Yea. My grandfather got 1. pillar without ever paying in a Rappen. But that is OK, it is the purpose of the 1. pillar.

But the 2nd pillar? The purpose was that everybody saves for himself. But now working people have to support the higher payments for older people and will never get them for them self, that is just not fair.

There are two ways: get rid of it altogether (or integrate it into 1. pillar) or start individual accounts where the choice stays with the insured person.

I agree, it’s where the system in CH appears to be starting to break despite being in theory part redistributive (1st Pillar), part capitalized (2nd & 3rd pillars).

It’s already well and truly broken in many other countries, though, so a personal solution would be to geo-arbitrage (as you already do, right?).

I understand the message but I think there is more to it. Something is different for sure and I don’t know if it’s entirely upto unsustainable conversion rates

It’s not that suddenly fund managers became stupid or market became less rewarding. In fact we are living in times of asset bubbles everywhere.

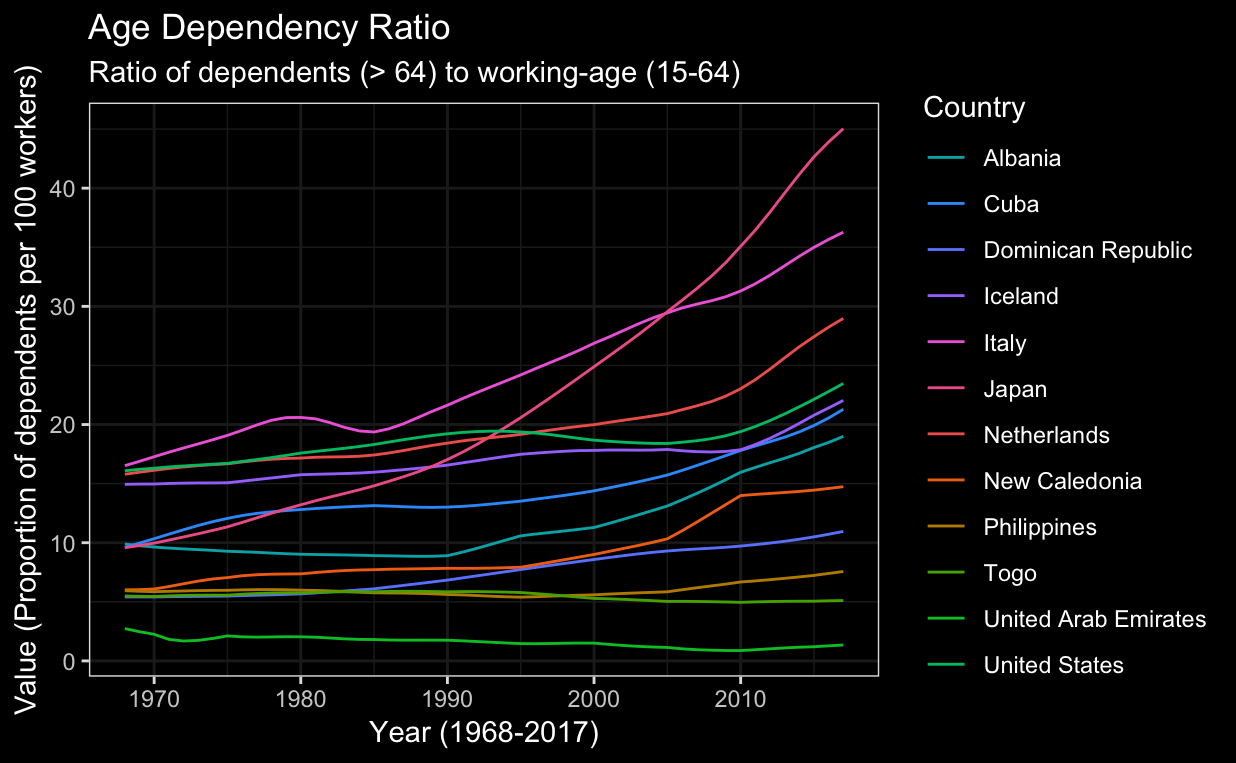

It’s just pure maths: if you predicate a system on say, 20 people paying into a pot and 1 withdrawing for a few years before dying.

