Still depends on frequency, size of portfolio, etc. They also don’t want people to deduct losses ![]()

1 Like

Forgive me if I’m not following but I don’t understand the talk about hedging for this particular situation. Selling puts, you get a premium. That would be income, not capital gains, and, as such, taxed as income.

Now, buying options (whether calls or puts) would be buying an asset that can appreciate (as well as loose value). That appreciation, if it happened, would be capital gains which may or may not be taxed depending on how the tax office classifies @stra, as a professional investor or not.

Now, in case selling puts makes the tax office classify @stra as a professional trader, which it may (though I’d consider it unlikely if the amount is not really significant vis-à-vis other sources of income), then other capital gains would also be taxed. But the premium coming from selling puts would be taxed anyway, regardless of how the tax office classifies the seller.

Am I understanding it wrong?

1 Like

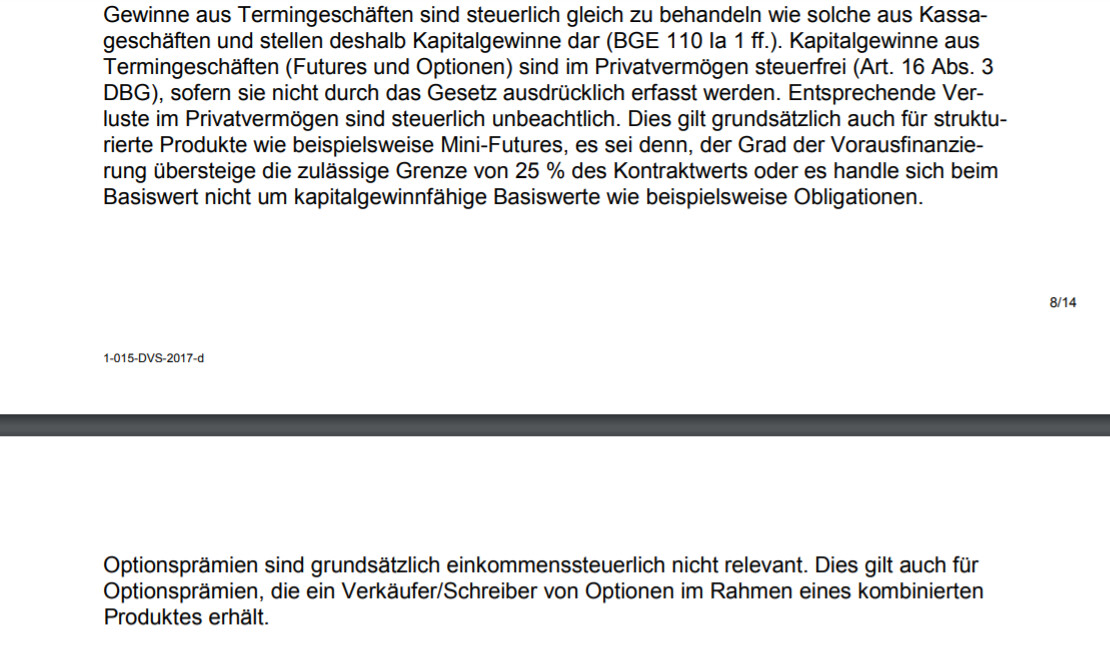

Earnings from selling put options are considered equivalent to capital gains, not (dividend/interest) income, from a tax perspective. The reason is that in both cases (selling securities and selling put options) you’re making money from price differences. See BGE 110 Ia 1 and section 3.4.3 in https://www.estv.admin.ch/dam/estv/de/dokumente/estv/steuersystem/dossier-steuerinformationen/f/f-finanzinstrumente.pdf.download.pdf/f_finanzinstrumente_de_2018.pdf

3 Likes

According to Circular 15 from the Federal Tax Administration:

Les primes d’option n’ont en principe pas d’incidence en matière d’impôt sur le revenu. Ceci est aussi valable pour les primes d’option, qu’un vendeur/souscripteur des options reçoit dans le cadre d’un produit combiné.

So no, unless you are considered professional option premiums are tax free, no income tax is levied.

2 Likes

Anecdotal but in Geneva I have not heard of any of my coworkers being classified as professional traders for tax purposes. And I know they do a lot of personal trades per year (I work for a trading firm).

On the topic of short volatility strategies (in particular cash secured puts and covered calls) I recommend being very wary of your risk exposure. Many of these strategies can be summarised as “picking up pennies in front of the steamroller”, i.e. you make a few % every month and eventually lose everything when a freak event happens.

Not that short volatility is always bad, you just have to understand WHY someone is paying you those few % and what event you are insuring against that WILL happen in the long run.

