Nope, no idealized scenario here. None of us here are able to predict whether things will go up or down nor whether we’ll act like we say/think we’ll act (often people will say “yes, but if stock goes up…” - sure, and it can also come crashing down before you sell it…)… because if we would be able to accurately predict that, I sure as hell wouldn’t be spending my time on a FIRE message board. Holding cash = also taking risk. DCA = also taking risk (never mind the fees). Eating that additional M&M = also taking risk.

So, all you’re left with is “don’t know” and how do you act based on that. I’ll take the premium (tax free!) plus the potentially reduced purchase price across a portfolio of positions for stocks I’d like to have anyway - it works just fine for me.

I provided a path. Never claimed it was the only one.

Some here seem to jump on a thread to snipe rather than providing alternatives.

That wasn’t my preferred answer, but ok. As suggested, I asked Gemeni and was able to answer my own question. Yes, this is done by selling (writing) puts.

Since this topics seems to be a recurring theme where most arguments have been written in this forum, I don’t want to extend the discussion any longer than necessary, but simply summarize my understanding. It’s a strategy for DCA investors to make their uninvested cash work (i.e. generate more income than the non-existing savings interest) until it is invested. It is not risk free but if you know what you are doing, the risks are managable.

From my limited understanding, the thing with writing puts is that your upside is limited, if the underlying rallies, you will not get assigned and will lose on that upside. Of course, you keep your small premium.

So, it would seem that it’s most advantageous when the market is flat. But then comes the question of trading volume. If you want to generate significant income and not get fucked by the MM. You need to have a portfolio of at least 150K+.

The focus of the anti-options point is the tail risk (as somebody else put it: what if it completely collapses in price). Guess what, if you buy the stock/ETF/etc. outright (or via DCA) you have the exact same tail risk. If you are concerned about a specific investment completely collapsing then you’re probably looking at the wrong opportunity regardless of which instrument you use.

Fundamentally, when for instance writing an out of the money put, you articulate it as being paid to insure somebody elses risk. While I see some merits to that, my perspective is rather different:

I want XYZ (let’s say current price: 10)

By writing an out of the money put (e.g. strike price 8) I reduce the uncertainty about what I’m going to pay for it (regardless of whether DCA or buying it in one go)

80% of options wind up expiring with zero value and my experience is that the 20% (perhaps a bit less, in my case) where I do take delivery, the price is not that far below the strike price and I’ve almost always been able to quickly convert it back into cash (+ a premium) using a covered call option.

“we have some history and some logic” - yes, and you purposefully apply it to a case which doesn’t suit your philosophy, narrative, etc. but conveniently ignore the fact that fundamentally this point could be made in almost any situation… e.g. you could argue Warren Buffet’s returns are just luck, a coincidence, a random event (one in a billion investors) while he’d argue it’s not.

That’s fine, everybody finds their own path… incl. some apparently sitting on a high horse without being aware of it.

You would agree though that there are several steps someone not gambling must take, and document and understand beforehand, before this makes sense? Eg

what’s my goal for doing this?

what’s my risk-free rate, and how much above can I get it using CSPs or CCs?

what’s the impact of the volatility

what am I willing and able to commit?

what amount or above do I need for this to make any sense, ie does it make sense to take the trouble for $100? No, in my opinion. $1000? Borderline. $5,000? It’s now interesting, but then you need to put up 50,000+++ to get there, isn’t it, but then it goes to no 4 above etc.

I understand the theoretical part members here are pointing out, framed by total return. I also understand the point about a price crashing through your CSP and you ending up paying 8 for something worth 1: you’ve theoretically lost money, but in practice it may be that you didn’t if you were fine to own the stock for 8? Of course some of our colleagues will be incensed reading this!

Again I think the point is that these are essential and pretty complicated questions and unsuitable for someone unsure if to DCA in broad index funds in any way other than food for thought.

Edit: caveat: I find options incredibly interesting but haven’t had the guts to dip in.

disclaimer: I’m also trading options (more actively in the past, and resuming after a short break)

While I have no particular objections to your points above, it may be worth highlighting — especially for our less experienced colleague(s) — that the longer the option’s DTE, the longer you remain “locked with” XYZ.

I mean, if you place a limit order on XYZ and the stock subsequently takes a direction you no longer like, you can simply cancel the order at no cost. By contrast, if you have sold a put, you are exposed until expiry (unless you close the position). You either accept the possibility of being assigned shares you may no longer want — and then potentially try to get rid of them by selling a call — or you buy back the put, possibly at a higher premium, which could result in a loss.

Yes, absolutely correct. Hence I don’t (OK, i have been ‘guilty’ of it a few times in the past) due purely speculative options trading for premium harvesting on stocks I’m fundamentally not interested in owning. Eg. made a lucky / lucrative options trade on Microstrategy but that was stressful. 99% of these written puts are on stocks I’d want to have anyway. Note, not that I am narrowly focused on that one stock, I’ll have a portfolio of stocks that I like and write OTM options on and most don’t then come my way. It actually helps me to not fall in love too much with a single stock.

Now, if you buy the stock outright (or through DCA) you fundamentally have the same issue as you describe… you accept the possibility of being underwater. Unless of course you delay purchasing entirely because you expect it to drop but that becomes different discussion (time in the market vs. timing the market).

I see it very similar, I get greedy in the sense that I do not want to pay fees to buy a stock but actually get paid to buy a stock. At least for me I do not really make a lot of profit from the option selling, it’s more a limited buy order that I play as long as needed if I want the stock. However, there where from time to time some bets that I did for stocks that just had a massive drop and I did not really wanted in my portfolio. I do almost never do call options as I see there the problem with the limited upside. Only if I get assigned a stock that I do not longer want I work with call options but this strategy is not really well defined yet.

