So in our example of 1’000’000 wealth, if you held it all in an ETF, and would earn 20’000 dividend (Vermögensertrag), the other 180’000 of income coming from the salary, the “Bremse” would be 25% of the dividend, so 5’000. The calculated total tax is still 65’796, but the wealth tax part is only 4’140 (52234*900/11355). So the Bremse has not been reached, and the tax has to be paid in full.

I guess this tax relief is for people with high income from capital and as said, only applicable in canton Bern. Still, I don’t see where the 68% marginal tax rate, that you mention, is.

Some Numbers for an example do not try to make any similarities with a real case.

Case 1 : Wealth: 1’000’000 Salary: 180’000 Dividend 20’000

Wealth tax: 6’000 Income Tax: 50’000

Hey, the wealth tax is larger than 5’000 (25% of 20’000) then I get a discount of CHF 1’000 on the wealth tax so it stays at 25% of 20’000.

At the end I pay CHF 55’000 of tax al included.

Case 2: Wealth: 1’000’000 Salary: 180’000 Dividend 21’000

The marginal tax rate on the income is 41% then based on case 1:

Wealth tax: 6’000 Income Tax: 50’410

Once more, the wealth tax is larger than 5250 (25% of 21’000) and I get a discount on the wealth tax of CHF 750.

At the end I pay CHF 55660 of tax all included. (6000+50410-750).

I end up paying CHF 660 more of tax for an increase of CHF 1000 of dividend. This is 66% marginal tax on dividend.

The problem is that all the people interested in FIRE try to get in direction of case 2 (I get the income from my investments rather from my working hours) but it is (at least in a given ratio) very tax inefficient.

Capital gains on your shares are not taxed in Switzerland. If taxes on dividends are too much of a friction for you, this should tell you where to concentrate your investment income.

Thanks, now I finally get it. So in a Case 3, if you had a dividend of 24’000, there would be no more discount (25% is 6’000). Then in Case 4, by a dividend of 25’000, your marginal tax rate on the last 1’000 would only be the 41%?

Yes capital gains distributed by Swiss companies, mostly in the financial sector, are real yummy cakes. But it is difficult to tell which company will distribute them and which year. UBS and CS gave them in 2017 and 2018 but nobody knows if it stays in the future. I expect some capital gain distribution from Novartis if they decides to sell the shares from Roche they are invested in but nobody knows if this will happen one day.

You’re still better off earning these 1000 Fr than not earning them as long as the marginal rate is under 100%. And this is just a small temporary spike in marginal tax rate graph, after you cross this threshold, the rate is again 41% something, no? So it’s the 41% rate that you should still pay most attention to

Also don’t forget 5-10% AHV. All AHV you paid on above first 86k part of your salary doesn’t count towards your pension benefits and you can’t have it reimbursed when leaving. Just another f’ing tax.

These gains are already priced into the stock, so I don’t understand what are you so happy about when they just pay you your own money. I’d rather call it a tragedy that they can’t do anything useful with the money but to give it back. Looks like bonds just with extra steps and risk

