Hello Mustachians,

I signed for a Pillar 3A insurance two years ago (01 Dec 2016) from axa winterthur

Recently, after having thought a great deal about it, I have come to realise that I totally misunderstood what it was. I now regret the fact that I signed up for the insurance and would like, if possible, to either cancel it altogether or change it to another company.

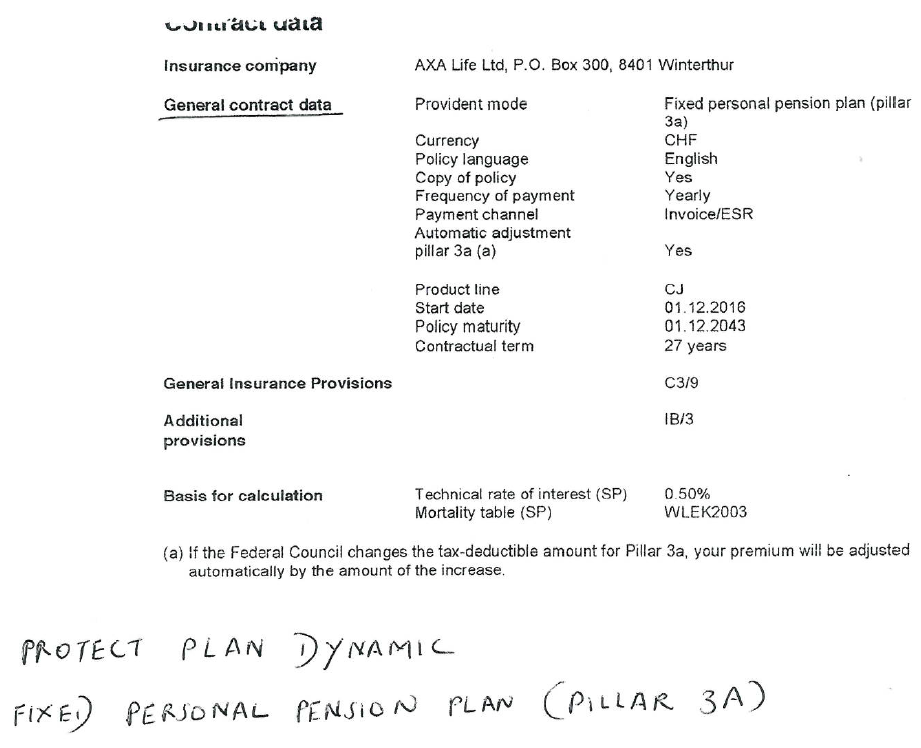

It is a pure endowment insurance (dynamic) plan. The plan is called “protect plan dynamic”.

