People in the West haven’t experienced true, large scale, unspeakable horror for 80 years, I believe that’s made us in the West think it’s not possible anymore because we learnt from our mistakes. Looking a bit past the borders of the collective “Western Democracy” countries (you know…about 75% of the rest of the world by number of countries) tells me people are just as shit to each other as they always were.

You know the saying: Bad times make hard men (ok, let’s say people), hard people make good times, good times make weak people, weak people make bad times. We’ve had good times for a pretty LONG time now, here in merry West.

I just realized that break-even is achieved earlier in Februar '15, so 179 months (14.92 years), but only if you sell right then, as there’s a few ups and downs after. July '16 is the month after which the index has never dropped again under the high of March '00.

if the time period is “short” enough, pick a suitable starting point on your chart to prove your return theory, e.g. pick the end of 2011 to arrive at an impressively high CAGR (or pick your suggested March 2000 high for proving the opposite).

(Just to be clear, this is not to pick on your analysis – which I find great – just that somewhat volatile charts over a relatively short periods of time allow one to tune return numbers by picking a suitable “inception point.”*

Any sufficiently long enough obvervation period – 50 years plus? – will likely filter out this noise – or indeed point out the times when the investment theory, or rather practice, actually changed …)

<sarcasm>

more importantly: AI will replace us all within months now – fear for your life!

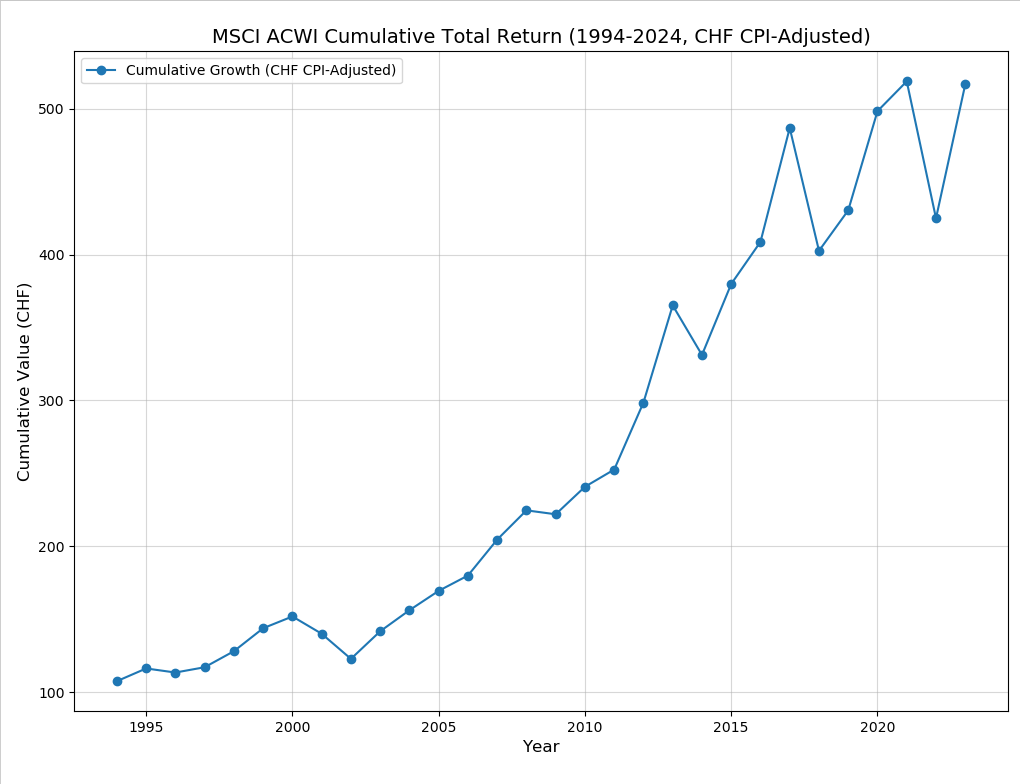

Here’s why: I asked ChatGPT to do your work, i.e. give me the “return chart of MSCI ACWI total return in CHF CPI adjusted for the past 30 years”. After all, this is just mostly publicly available data, and AI is smart!

Answer 1 gave me (in text form) “7.9% CAGR for the past 10 years” and “8.22% since 2022.”

Answer 2 (after explicitly asking for a chart) gave me instructions on how to install Python and a plotting library and gave me a Python script I should run.

Sheepishly, as I am just human intelligence, and because everyone knows how to run Python and has a spare Python runtime ready to fire,** I added the suggested library to my existing Python installation (if only AI could do such computery things at some point) and ran the suggested script.

It gave me what I asked for deserved, I guess, plotting a chart of numbers going up and down the zero line.

I realized my (human) mistake and asked for a cumulative chart of this.