I would also recommend reading insight from professional volatility traders like the below:

2 Likes

I started doing some small options trades, mainly selling puts monthly to open positions in SPY ETF (S&P 500 index ETF) as a way to get paid for DCA

I’ve stopped and given up on the small extra income because of the uncertainty over being taxed on capital gains on my whole portfolio. Given the relative size of each the risk is too high for me

Good to hear that Geneva does not seem to be too strict [Edit: Geneva resident]

@Ed_Waadt you are right, i found the same document in German file:///C:/Users/efstr/Downloads/1-015-DVS-2007-d%20(1).pdf (it is easier for me than French ![]() )

)

Anyways, I will talk with someone from the cantonal tax-office and let you all know what they officially say.

You’re right, I was too lazy to add the reference to the German text.

But yeah, that’s the rule unless you’re considered a professional trader.

Hi everyone! as promised, I am posting an update after the phone call with an options expert from the cantonal tax office of Zurich. I explained him my intention (to sell options) and he explained me two things:

-

As long as I declare all the transactions of the year thoroughly and they can see from my payslip that I have a normal salary from a 8-5 job, there is no probability that they consider me a professional trader.

-

Even the premium that I may receive from a put sell (or any other option) is not taxed, since it is not considered revenue (Ertrag in German), but it is somehow connected to the capital gains (or losses) of a stock in the future.

So in the end they are pretty relaxed (he even told me not to think too much about it, as long as a have salary job).

4 Likes

So much for “only declare your positions at the end of the year”.

Thanks for the update @stra! Would be curious to know how the cantonal tax office in Schwyz would anser the same questions.

Does anyone know what is actual capital gain tax if you are listed as professional trader? Or gain is simply added to annual income?

1 Like

Added to your revenues, there’s no specific tax % on capital gains like in France for instance. But you also need to pay AHV and so on on top of income tax.

1 Like

Any updates on Mustachian options trading profits vs. a benchmark like VT or VTI (opportunity cost of not being fully invested in an index)? I’ve always wondered if the option trading yields are actually worth the effort.

Science does not seem to back magic profits for covered call strategies:

https://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.1023.1099&rep=rep1&type=pdf

Last year on my portfolio I got

- a little over 4% in dividends

- an additional nearly 7% in options income (writing covered calls as well as cash secured puts)

- above in addition to the increase in value of the portfolio itself

I’m considering reducing the nr of put options trades though (to make it less work) and go more down the path of long term options writing (e.g. cash secured puts with December 2030 as expiration date). I’ll give up some return over time (v.s. e.g. writing 1 year options again and again until 203) but it makes things less work and if you target the right stocks to write these options on the potential is appealing - i.e. very high premiums + potential to get the stock at a major discount.

3 Likes

how will you handle them from a tax declaration POV ?

In a few weeks I’ll download my big UBS tax report and hand that to my tax consultant (along with a boatload of other documents) and he takes care of it.

Practically - assuming my understanding thusfar is correct

- Options premium don’t count as income = tax free (aside from the small wealth tax for part of the premiums not used to pay down the mortgage or other living expenses or to invest in stocks/ETFs)

- The options themselves show up as a negative amount in my portfolio thus reduce my taxeable assets

1 Like

-

Write a cash secured Put on a solid dividend paying stock which you’d like to own at a discount (e.g December 2026 expiration date)

-

Receive the premium and put that in a middle of the road diversified ETF

-

Repeat again after the expiration date passes (assuming you don’t take delivery of the stock)

It’s a good way to keep cash while generating income and putting that to work. If you do wind up having to take delivery of the stock, you’ll get a good stock, which generates dividends, at a discount.

2 Likes

How do define such a discount? Today’s price minus 5% or 10%?

I wish it was that simple.

I use a couple of parameters

- I tend to not do an options trade if premium in absolute terms is not at least 1k CHF

- I have access to a lot of equity research from UBS and tend to select companies which I’d like to have in my portfolio (not too expensive, good dividends, not too much debt, and with upward potential based on the analyst estimate in terms of stock price)… this way, if I do wind up taking ownership I’m just as happy. I keep a range of such stocks on a list so I never fall in love with a single one but can use them as a pool.

- I tend to indeed go 5-10-15% depending on the stock and sometimes 20%+ (if a bit of a longer term option write). E.g. recently wrote a 2030 expiration date put option 30% below current price and got 20% premium paid relative to the price I’d have to take it for. In other words, my exposure was 50k (if i’d have to take delivery) and got a 10k premium today. Counterparty on longer term puts rarely wants to exercise early so i can relatively worry free wait until 2029 and in meantime have the 10k invested.

- If the option rapidly reduces value I sometimes buy it back and write a new one.

In other words, there is no perfect answer. But these are stocks at the end where plenty of people are buying them now and instead I get paid to potentially have to buy them at a lower price later. I’m fine with that.

4 Likes