I was wrong about removing tariffs “next week”. It was actually “the day after announcing them” xD

1 Like

It’s a shitshow honestly… I’m going to ask for more offers this weekend, will let you know.

Those penguins are going to party tonight

5 Likes

@Cortana

You a are well known four your incredible timing on equities ![]()

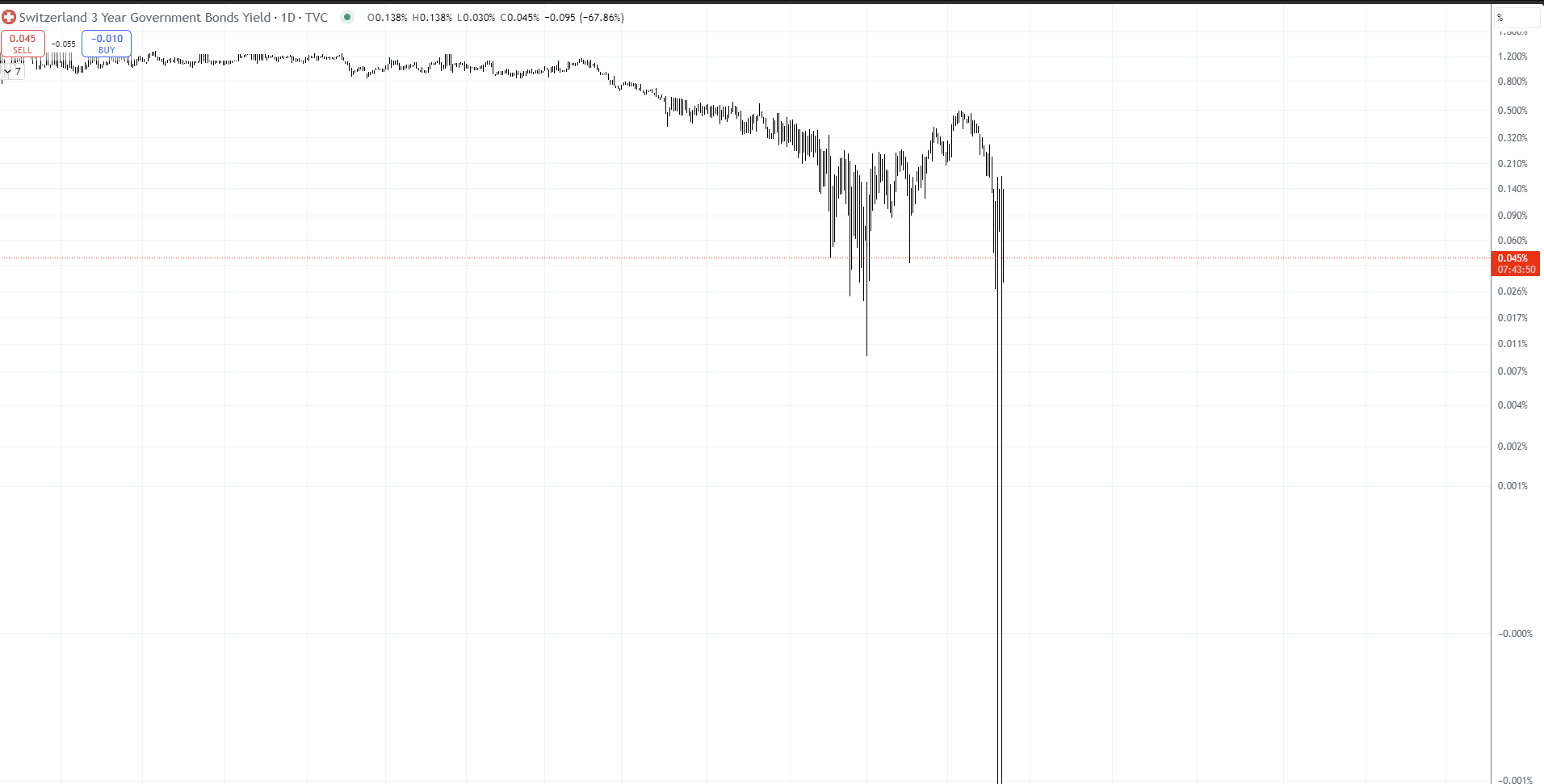

Less for the SNB rate forecast for unknown reason. ![]() With the swaps turning negative can we expect a negative rate already in June?

With the swaps turning negative can we expect a negative rate already in June?

they influence the short end of the curve… less likely to dramatically impact the long end (5y+) unless the market things the rates will stay low for a long time.

For both long and short ends, it also depends on what is “priced in already”

1 Like

These are quote from ZKB? Why does it differ from the data of Investing ?

With the current forex rates 0 is definitely coming in June… Hopefully we can count on Donald to keep up with the good work ![]()

1 Like

I don’t know why but I’m pretty good at interest rate forecasts ![]()

I excpect 0.00% in June for sure. But I think SNB will hesitate to go into negative territory again. Maybe they will first try to intervene on the FX market before going down that route.

1 Like

Honestly I rater pay few hundred francs more mortgage instead of my portfolio losing 6 digits.

1 Like

By the end of year 2024 SNB had on its balance shit

-325 Bio USD

-293 Bio CHF

-302 Bio EUR

-10’000 JPY

-1000 Bio Others

-80 Bio of Gold

Given what the central Bank has already lost a lot this year. If that crisis carry on with rising Franc that sounds risky buying huge amount of foreign currency.

I currently bet on a negative rate by June

Does SNB still hold stocks?

SNB data portal (I’d guess that securities is mostly stock).

I’d guess there’s a lot of bonds under the Securities position.

Judging by this page, I’d say around 25% of Securities were Equities at the end of Q4 2024:

2 Likes

150bn if I read this webpage correctly:

1 Like

3/4 is in bonds according to an interview with the head of asset management from SNB.

I see it less of a risk because the CHF is strong historically, so foreign currency purchases will only increase even more in the future. If CHF weakens long term (foreign currencies appreciate), then the SNB would just exchange foreign currency for CHF and then there is less CHF supply which would lead to CHF appreciation. The foreign currency purchases are just an instrument to influence CHF.

If my interpretation doesn’t make sense or is wrong, please feel free to correct ![]() .

.

1 Like

According to slightly current negative rate on 1 and 2 years Interest rate swap SNB is becoming more and more likely to come back in negative rates already in June.

Would be a big signal to avoid foreign CHF buying

I don’t believe they’ll take such action in June, bringing rates down to zero is already a strong signal, and they had anticipated the EUR/CHF ratio to reach 0.92 at some point this year. That said, depending on how the situation develops, the possibility of negative rates emerging in September can’t be ruled out for sure. Another influencing factor will come tomorrow with the decision from the BCE.

Just closed today with global bank for 0.89 % all-in SARON mortgage (including margin) - indefinite term - 1 tranche.

Thanks everyone for your feedback and advice. Appreciated!

8 Likes

that’s a great rate! could you tell us how much was your initial payment % ? more than the standard 20%?