No need to get pissed. There are applications of covered calls and cash secured puts, but “uninvested savings” probably ain’t it. Those strategies tend to have stock like losses, but only cash like return.

Regarding Buffett’s Alpha: Buffett’s Alpha by Frazzini, Kabiller, and Pedersen (2018). Whether or not the explanation through factors and extremly cheap leverage is datamining, it is rather unlikely that the next Warren Buffett is on this forum.

Cash secured puts and covered calls beat the raw underlying on a crash, because you will have the premium in addition on top of what happens.

Of course, only if you don’t get liquidated in freak markets. Selling options means owing something. Prices can decouple, and brokers can panic.

The bigger problem, though, is more the other side: The market explodes and you are effectively in cash.

@Butch , reading the initial post again, it seems they actually do want to invest it all, just not lump sum. I revise my stance and I think your suggestion could be useful here to get some returns while waiting.

It goes down → You get it cheap.

It doesn’t or goes up → You would have waited anyways.

I’m not sure a novice can execute this correctly though. Also they probably shouldn’t space this out for multiple years. So DOTM puts won’t have much optionality premium.

“The bigger problem, though, is more the other side: The market explodes and you are effectively in cash.”

That point connected with the original posters position is kind of like being half pregnant.

Some generally accepted facts:

80% of options expire out of the money

Equity markets in general grow 5-6-7% CAGR in the long run - i.e. time in the market is more important than timing the market

If you get a premium of 1 for a written put option (strike price 8) on a stock with current price 10, then your max downside from a catastrophic crash is 7. A middle of the road scenario would be that you get the stock at 8 + 1 in cash. As per your own admission, the max downside from a surge is infinite.

Given the premise of this entire discussion is that somebody fundamentally believes an investment is a good investment and will increase in value over time, delaying market entry or DCA-ing would surely according to your logic destroy value. If you apply probabilities to the 3 scenarios in the last bullet, my hypothesis is clearly that written put options create value.

My entire point though is not to aim for ownership at a lower price with options, but to generate income with potentially a lower priced entry point (but just as happy with no entry point).

Bottom line, you conveniently use the “the stock could surge” argument but are not willing to back those words up with a strategy thusfar.

This compares the 3 strategies (staying in cash, buying stocks, cash secured puts). The underlying stocks are worth 100. Volatility was assumed at 15%, maturity for options is 365 days out. To focus on the relevant part, dividends and interest where set to 0. This gives around 6 premium for a strike at 100, 2 for a strike at 90, and 0.4 for a strike at 80 (option-price.com).

Cash is better on a drop lower than the options strike (minus premium), then options are better until stocks rise more than the premium.

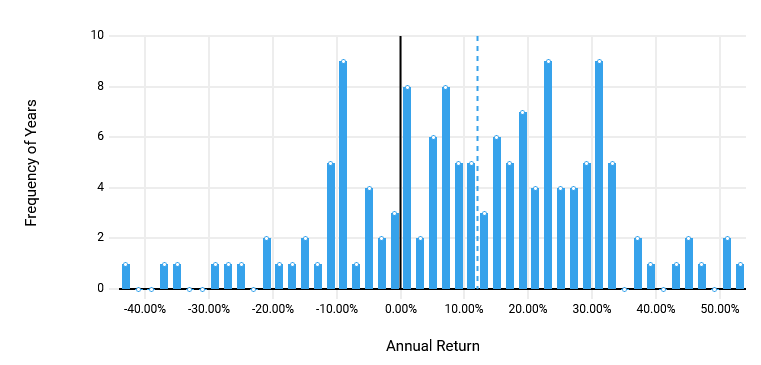

This is a histogram of annual returns for tesfolio’s SPYSIM (large cap US stocks, back to 1885).

I’d say most lies outside the range where cash secured puts win.

But this is of course no apples to apples comparison. We would need actual data and compare the strategies over the whole year (because American style options). Could be done. If you want to prove your point, please do.

If not lump sum, probably buying DOTM calls. Or DITM calls.

It lowers the expected return vs. lump sum on a random entry. But it also lowers volatility of outcomes. I think that often the entry is not random. I think novices, especially, tend to be motivated to enter the market during euphoric social sentiment towards the market.

I write options mostly just like @Butch. Plenty of option income taken in so far (high 5 figures over the last couple of years).

Last option sold on Feb 20: AGM Nov26 125P. Sold for $5.529, currently trading for $4.65. I expect the option to expire worthless, but I’ll take delivery for $125 if needed as this is and would continue to be a long term holding. AGM is currently trading at $166, so the time decay is probably most of my profit over the next couple of months/quarters. Certainly exceeds the dividend I would get if I held the underlying outright. Already exceeds the dividend in the timeframe since I sold the option, actually, if I bought the option back today.

First it would be nice if you had some non-anectotal data to back up your argument. What is the expected outcome of such a strategy? How does it compare to alternative strategies (e.g. plain buy and hold)?

Also something else that would be of interest to me, although it does not necessarlily seem to be your field: DITM options that are months to years out can have quite some spread. Can one get fills mid market or near your side of the bid-ask?

This thread was already killed by Mr. Pi, and as I was called out by them as well, multiple times. I’m a little hesitant adding to this thread, as I have already added to it but it was readily and reliably censored, IMO.

I’ll add my summary update, but I’ll state that I won’t place any bets on it surviving. Any options writing like described above (Options trading, Cash Secured Puts etc - #101 by Beate) seems to continue to work fine, What seems unclear is whether anyone safe from offtopic or bickering is … well, clear of criticism.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.