The more I think about this the more worried I am. If my saving capacity is around 3.5k per month, I am already somehow timing the market by investing 15-20k per month. Of course it’s better than all in one, but still, if we’re in all time highs and a recession comes in a couple of years, it will take me more 6 years to invest the same quantity and probably almost 10 to “average” out (basically until the next recession).

I know I shouldn’t be thinking like this, but I’ve seen some posts in the forum about this issue, and I am a bit concerned, tbh.

Hi Albert, you are really in a privileged situation, having already a bunch of money aside. So currently your natural fear to lose is stronger than the trust to gain long term. You can always pass away the responsibilities to handle your money to a bank. They will mix it up more conservative and you will sleep well. Have a lot of friends, who have a lot of money, but can’t stop thinking every day about “bad news” in the newspaper when they are invested in equities. So they passed it to their bank and they are really happy.

If you want to keep the responsibilities to your own, there is no way around that you have to stick a toe in the water. Just start small with a monthly investment, make yourselves comfortable with the tools and the feeling if a the price dumps 2-3% per day. And when (not if) there is the next recession of crash, than you can buy lower with more confidence.

Remember the next bad news, crash or even recession will come, we just don’t know when and how it will reflect on the market. Good luck to you!

Found this picture - think this is the S&P 500 with some “end of the world events” linked: https://imgur.com/g7WmIXr

True, and as @OogieBoogie wrote, if you are an inexperienced investor, going for a passive approach might be more suitable from a psychological point of view. Just be aware of two points:

(1) Timing the market is generally a very bad idea. And yes, currently there are signs of a recession, but that discussion has been held at least three times since 2009 and everyone who waited for the crash has lost a lot of money (from an opportunity perspective)

(2) Despite what I just said, in your situation you will not be able to avoid timing the market. Either you wait for a crash that might or might not happen, or you invest and might or might not make nice profits. Point is: No one knows what is going to happen, so go with the average, hence dollar cost averaging investing. With 3.5 kCHF savings/month, I’d however lower the figure I first mentioned to 10k/month, which gives you around three years until you are fully invested.

Edit: You could of course also create a more sophisticated strategy. You could for example invest just 7k/month, and time the market with another 3k for every 3% drop from previous high (all figures just examples). This is not necessarly a good idea from a statistical point of view (because missing out just a few very good days on the market is decisive for long-term returns), but it would get you to invest, gather some market exposure experience, and give you the feeling of beeing in control. Because in the end, the most major mistake investors make (at least in my experience), is having a strategy that stresses them, and consequently they mess-up their investments with irrational, fear or over-confidence driven decision from time to time. For the same reason many investors choose a dividend strategy. Statistically that is non-sense, but receiving the dividends even when markets fall feels like a warm blanket. If that is what’s needed to keep you in the market, so be it.