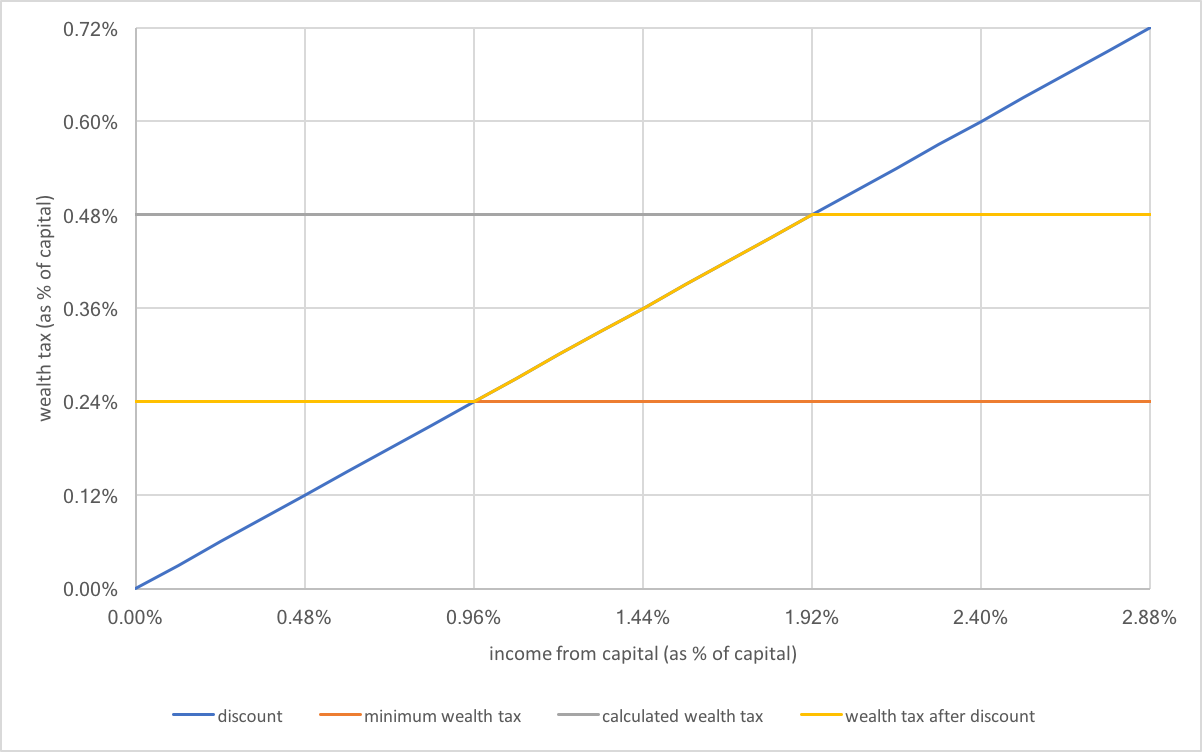

I put the whole thing on a chart. So let’s say the calculated wealth tax is 0.48% of your capital (grey line). If your income from capital is less than 4x that (1.92%), you get a discount (blue line). However you have to pay at least 0.24% wealth tax. So the final tax is the yellow line and the total discount is the difference between the grey line and the yellow line.

So if all of your money is in the stock market, then the dividends are usually higher than this 1.92%, so you shouldn’t worry about the discount. And how is it with real estate? (rookie question) I assume income from rent is also counted as income from capital? If so, the rent is usually also higher than 2%.

The rent is also counted as income from capital and is higher than 2% but read the following.

One strategy I like with housing is buying an old building in poor condition but still able to be rented. Then you invest all the money of the rent in renovation of the object so the house is some wealth not producing any income. Then after 15 years of this game you finally have a house in good condition which did not cost you anything to renovate.

The investment of profit or capital gain within the company is maybe efficient in tech companies with fast growing rate but probably inefficient in a lot of companies that retain the profits.

If the company works fine there is another capital gain distribution next year.

As investor you need cash flow, maybe just to pay your taxes. It also gives the possibility to invest in another sector than finance.

It is not just like bonds with more risks. One example, with 6 capital gain distribution from 2010 to 2015 Zurich gave a tax free dividend to swiss shareholders which was worth 7% of the share price each year. During the subprime crisis, the capital gain distributed was even worth 10% of the price of the share. Bonds providing this kind of coupon are far more risky than shares.

And where did their stock go? Nowhere! How did a few other insurers who are known for reinvesting profits do over same time period? MKL, BRK - 2.5x’ed your investment. Reinvesting beats sitting idle on cash.

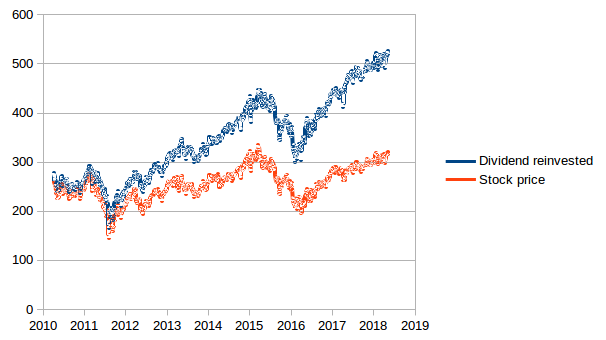

Yes reinvesting beats sitting on cash. By the way if ypu calculate the price of Zurich with dividend reinvested you get a progress by a factor 2 over the last 8 years not far from your examples for MKL and BRK. See the plot next.

My point is that when the managment of a company believes he is more knowlegeable what to do with the cash than what the shareholders woud do with their dividends then it is the point where a company may well begins to be financially inefficient.

Exactly, the allocation of earnings is a topic in its own. it is a function of:

what is your current return on capital employed

is it possible to reinvest your earnings at a decent return

That gives us 4 categories :

weak ROCE, weak reinvestment possibilities -> pay dividend, the shareholder has better investment opportunities with the money

weak ROCE, strong reinvestment possibilities -> that would indicate a radical change in the company, for instance when Buffett bought Berkshire and reinvested textile earnings to buy an insurance business

strong ROCE, weak reinvestment possibilities -> pay dividend, if you reinvest the earnings at a weak rate you are destroying value

strong ROCE, strong reinvestment possibilities -> reinvest everything, and enjoy your cash compounding machine.

Basically, one of the tests to check if earnings have been retained wisely is to check if, over a given period (let’s say 5 years for instance), one dollar of retained earnings has been translated in more than one dollar of market value, i.e Delta(Market Capitalization) > Sum (Retained Earnings).

If the check is failing, then the earnings have been wasted and the investor would have been better off with the dividends.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.