I saw one or two rental deposit discussions from other posters, hopefully this one has enough value to exist on its own.

As you might know, having money sit in the deposit account is terrible. The other option - insurance/Mietkaution - is also expensive if it is even accepted by the landlord. But what’s the real difference? This was the question I had recently after putting all of my accounts in YNAB and seein a 5-figure sum sitting there doing nothing.

So I made a calculation, the numbers aren’t exactly my situation but they are close enough. The equation works even with my numbers so consider this the generic version.

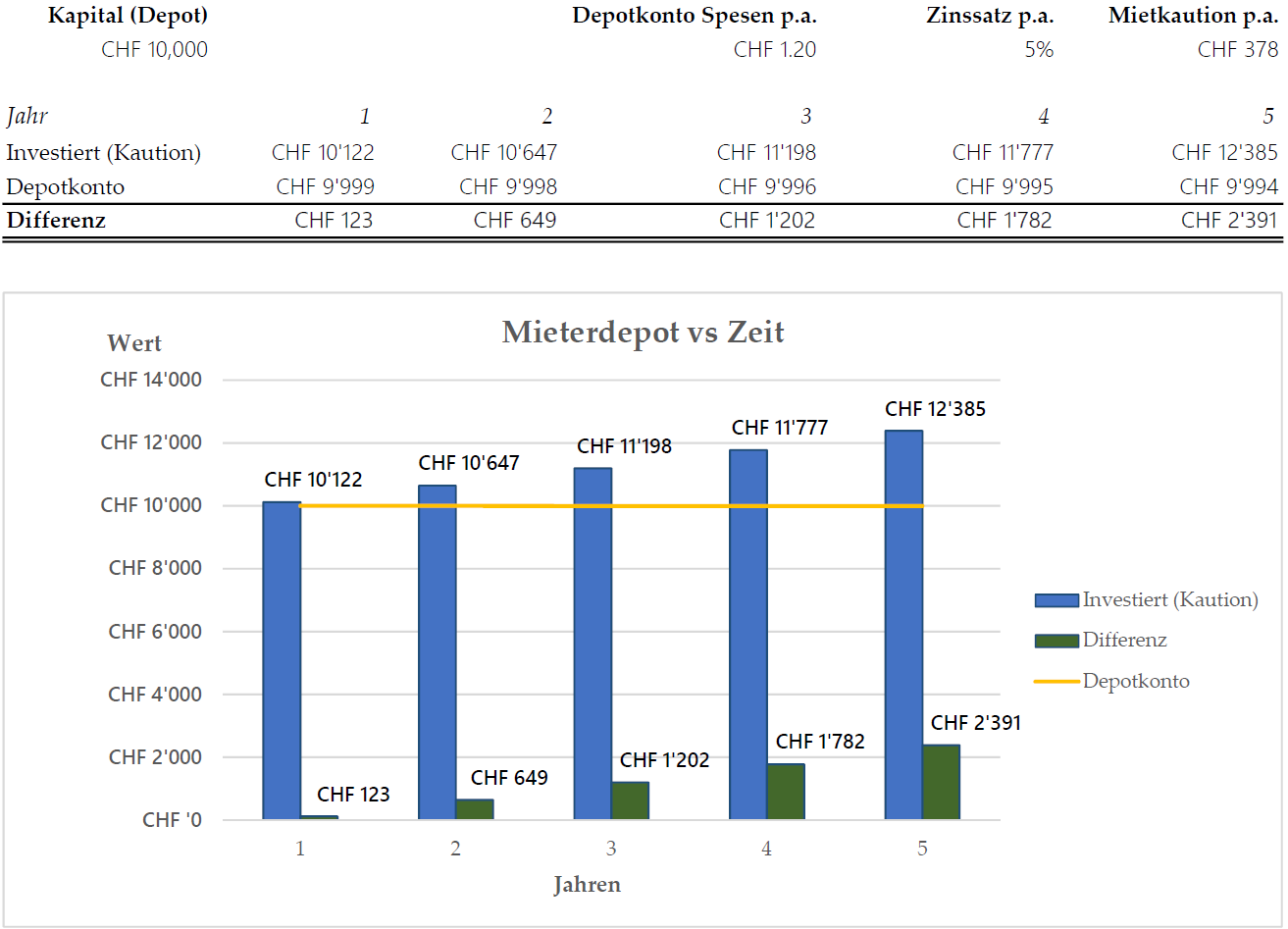

In the chart below you can see the options of

yellow line: money rotting on the account (the annual porto fees are more than the interest)

blue bars: estimated returns at 5% level ( = compound interest minus annual insurance premium)

green bars: the annual difference between the two approaches

The annual premium for the Mietkaution has been calculated with Axa. It includes a 10% discount because we already have insurances there. Axa was the cheapest option I could find.