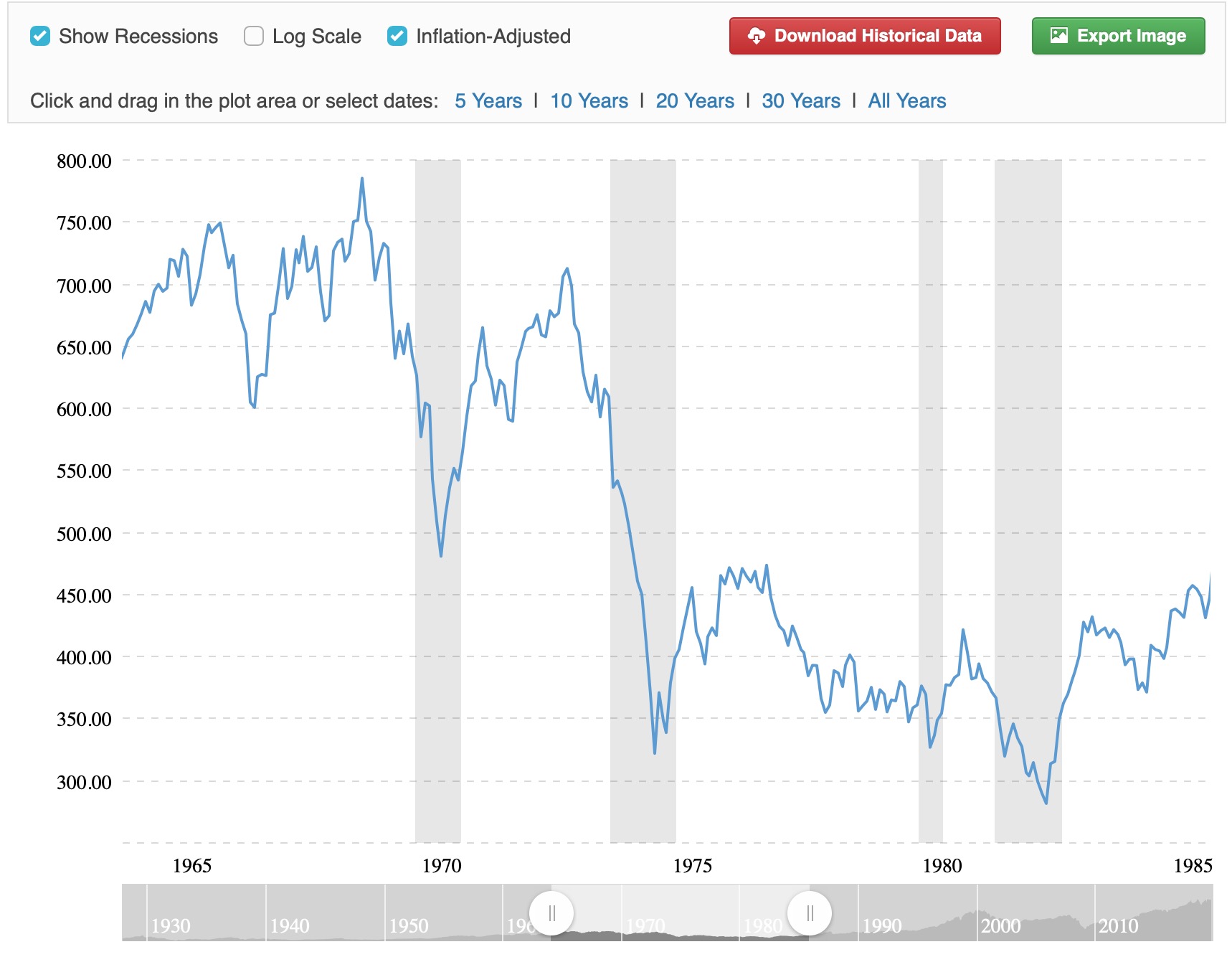

Though to be fair, 1950 till today is not a realistic timeframe for a personal investor’s.

Speaking of awfully periods of time, and if we adjust the S&P 500 for inflation…

When you show the charts like this, it makes more sense for something like “Ray Dalio’s All Weather Porfolio” when you already have a lot capital and want to invest all of them. The more you have, the more conservative you might tend to.

