So far, I understood you wanted to ask for a theoretical discussion. But it seems you have a concrete example.

I think you need to distinguish between theory and practice. LifePlus from VIAC is a unique offer (at least to my knowledge) and not available from any other provider, so there is no point about theorizing. All discussions then should focus on how to hack (or not hack) LifePlus.

Happy to be proven wrong on this.

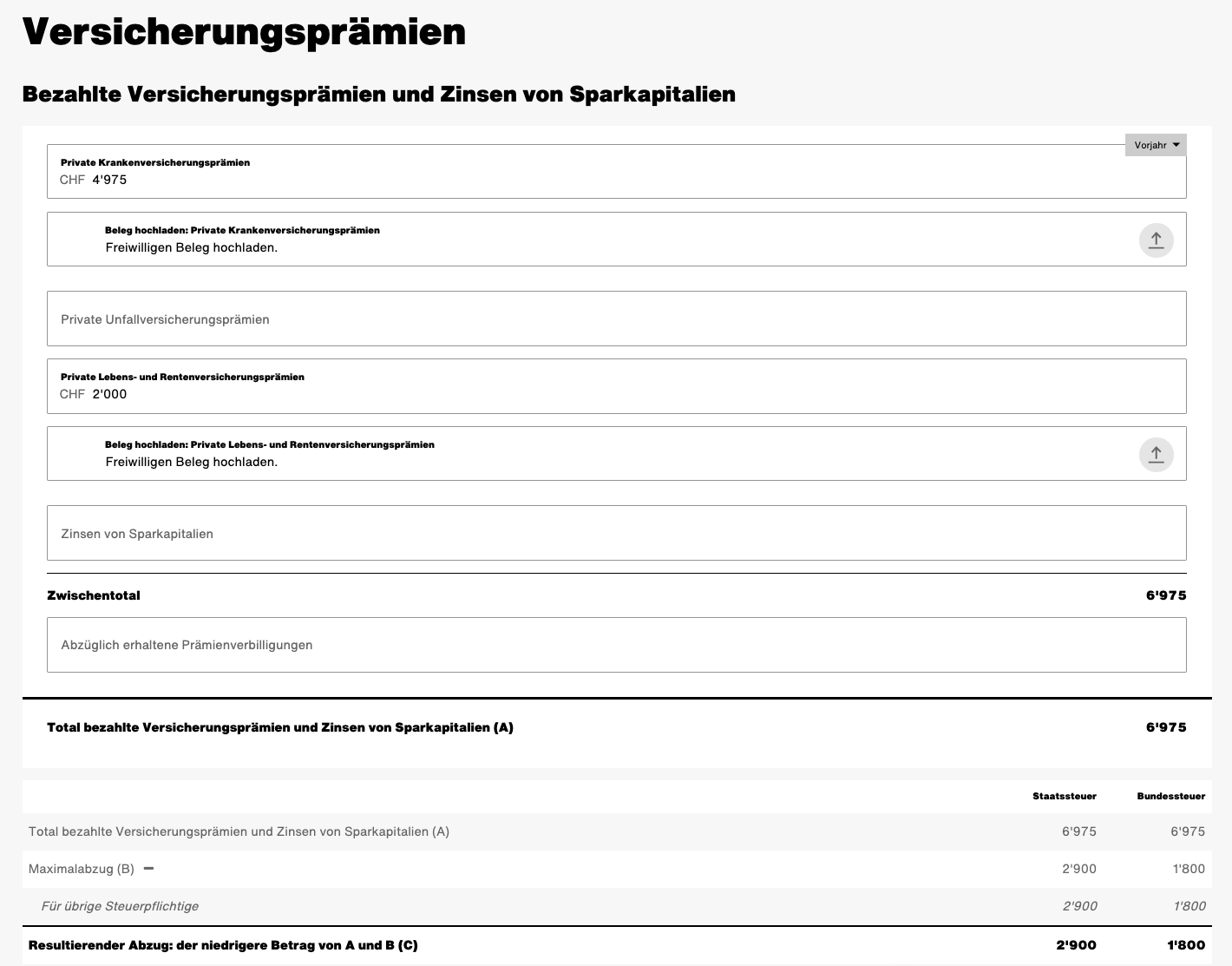

I’m filling it up with just my health insurance. See attached. (The Fr. 2’000 is just for illustration, I don’t have life insurance). So yes, no tax benefits on life insurance.

As a side note: I don’t think personal liability or household are deductable. At least, I don’t consider household or liability insurance as ‘Private Lebens- und Rentenversicherung’.

Oh no, I was not talking about LifePlus. I have a risk-only life insurance from Zurich, and I got the option of paying the premiums either on 3a or 3b.

