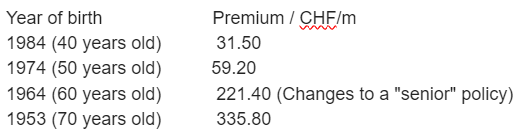

I spoke recently to an advisor, who told me that the premiums you pay are fixed for life. e.g. Sanitas 30 years old 0CHF franchise is 77-/month in Aargau for life. It sounds weird to me because if I were 60 the premium is 331-/month, which results in a much higher overall premium (let’s say you live up to 90 yo, it is 55k vs 120k CHF).

Where is the catch?

That would be an unusual model. But the catch of that model is: The premiums you pay for unused insurance during your younger years compensates for the low premiums you pay when you are older and actually using the insurance. It’s kind of 6-of-one, half-a-dozen of the other.

Supplemental hospital insurance only covers what is not covered by mandatory insurance. With many of these offers, you are paying for more privacy, and possibly free choice of doctor. The actual medical care is covered by mandatory insurance. The hospital insurance offers that add coverage for private clinics are generally expensive.

Thanks for all your feedbacks, it’s very helpful. I’m close to apply, probably for the private, but I have still some doubts.

I’ve been told the premium you pay will stay the same for all your life. e.g. with Sanitas private I have 80CHF/month, will it really stay 80CHF/month for all my life? The person told me that in case it increases I can close the contract, but of course that’s not what you want. How can I be sure that when I will be 80 they won’t double it?

Are there significant difference between providers that I should be aware of?

I guess I should also be careful in choosing an insurance company that is expected not to fail in the next 50 years. Am I right? Is is something to be concerned about?

Yes, I can see that, but still from my calculation you will spend much less over a lifetime (55k vs 120k if you do the insurance now vs at 60 yo and you live up to 90 yo). Am I missing something?

Note: SWICA hospitalisation insurance and deductibles seem to be more expensive than other insurers. Seems likely customers <50 are subsidizing loyal customers >50

True, but it also covers more private clinics than many other insurers.

The real value in a supplemental hospital insurance is in the coverage it gives you that you do not already get from mandatory health insurance. The cost of treatment in the general wards of hospitals on your canton’s list is already fully covered. So supplemental insurance only covers the difference in price from that to whatever perks they include. They do not cover the treatment itself, as that is covered by mandatory health insurance.

The difference in price between a general ward and a semi-private or private room is relatively small. For stays in private clinics that are not on the canton’s list, on the other hand, mandatory insurance covers just under half the cost, so supplemental hospital insurance plays a much bigger role. So you can’t really compare hospital insurance that only covers listed hospital with hospital insurance that covers private clinics. They’re almost two different things.

I did wonder about that, how small is relatively small? Do you have any more information here? My assumption has been about 1000 CHF per night in the University Hospital Zurich, which I took from an old SRF article. A very rough assumption, but I’d find this difference rather expensive…

Thank you very much for the pointer on Swica. It looks like the only one that offers that service (that I found at least).

The amount saved over a lifetime is huge, I don’t understand how they can guarantee fixed prices with potential inflation, etc…

They also seem to offer this copayment of the basic insurance.

One more thing:

In the Swica leaflet they mention " Short waiting periods for scheduled operations" but then I cannot find anything more. Helsana and Sanitas were more specific indicating e.g. max 5 days for a medical examination and a possible second opinion.

Do you know anything about that? This combined with the choice of doctor is probably the most important thing for me.

I think as long as I understand the best treatment is for those with Private Worldwide (BestMed). It looks like you have a faster access also in semi-private but probably less fast.

Note SWICA told me they also apply the copayment if your basic insurance is with another provider. You need to send them the invoices and they take it into account (but please do your own research)

No. Interesting how Helsana and Sanitas can guarantee that as is it depends on the availabilty of the Dr ( what about vacations?) . I assume it means they will just direct you to a different Dr

We had a seminar at work with SWICA and an independent insurance broker. The question was asked how restrictive the SWICA Basic Insurance Medpharm model is (obligation to call Sante24 health line who make a plan which is binding) and is there a conflict of interest to choose the cheapest provider, would it stop you choosing a Dr (example cancer specialist). The answer was that it was not a problem at all. In practise all Drs at hospitals are covered. I tend to believe them as SWICA rely heavily on their reputation for reliability and customer service.

I’ve seen that Swica private world offers what they call the BestMed insurance card, which if I understand it correctly is the top service in terms of speed of treatment and advice.

I’m leaning more towards it now.

I still don’t understand why the private world with BestMed costs only 10 cents more than regular private which is not world and does not have BestMed. I don’t know if I’m missing something important.

I am not a specialist in insurances, but I am good with probabilities. Check if this insurance covers you only as long as you stay a resident of Switzerland. If this is the case, as I guess, an extra value of you getting a medical treatment more expensive than in Switzerland while traveling abroad is rather small.

That’s a good estimate. What I meant was that the markup for semi-private/private is relatively small in relation to the total cost of hospitalization, which easily runs into tens of thousants of francs.

Here is an example for the cantonal hospital in Luzern:

The daily basic flat fees for a general ward are:

Acute treatment: CHF 2500

Rehabilitation: CHF 1000

The markup for a semi-private room is CHF 500 on top of the general ward price.

The markup for a private room is CHF 650 on top of the general ward price.

It means if you have private hospital insurance with 5000 CHF excess you won’t get much back from the insurance company for short hospital stays in Switzerland.

With such a policy you are covering against long hospital stays or for hospital stays in countries where the health care costs are higher (i.e. USA … in that case you need to check your coverage is global )

I guess there is a “soft” point too: if you want to be admitted to a private hospital and pay yourself, without any guarantee from an insurer, I assume you have to provide proof of funds or an advance payment…

I’m also currently deciding what I need. I’m nearly forty years old, perfectly healthy and have a semiprivate hospital insurance, with a supplementary insurance that allows me to upgrade to private without a health check.

I could save CHF 1000 per year if I would downgrade the above package to general hospital insurance, again with the possibility to upgrade to semiprivate (but not to private) without a health check. The semiprivate option includes the ability to upgrade a stay to private where I’d only need to pay 25% of the upgrade costs.

And now I’m undecided what to do. I’m thinking I could downgrade, upgrade to semiprivate in 20 years, and upgrade individual stays to private if I’d feel like it. Hell, even with the general option I’d be able to upgrade a stay and pay 25%/50% of the upgrade costs to semiprivate/private. And I’d save at least CHF 20’000.

I allow myself to riff off the existing topic, with a bit of a different tune.

My wife [insert Borat sound] will be moving over to CH these days.

We are generally healthy and plan on taking out the 2’500 franchise for both.

However, anticipating that she might get pregnant in the coming months, I was considering whether to take the semi-private instead of the general ward hospitalization supplemental insurance.

Primarily because of the free choice of doctors (obstetrician etc.), but also for a bit more “luxury” when staying in during those (hopefully) few days.

So I got a few questions:

Timing the package: Could the bump from general to semi-private be done “in the future” (e.g. from 1.1. only, or once we know we are expecting)? I would expect there might be some “delay in activation” from the date you upgrade.

Does semi-private actually bring much “privacy” benefits in Zurich city public clinics? (How “big” are the rooms, I wouldn’t know yet)

How big could an “out of pocket” payment be for an ad hoc bump to semi-private just for those few days? (I read ~1000/day somewhere up there)

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.