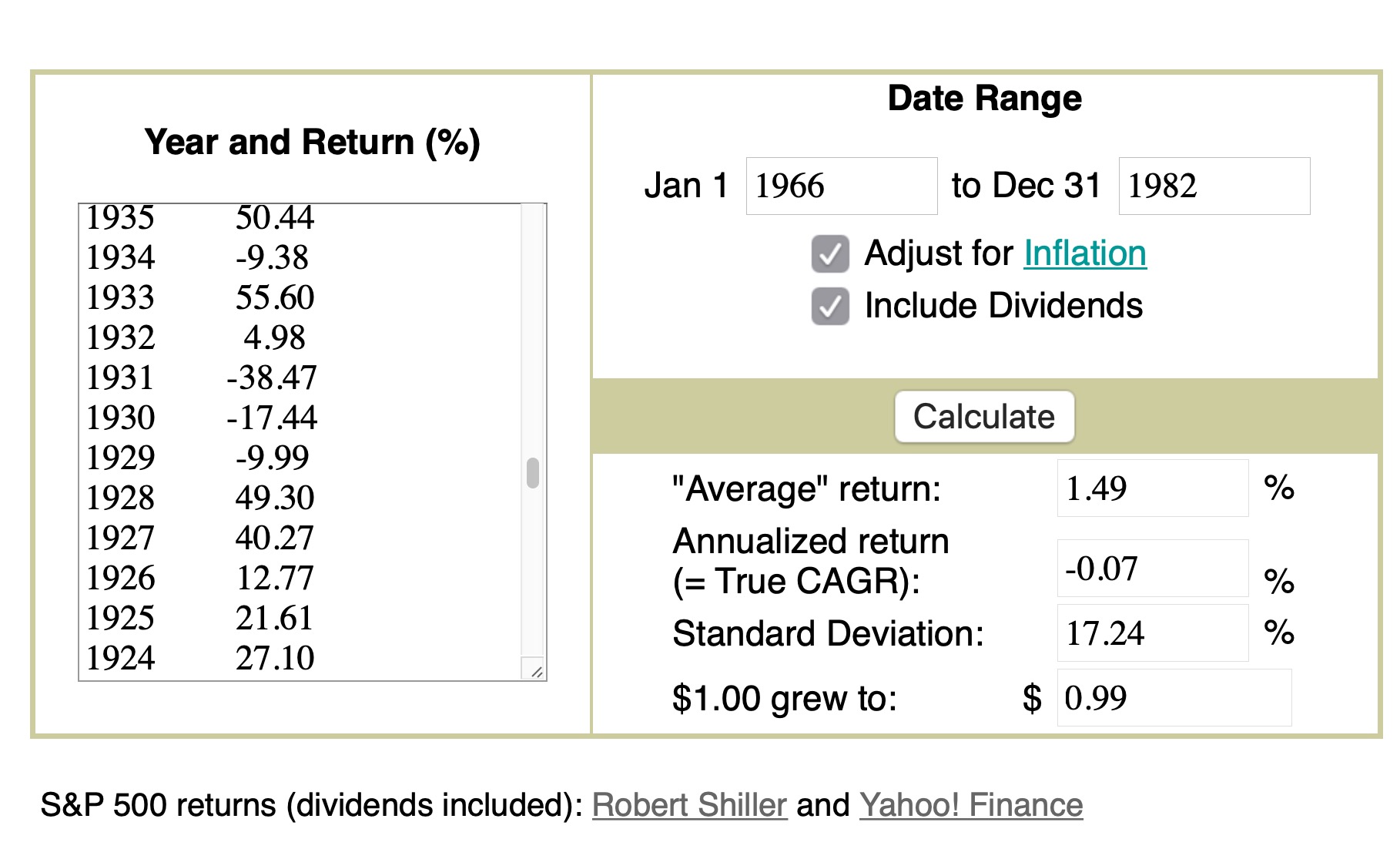

PS: Or for a more recent timeframe, try to calculate for Jan 2000 through Dec 2012: -0.79% real (adjusted for inflation) annual return, including dividends.

Granted, you could consider yourself quite “unlucky”, had you invested a lump sum at the beginning of these periods. And these returns are far from the long-term average.

But any way you slice it, 13+ years is a pretty long time span, and 2012 wasn’t even that long ago. For me it serves as a reminder that one shouldn’t rely or plan too firmly stock market returns - or discount “timing the market” altogether.

This is very interesting, I didn’t know about this. Somehow it looks a lot less “risky” than full VT but also has a lot less upside? Reading around it seems it doesn’t underperform the S&P historically by much (and on average) and is safer during large recessions. Anybody here has experience with this? Any downsides I’m missing?