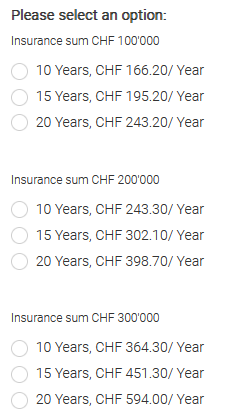

Here is an example of pure risk life insurance not linked to any 3rd pillar account (3a or 3b). You just have to pay a premium to be insured. I receive a bill per year, that’s all.

OK. For my clarification, am I correct in the following?

Paying the premium into your 3a is a special deal that is not available to the public.

Paying the premium into 3b is the same as buying milk in the supermarket or paying for a flight. It reduces your wealth tax but has no further tax implication.

In that case it’s still an interesting thought experiment for me, even though I will not be able to make practical use of it

Just to be sure, you have this product? I think what is happening is that you are indeed paying into a pillar 3b of the insurer, but this is completely transparent to you (from your point of view, you are just paying a bill). This is exactly my case.

I think paying into a 3a is quite standard practice, it’s not a special deal, actually as I said most tax advisors recommend it, I have not seen any insurance that does not offer you the possibility of paying life insurance premiums in 3a.

You are basically right about 3b, from your point of view it’s just a normal expense. This is, mind you, provided the 3b account you are paying to is not yours but, e.g. the insurer’s. Otherwise, if it’s yours, I’m not entirely sure if there can potentially be cases where you can “lock” the funds in a similar way to 3a, maybe not but I’m not sure about fringe cases.

EDIT: or, as @Ardius pointed out, it might depend on the canton.

Correct, this was also common ~10 years ago when I arrived in Switzerland. It was (is?) such a plague that by now the oversimplified “insurance in 3b = scam” has entered common folklore to the point that it has become very diffcult to have a serious conversation about it.

You’re right. However, technically speaking it’s not ‘paying into a 3a’. You pay the insurance premium in the same way as you pay your phone or electricity bill. Then you list the insurance expense in your tax declaration under 3rd pillar. This is my understanding when reading the Axa website.

Periodische Prämienzahlungen bzw. Einzahlungen können unter der Rubrik «Beiträge an anerkannte Formen der gebundenen Selbstvorsorge (Säule 3a)» deklariert werden. Hier beträgt der maximale Wert bei Privatpersonen CHF 7’258, bei Selbständigerwerbenden CHF 36’288 pro Jahr.

This is actually a fantastic option that I have not been aware of until now. I’m therefore repeating the tax advisor in your first post:

You pay the insurance premium to the insurance company (not into your 3a account)

You invest the remainder of the Fr. 7’258 into the best possible 3a solution (Finpension, Viac, …)

Your get the full 3a reduction of your income tax (reduction for Fr. 7’258)

At retirement you withdraw less money from 3a, therefore paying less withdrawal tax.

If you have additional money available for investment, that’s great! But it’s not part of the above setup. Of course you will pay wealth tax and income tax on dividends for this investment. But your total investments gains from this additional money far outweigh the taxes.

In other words, don’t consider the insurance premium an investment. It’s an expense, just like milk or eggs at the grocery. But, other than milk or eggs, you can fully deduct this expense from your taxes.

If you can afford to max out the pillar 3a for retirement savings, doing that is the most sensible option. The reason is that, while the initial tax deduction is identical for all pillar 3a contributions (retirement savings, term life insurance, etc.), the long-term tax benefits are bigger for retirement savings because assets in the pillar 3a do not count towards your capital wealth, and interest/dividends do not count towards your taxable income.

In this case, you can use pillar 3b term life insurance, which has the benefit that you can name any beneficiary you want. If your tax deduction for insurance (health insurance, life insurance, disability insurance) and interest yields is not already maxed out by your health insurance premiums, then you can add the premiums for pillar 3b term life insurance to that deduction.

If you cannot afford to max out your pillar 3a allowance with retirement savings, then getting pillar 3a term life insurance can make sense, as the premiums can be added to the pillar 3a tax deduction. However, your choice of beneficiaries is limited to what the pillar 3a allows (spouse, children, etc.).

Thanks for challenging my statements! I took this opportunity to dive deeper into the topic. My new conclusion: I largely agree with you. The only exception is the period of 7-8 years before retirement. If you start your life insurance at that point, it can make sense to deduct the full 3rd pillar but not pay the full amount into your 3a account.

You can find my assumptions, thinking and calculations on this spread sheet: https://1drv.ms/x/c/71E9FB80E3006555/IQCtdm-qh0ngSJ7br6v_AimTAaVWdkzrbtfprN5601l_9vE?e=Ky05S8

I believe one would need to run actual numbers because the initial tax benefits are not exactly the same.

Assuming the premiums are an obligatory expense, the cost of the 3a option is proportional to 1 + r while the cost of the 3b option, 1 / (1 - r), where r is your marginal income tax rate.

Once the withdrawal tax for the investment 3a is taken into account, paying the life insurance through a 3a becomes even more attractive.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.