Yes - we have high rent! We are keeping over 10k in the depot account (it’s already there) .We live in Zug in a family apartment and it is what it is. For various reasons, we are absolutely unable to move elsewhere in the upcoming years.

Regardless, up until now I’ve thought the deposit insurance is expensive but considering the opportunity cost, it doesn’t look so bad anymore. In fact this seems like a no brainer because the break even would be already after 1 year. I did an alternative calculation at 4% annual return and it’s still breaking even after year 1.

I am in good terms with our landlord so this motivates me to re-negotiate the deposit. Comments would be extremely welcome. Am I missing something?

What you’re missing is that 4-5% (savings on not having to pay insurance) guaranteed interest is crazy good return on CHF today, you won’t find anything even close to it today.

)Sure stocks can return even more, but they have a very different risk profile. A fair comparison is with interests on savings accounts and loans)

If you must, it’s cheaper to borrow the cash from IBKR at 1.5% and put it into your Mietkautionskonto, than pay 4-5% to such a so called “insurance” (Note they don’t actually insure anything besides the fact they will pay whatever the landlord wants and then hassle you around to get the money back from you with interest and fees.)

Thanks for the insight. I’m not sure I understood it completely. By my calculation the cost for insurance is 3.78%. That’s the percentage I would be saving by not switching to insurance.

I’m not expecting a guaranteed return of 4-5% annually - that would really be crazy good. I would put the money into ETFs or stocks. That includes a risk component of course. With 0% returns or worse I still have to pay for the insurance. That is a fixed cost and I can budget the insurance in my annual costs.

Another thing I didn’t account for is inflation in addition to the already negative return on the account.

Ok. Well IBKR margin loan is still cheaper at 1.5%. You should consider that option first before venturing into borrowing money from an “insurance” at 3.78%. It’s really a no brainer.

I believe I wasn’t clear enough with my post: That 10k+ is already on the account. It’s my money but it’s locked and doing nothing. I don’t need to borrow it. I agree completely that if it was a case of borrowing vs. insurance then the Mietkaution is really expensive.

I edited the original post to clarify that the money is already there - in prison.

Well, it’s working for you by saving you those 3.78+% insurance premiums. Can’t rent a flat without Mietkautionskonto here, with rare exceptions. Consider it a necessary cost of doing business in swiss

If you “release” the money by going with an “insurance”, it’s just like borrowing it at 3.78+% interest. IBKR will loan it to you for cheaper (with stocks as collateral) and with less hassle (no surprise extra fees if landlord decides to claim)

In fact you can even deduct IBKR’s interest from your taxes, it’s just plain ordinary debt. But insurance premium is technically not debt interest and not deductible

This together with @kilyn 's explanation made it click! Exactly the input I was looking for. I’ve never used leverage for investing (ok, I did have a mortgage once).

Right now I’m with Degiro instead of IB because I don’t have 100k in this category. I did a comparison of the costs between the two and chose Degiro for now. I will do another calculation including the margin loan.

You used to own an appartment/house and are now in an appartment that costs between 3333 and 5000 CHF per month? May I ask for the reasons why you gave up owning a appartment/house?

Sure. That was outside of Switzerland in an EU country. We sold it when we moved. Renting it out in that area was not really attractive and there was some other risk involved too. We have around 50k€ remaining from that which I’m investing in monthly chunks. Right now we don’t have enough liquid funds for a deposit to get a mortgage and buying in this area (ZG) may not make sense anyway.

I’m not at all happy with the current rent but in our family situation options to lower it are far and few in between.

1 Like

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.

.We live in Zug in a family apartment and it is what it is. For various reasons, we are absolutely unable to move elsewhere in the upcoming years.

.We live in Zug in a family apartment and it is what it is. For various reasons, we are absolutely unable to move elsewhere in the upcoming years.