Answer 3 gave me a lengthy explanation on how to calculate cumulative returns via compounding and also provided me with a new Python script.

Being the sheepish human I ran this updated script and arrived at this output:

It seems to me the chart above has some sort of correlation with the previous one, but only directionally?

Anyway, if you overlay the latest chart with the numbers/graph put together with @assemblyrequired , it’s basically a 1:1 match … no?

Good luck with spotting any significant differences.

</sarcasm>

To be fair, in my AI journey I (eventually) also ended up with an about 500% return for the question I asked.

So … squinting enough, we arrived at the same (averaged) results.

Of course, you only put a few years of your life into collecting, calculating and graphing your numbers, while AI spend about a billion USD just on electricity for arriving at the same results.

* I see this with tracking the performance of my own stock picked portfolio ETF: my actual inception is June 2019 and since then I’m mostly in line with the S&P 500’s performance. Shift my inception point to January 2020, and I lag the S&P 500 by about 29%. Shift my inception point to November 2021, and I lead the S&P 500 by about 11%.

(measured in USD, not inflation adjusted

** Pretty sure most people do it like me: I am typing this on my Windows PC or my Macbook, depending on where I sit in our apartment. From whichever client I ssh into one of my Linux virtual machines running on an actual physical “server” (which also runs on Linux) – in my case a fanless nano PC without any physically moving parts (somethink like this) to extend lifetime – to do command line stuff.

For GUI stuff I run corresponding VNC GUIs on the virtual Linux machines, and on my main Python development VM I just added the corresponding graphing library as an Ubuntu package (no need to use pip or anything fancy, let alone compile things), and jolly, there I was ready to run those AI provided scripts and snipping them graphs after connecting with my VNC client from my actual client.

I know, more sophisticated folks do it like I (used to) do it at work, i.e. package and rung things on docker (or some other PaaS), but we’re only talking about home use to serve our most advanced AI here, so please give me a break for taking shortcuts here …

I’m wondering: does it make sense to correct these numbers for inflation? Or would a chart with nominal values also provide a (different) benefit? Maybe when comparing to “cash under the mattress”?

With nominal values, March '00 would still be the worst time to invest, with a recovery time of 86 months (7.17 years), followed by the GFC (84 months/7 years).

My comment is probably orthogonal to your hard numbers, but I’ll still try:

I think (not) “adjusting for inflation” matters most to the hypothetical person not willing to adjust their lifestyle no matter what, to economists (and maybe especially politically motivated ones) calculating “overall consumption and spending” and to people with a super tight budget when it comes to the basket of goods in the basket used to calculate inflation.*

Inflation still matters, but perhaps a little less, to people who will adjust their lifestyle. Maybe I’ll buy the Migros brand (or even low budget Migros brand) if the Coop “Bell” Cervelat suddenly costs more than I am used to (and if/when I actually notice it on the receipt that I did not used to look at forever).

There’s of course also companies purchasing goods and services, often probably with less leeway of adjusting their consumption patterns or paths, but they will adjust, too, just maybe with a little more lag than an individual.

* In my mostly affluent bubble of colleagues and friends, the person most vocal (or maybe the only person?) complaining about inflation was a 17 year old in their 3rd year of their apprenticeship, making about 1/6 or a 1/5 of what they will make afterwards. If your salary is, say, 1k CHF, you feel inflation differently than if you make 5k or 6k.

You feel it differently if you have no salary that outpaces inflation, but instead nervously watch as the real value of your assets are assailed by inflation.

I like the “Rolling returns” feature of Lazy portfolios for that. It’s not perfect (returns in USD, EUR or CAD, bonds as either US or global (including EM)) but it’s good enough for an approximation for me (the future won’t be exactly like the past anyway so we need to account for flexibility in how we interpret data):

100% stocks, all world since 1970, in USD (total returns):

I would say it doesn’t: we’re comparing stocks to the alternatives, that also suffer from inflation. It offers a better way to immediately compare their results to cash without having to add it as an alternative itself. Many people consider going to cash when they get out of the stock market due to anxiety/fear, too, so that’s often the comparison they should be trying to make.

That being said, I do take inflation adjusted returns when using returns in USD and am trying to assess what that would represent in CHF without going through actually converting the data. I consider that in a theoretical and broad sense, our respective inflations and returns discrepancies should cancel themselves when taken into account on longer periods of time and the inflation adjusted returns are more comparable in some way than nominal returns would be.

Accounting for inflation is useful to me when determining average past returns and then using that number to calculate a possible future pension.

When talking about “minimum period for stocks”, we’re talking about maximum duration for recovery. So we should use nominal values, maybe substracting savings account interest rates.

I think the old farting part on my behalf is mostly because I’m still so nervous about how it will actually work out despite having run the numbers over and over in spreadsheets at the peak capacity that the Google Cloud can provide …

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.