Yes, in the past bonds performed very well and had very low fluctuations. So you had steady uprise 4%-5% p.a. thanks to high bond allocations. Since 2008 crash central banks to “stimulate” the economy went with interest rates so low, that they destroyed the borrowing money by making it ridiculously cheap and thus now bonds perform like crap. That’s why it will be hard to repeat the previous success of “All-Weather” or any other portfolio with high bonds allocation. Burton Malkiel in last “Random Walk Down Wall Street” suggests one should replace the bond allocation with low-volatility dividend stocks (utilities and others). Another, alternative is to just accept the wild ride and go full stocks (+ some cash), and that’s what I’m doing.

Thanks to all the comments and nice input, I’ve established a conservative funding strategy (10k/month into VT) so that if a recession comes in ~2years I will still have capital left to keep buying at a good rate. For the time being, I won’t do anything fancier and I’ll keep things simple (too busy with life).

However, when trying to implement this strategy I think I’ve already fallen into the mistake of timing the market, and I was wondering if I can get some sage advice on this. I invest once a month, typically by the end. I transfer money from my post account to IB, then put a limit order to convert to USD, which takes a few days but given how things fluctuate it’s reasonable. Then, instead of buying VT at market price I place a limit order too (here’s where timing the market mistake comes in). The first couple of months, I did that at a price very close to the current one, so order was fulfilled rather fast, but then I saw price dropped even further. Therefore, last month I placed a very aggressive limit order and since VT has been rising, now my price is very far. I am thinking of doubling down this month (just increasing the order and keeping the limit price) but I may be going down a rabbit hole with this. On one hand, it makes sense because it eventually will go down (will it?) so I will buy at a lower price, but on the other hand I don’t know when and this is very aggressively timing the market. Am I missing some angle here?

Since I blame this on my lack of experience but also on the lack of automation (if conversion/buying was done on a pre-programmed basis this would not happen) I was wondering as well if anybody had a system to do all this process automatically. I know I can automate Post -> IB transfers, but I was wondering if all the IB stuff can be done automatically, given that there is some manual calculation to be done every time. I read the “I Will Teach You To Be Rich” book and, while many of its views are “incompatible” with the Mustachian approach, there are many teachings to get from there, and one of the most interesting one is automation. This is easy in the US, but I have not found anything like that in Switzerland. Maybe I failed to find the correct tool?

Love Ramit Sethi’s book too, it actually got me here… !

About the automation, did not find something I really like. Except the “Robo Advisors” which are booming left and right. But they could do much more, than I am actually looking for. I want a simple 1x month order form to buy a specific ETF. Also the Robo Advisors do charge some money - cheapest is 0,5% per year (more info see below).

Link German:

And about the timing to buy. You have to experience it by yourself. My experience so far was the following: I bought by the end of the month, the market went down 2-3%. Next time I did wait a few days/week to catch a potential dip and the market went up 2-3% during that time… So my personal conclusion so far is, that when I buy blind by the end of the month, I don’t watch the market so closely and that calms my nerves. So that I can much easier focus on other things in life/business (than watching the performance of my ETF’s).

When in or near Switzerland, buying a principal home is a valid reason for withdrawing pillars 2 and 3. Moving to Spain makes you eligible for another withdrawal reason: permanently leaving Switzerland. In the EU this allows you to withdraw the part of money that is “überobligatorisch”. So you will be able to withdraw all your pillar 3 money and the super-mandatory part of pillar2 when in Spain. The mandatory part is indicated on your insurance certificate as “BVG-Anteil” (amount under BVG law). The difference between the total amount in your name minus the BVG-Anteil is the money you can withdraw as of now (parliament is discussing cases where people moved abroad, withdrew pillar2, spent it all and returned to claim social welfare. Might be that the withdrawal rules change in the future).

If you have some cash left and plan to move to Spain only in 3+ years, you can consider paying money into the pillar2 pension fund (if they allow you to), which you can deduct from your income. There is a risk-less profit to be made. After 3 years it will no longer be taxable when withdrawn.

I recently withdrew my pillar3a money in Luxembourg and have described the steps here. Withdrawing pillar2 should follow the same process - more or less.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.