There are still some ways like @xerox5003 mentioned, but you are right. Once you are below 66.6% LTV, there is less room left for tweaking an application. Example with a 2 million CHF house:

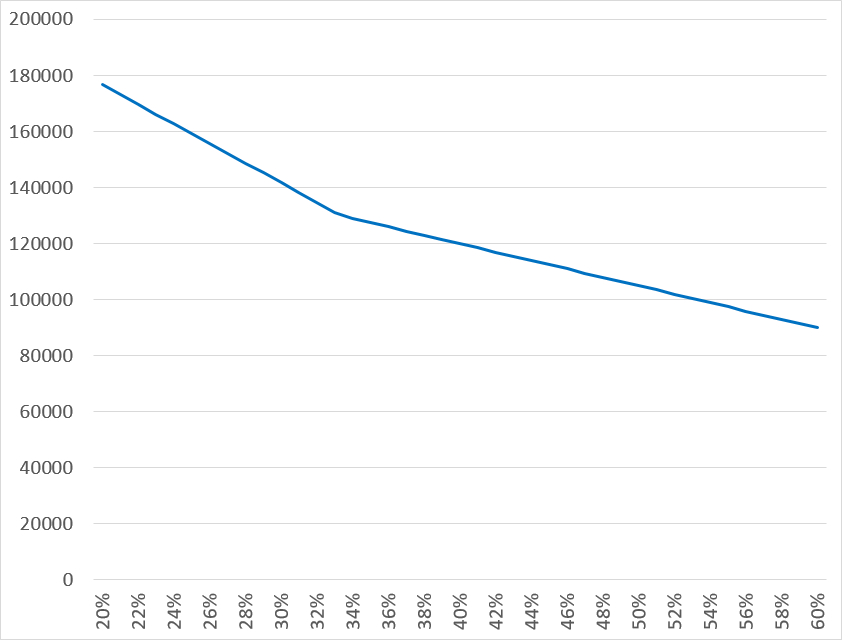

400k own funds, 1600k mortgage (80%): 353k salary needed

600k own funds, 1400k mortgage (70%): 283k salary

667k own funds, 1333k mortgage (66.6%): 260k salary

800k own funds, 1200k mortgage (60%): 240k salary

1000k own funds, 1000k mortgage (50%): 210k salary

You see getting down from 80% to 66.6% reduces the required salary by -26%. Further increase of own funds has less impact from here on.

I don’t know, I must be really crappy at communicating my thoughts. I do not think that you can’t amortize below 65%. But you don’t have to. Not sure which part of my post you’re correcting.

Yeah, 66.6% is the sweet spot (the devil’s number lol), because below it the mandatory amortisation disappears from the affordability calculation. I’ve been always calculating with this LTV, because I always sooner hit the 33% affordability ceiling than the 80% LTV ceiling.

I am not Cortana, but maybe I can share some input:

Of course, this is always possible and has the highest impact.

Yes, if the property can cover the imputed costs (some banks say, 80% are sufficient) this is also a good possibility.

Yes, maybe you can ask your parents for a donation or early inheritance?

Starting an own company is not a good idea, since you do not have a track record and all the boni you generated with your old employer are normally not taken into account anymore. The banks normally want to see the statements of the last three years of your own company.

There is indeed one bank, but this only applies for holiday properties in region of Basel (if this makes sense, this is another story). Your affodability ratio max not exceed 20%.

I thought you wanted to know how to improve your affordability once you are over the regulatory amortization threshold, in that case if you are not able to increase your salary you have to reduce the mortgage either by bringing more cash at the outset or by committing to further amortize the debt so you reach the affordability criteria along the way. From a wealth management point of view I think that does not make much sense but the bank will not prevent you from paying back if that’s what you want to do anyway.

Same for me. As our combined salary is 170k, we can afford something for up to 950k with 20% equties but up to 1300k with 33.3% equties and up to 1360k if it‘s new (0.7% instead of 1.0% maintenance costs if not older than 10 years).

So you see a normal family with an above average salary can only afford something decent when bringing in 1/3 upfront.

Example with 1 million buying price and required salary depending on own funds in %.