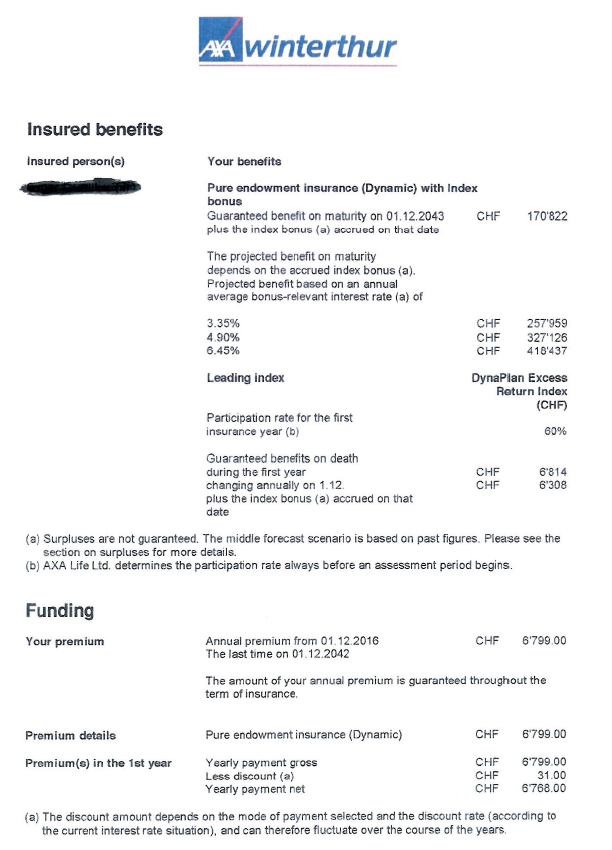

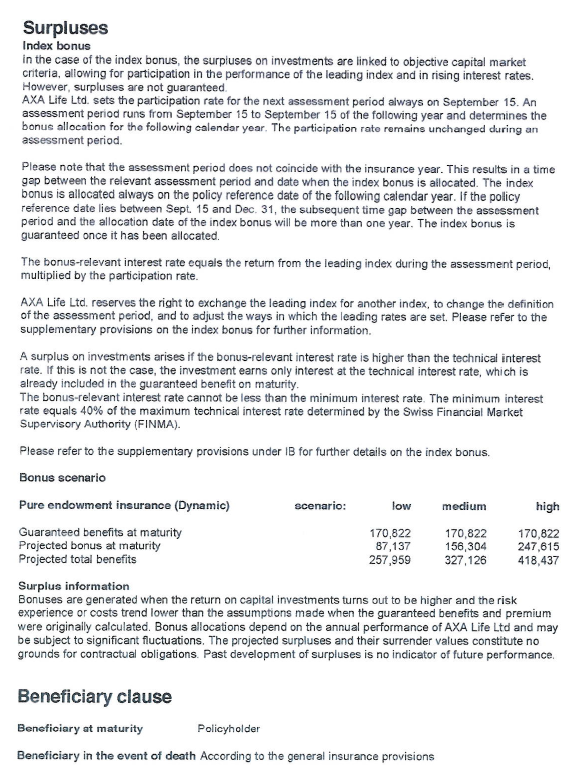

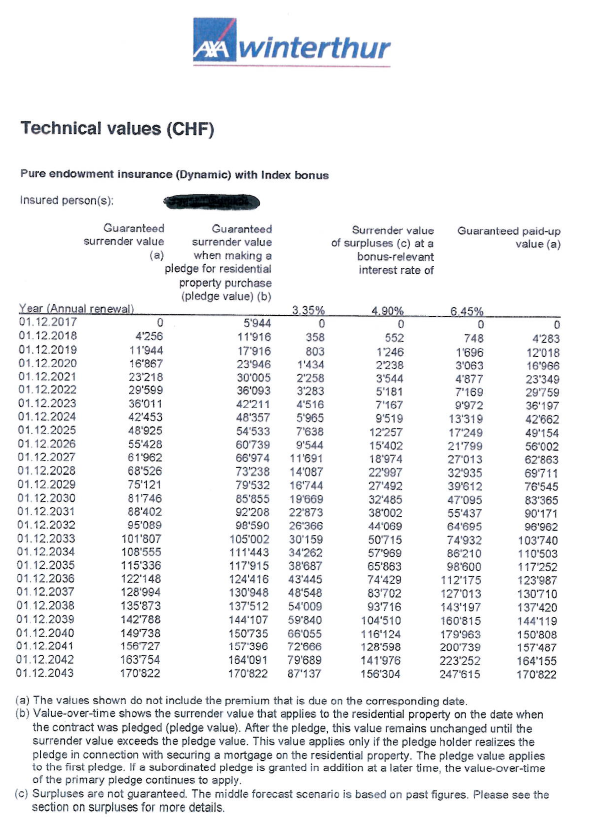

There is a guaranteed benefit on maturity on 01 Dec 2043 (plus bonus depending on market, which I am not considering).

The guaranteed benefit on maturity is lower than the sum of all premiums.

I have claimed the entire premium amount of 6,768 CHF against taxes in 2016 and 2017.

•The premium paying contract runs for 27 years.

•First premium paid on 01 Dec 2016.

•Last premium payment on 01 Dec 2042

•Annual premium amount: 6,768 CHF

•Total premium amount paid so far: 13,536 CHF

I have attached the relevant pages of the insurance policy.

I did not understand that I would get so little money if I ever want to move abroad or decide to purchase a house here.

I am looking for a way to get rid of it without losing everything. Transferring it, buying it for a lesser price, terminating outright or anything else.

If anybody has any expertise or previous experience on this matter, I humbly request you to share your knowledge. Thanks very much.

I know that I have made a mistake and any reprimand or harsh words are justified.

If it helps in any way, my personal situation is as follows:

40, Indian national, C permit, Basel Stadt.

Plan to get married in 2019, start a family in 2020 and buy a house in Basel Land (reasonably close to Basel Stadt) in 2022.

Thanks for reading,

Sirob