I am too liquid at the moment. I should have invested more but I’m not really keen investing at current valuations, especially with Mrs. pressing harder and harder for buying a home.

I opened a neon account to park money because the threshold for negative rates was 500k but they recently cut it to 100k.

I am looking for an alternative solution, in eur or chf.

My alternatives so far are:

Invest, take the risk (not really acceptable but I could mitigate this risk by buying real estate funds for example)

Open another account: Where ? I thought of Zak. I don’t need any services, card… Ideally when I have use for the money I want to transfer it without headaches or fees.

Buybacks in my french life insurances (I kind of ignored this option as I forgot about the rules and taxation of those accounts…)

What would you recommend, especially for the 2nd point (and the 3rd point if you know this segment) ?

Sorry but you may end up in a situation where you don’t have enough money to buy a house because you didn’t invest and you don’t invest because you want to buy a house.

You can start by filling 3rd pillars and invest these money, for example.

Moneyland.ch shows 150+ saving accounts, I am sure you will find something suitable for you.

WIR still offers 0.05% interests for money up to 500K on their savings accounts, though you have to announce 3 months ahead for withdrawals of more than 30K and they’re likely, like most bank, to take that limit down in the future (they also may have other fees that I haven’t researched).

If the house buying project is short term, I’d park it in lots of 100K for insurance purposes, and pay some fees in the process that I’d try to make up for with my other investments.

For durations of more than 2 years, term deposits still warrant some low interest in many banks (WIR and my Raiffeisen branch being among them).

What a nice problem to have I agree with Dr.PI and I suspect a lot of people in Switzerland find themselves in this situation

What about 1) but via dollar cost averaging (DCA)? You could resolve to set up a monthly investment for a fixed amount as big as your monthly savings so your “problem” doesn’t get any bigger. At the same time you don’t risk the psychologial impact of losing your current deposit, at least until you feel confident to invest it.

If you need to hold cash, you can open a CSX account with CS for free. Private account is free up to CHF 100k (no withdrawal restrictions). From within the CSX account/app you can add a savings account and store up to CHF 2M without negative interest (free, withdrawal conditions apply). They will likely ask questions and try to sell you their products, but you can say no. IMO, there is no hassle-free way to park larger amounts of cash, unless you have an existing relationship with a bank (substantial equity portfolio or mortgage).

Depends on what your time horizon looks like to buy a house.

If it is within 5 years, I would not play with the equity markets.

IMHO, the best option would be to stick it in various kantonal banks with not more than 100 K in each bank in a single account (as @Cortana said), taking into account the withdrawal ease.

All other options are sub-optimal (including buyback of 2nd pillar).

I am there trying to get out but I have already a property which is rented in CH and only think in a long term investment. Just putting money in VT and IB.

That sounds as good advice, but a friend of mine did the downpayment just taking out the profit from the stocks invested in the 2020 march crash.

Of course it was 0 in VT

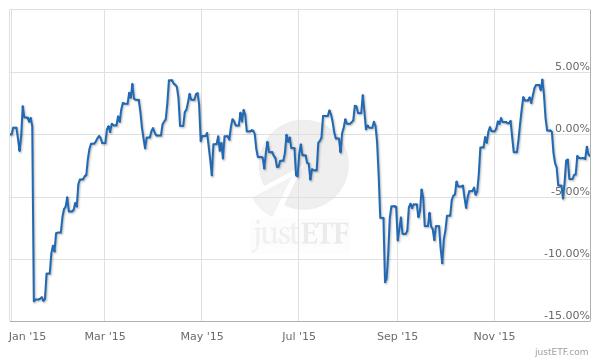

The odds favour gains in the stock market yet, down years happen regularly enough. Who remembers 2015? I don’t, it was a pretty unremarkable year if you ask me, yet your friend would have spent the year looking his downpayment go slightly up and greatly down then end the year on a tame -2% (That’s with VWRL, converted in CHF, dividends accounted for. It would probably be a rougher ride with less diversified stocks):

It’s not far away, it can happen any year. No need for a big crash for short term money to be eaten by a small drawdown plus some fees (sprinkle some panic selling on it at discretion). Long term investing is still where the money is, though.

Edit: the first drop is due to the SNB unpegging the Frank from the Euro but the picture in USD is similar enough:

He was pretty brave (or reckless)…doubling the money just 6 months before the mortgage.

1 Like

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.