P.s. One could argue that if affordability is still above the limits with 66.6% LTV, then maybe the house is just to expensive. Imagine if interest rates went up to 4% on a 1.33 million mortgage on a 2 million house. We are talking about 4.5k/month just for interest.

Does donation or early inheritance solves the affordability problem?

If I start the company now and generate some revenue, then 3 years later can the track record be considered as part of the family gross income? I am anyway not buying house in today’s interest rate.

I am interested how to meet the affordability criterium, yes. But the second part is not correct. I just said that going under the 66.6% amortisation threshold improves affordability. I can much easier improve my savings than my income, just takes time. My income is not growing with time (any more).

In Poland the mortgage interest rate is already at 10% I’m not sure if there is any affordability requirement there. But I think paying CHF 4’500 monthly on CHF 1’333’000 is fair. Arguably, this is still competitive to renting. Not sure how many 2m houses there are that you can rent.

@Cortana by the way, that 1% maintenance used for calculation, for a new flat that seems crazy high. Is it legally possible to reduce it in the calculation? If I buy a freshly built flat for CHF 1’000’000, I do not think I will need to put CHF 100’000 over 10 years into it, to keep it fresh. Or do you think once the big renovation comes (after 20 years), it will get so expensive, that it will make up for the initial years?

Some banks use 0.7% instead of 1% for the maintenance costs on brand new properties. For apartments where you usually have a common renovation fund you do have not to pay anything for the first two years because of the builder warranty thus they reduce the cost in the calculation.

Some banks use 0.7% instead of 1.0% for the first 10 years after construction. For 2 million that‘s 6k less or 18k less income needed. Keep in mind that this includes Nebenkosten (heating, water, insurance etc) which typically amounts to 0.3-0.4%.

So when you buy a house from 2000 for 1 million, the bank will assume 10k/year for maintenance AND Nebenkosten (~3-4k/year).

I think this number is actually on the lower side and maybe even too low. With my example we are looking at 60-70k after 10 years. I don‘t think this will be enough to replace a 30 year old kitchen and 2 bath rooms. And we aren‘t even talking about other big renovations like the roof or replacing a heating pump. Gerd Kommer thinks that 1.5% is a more realistic number longterm (looking at a 30 year horizon).

You can use the assets to reduce the mortgage and therefore the affordability.

Alright make sense. Yet my goal is LTV not lower than 66% for the second house so reducing mortgage beyond that is not aligned with my goal. I am focusing on how to afford the mortgage, without reducing the mortgage. In this context, can asset help?

Yes. There is e.g. one bank, where you put a collataral of three years imputed interest times the mortgage volume. So the money is blocked, but then they do not care about the affordability anymore.

You have to decide for yourself, if it makes sense to keep a high mortgage but have blocked assets or have initially a lower mortgage but paying lesser interest on this amount. There are moreover opportunity costs if you block liquidity in the mentioned example.

This option is indeed very interesting to me. Can you please elaborate a bit more with an example? I am not sure how to understand three years imputed interest times the mortgage volume. For example, 2 million house paid by 700k down payment and 1300k mortgage. How much collataral is needed and for how long, so that the bank does not care about the affordability anymore.

And you are talking about just one particular bank, or this is the case in general for all banks in Switzerland?

One data point, a friend paid 700 fr/m co-ownership charges for a 1.2m CHF, 100 sqm flat with a parking space and a concierge in the building. This included heating but not any costs related to the interior of the flat (paining, kitchen etc)

Purchase price: 2m

Own equity: 700k

Mortgage: 1.3m

Imputed interest rate: 5%

Imputed interes per year: 65k

Collateral of 3x 65k needed (195k), so the affordability rule can be bypassed

This is one particular bank in Switzerland. Unfortunately, I can/may not share too much information, since I am working in this area.

You have to ask yourself, if it does make sense to block cash instead of using it as a downpayment and lower the mortgage. It’s a nice USP they have, but honestly I can imagine better solutions instead of blocking cash.

Ok, now I got it, with the example. Thank you. And I assume the collateral needs to be there for as long as the affordability is not met?

I wouldn’t like to put 195k cash as collateral. But 195k cash equivalent, for example stocks, as collateral to go over the affordability limit would be very attractive to me.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.