Then you realise hey, people are living much longer e.g. going from 5 to 10 would be doubling the amount withdrawn. On top of that population is growing slower, so you may have only 3 people paying into the pot for every person withdrawing. If you don’t adjust the payouts, then soon the pot will be empty and all but the early few will have nothing let in the pot to take from when it is their turn.

Yes. These factors apply also to 2nd pillar and also to Switzerland.

As @cubanpete_the_swiss did, you can withdraw your Pillar 2. It would not surprise me if this escape hatch is closed and/or raided at some point.

There’s already talk of increasing taxes on Pillar 2 and 3a withdrawals (RAID).

In the end, how this problem is tackled with have a large bearing on FIRE planning. I have my ideas and solutions, but yes, Dr PI can close the thread now *

Well, it’s not so simple. It’s pure math for the 1st pillar, I agree.

But for the 2nd pillar, everyone draws a pension (or a lump sum) from its own contributed amount.

We can debate if the current conversion factor is too high, right or too low, but if the pension funds have the necessary capital coverage, then there is no transfer.

If many/most of the pension funds do not have the capital coverage, there could be transfer if no corrective measures are taken: retirement age or conversion factor or a mix of the two.

That’s why I asked for a factual/mathematical explanation of the hypothetical (until proven) inter-generational transfer for the 2nd pillar

60 years…there will be 5-10 bubbles and probably the same number of crashes.

The reason is simple: the performance of the investments is lousy. Very lousy indeed. That is only partially the fault of the money managers, the other part are the laws. They need to change, now! Not my problem any longer, took out everything in 2014, but the poor working people who still payed in since then are fucked.

2014 - 2020 45 Billion CHF were stolen from the young and given to the old:

I see that the common view seems to be to take the under performance of 2nd pillar pension funds on face value or attribute it to demographics or poor fund management or simple life.

This means there is nothing to resolve. I don’t necessarily agree but also cannot add more value to the discussion.

The interest paid on the contributions (“Verzinsung”) and the conversion rate (“Umwandlungssatz”) are not based on math or economy, but politics. If current pensioners got a high conversion rate (can’t be cut), that is compensated by lowering the interest paid on current workers’ contributions.

The conversion rates are still too high. This is not based on market results in the past or future, but what the voting population will accept.

Don‘t worry too much about that paper. Its a marketing paper that was intended to make pensioneers go to VZ for help. There are clear gaps thatvwere consciously not addressed in the paper and the results are not quite right. Please read the press coverage on the paper from VZ.

Fwiw it depends a lot on the fund, the axa fund I used to be in after the last fixes to conversion rate had minimal redistribution (was actually going both directions).

Exactly. This problem is theoretically solvable, but in practice cannot be solved due to politics. It would be political suicide to cut pension benefits. You see similar dynamics in other countries (e.g. UK triple lock protection) and also other issues (government budget deficits and growing national debt).

The pain of fixing these issues are too difficult to take politically and so the best politicians can do is mumble a few soothing words and try to kick the can down the road.

Unfortunately, at some point you run out of road. IMO, inflation will be the only way to ‘solve’ these issues. Instead of finding a way to settle the obligations, the easy path out of inflating them away will be taken, if not purposefully, then by default and inaction.

To me the most important part of the article is this:

”In theory, pensions should pay out 60% of the final salary but this is no longer the case. Concretely, a person currently earning CHF100,000 per year will receive about 51% of his or her final salary in the form of a pension at retirement. With an income of CHF150,000 the share drops to as low as 42%.”

Those 60% of the last salary are important to sustain people above 65. That was kind of a promise by the legislators who put together the BVG framework. It no longer holds true and needs to be addressed.

Not thinking as a mustachian, I feel that the system to provide retirement income needs to be based on a sound foundation. No need to throw away everything, but cross-financing retirement across generations is not a good idea. All I want is a tax-sheltered way to save 30-40% of my salary, so 44 years of my work are able to pay for the 22 years of my retirement.

Well, I mean, the mandatory insured salary is capped at 90’720.- so of course 60% of more than 90’720.- is not insured by default (though many plans uncap it, indeed].

Not saying that the base reasoning doesn’t hold, just that the article seems to cherry pick its numbers without presenting the whole picture (disclaimer: I haven’t read it).

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.