If you’re doing daily rebalancing, it’s going to be a bit of work for a buy/hold portfolio, it can be automated but at this point why not use something like futures? (that you also need to rollover and keep cash aside)

(and I think you’d also need to have your cash invested at the risk free rate, so not just sitting as cash at IB)

edit: SPYQ is probably a better idea if done with ETFs, it rebalances quarterly (but TER is fairly high)

This route can make more sense. But what happens if you dont rebalance (and thus selling on the way down, just like the daily levered funds do) to match your desired leverage is, that the leverage goes higher and higher the more it goes into drawdown. This then increases your risk and you are betting on mean reversion there. Which you can do (it worked in the past), but you need to be aware of that and most people aren’t. You are actively letting the leverage ratio drift higher.

Also another problem with a margin loan is the high financing cost (benchmark +1.5%), and if you deduct this from taxes, you’ll have a lower DA-1 return, as that offsets it (super weird ruling on that in my opinion).

I hate it. The herd usually invests on margin just before the top.

Key Trends and Context

New Record High: This figure represents a new all-time record, surpassing the previous record set in June 2025, when margin debt first crossed the $1 trillion mark.

Rapid Growth: The amount of margin debt has been on a sharp upward trajectory over the past year, increasing significantly from the low it reached in late 2022.

Correlation with Market Performance: Margin debt levels are often considered a measure of investor sentiment and leverage. They tend to rise when the market is performing well, as investors become more confident and borrow to increase their exposure to stocks. Historically, significant increases in margin debt have sometimes preceded market peaks and are seen as a potential risk factor, as a market downturn can trigger margin calls and forced selling, which can in turn accelerate a decline.

I always invest on margin, but with the lowest multiplier when the market is at its high (like now) and the highest multiplier in bear markets…

Buy’n hold 150% stock index is almost sure going to zero in 20 or 30 years. There will be a collapse of 66% or more and…adios dinero. OK, you will get the only tip you should ever listen to from your broker: a margin call.

A leveraged ETF will be not much better, your kid may lose only 99% because it sells after each down day and buys after each up day.

(Do as I say, not as I do. I always invest on margin because “cash is trash”…).

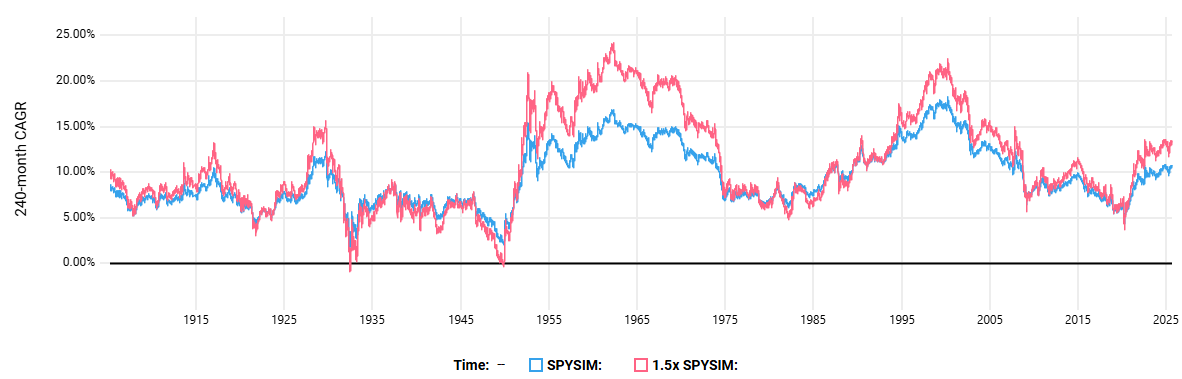

Since 1885-03-20, not even the Great Depression managed to give a 1.5x daily levered US market a drawdown of -99%. Over 20y span the CAGR only touches 0% on two short occasions. Link to testfol.io simulation.

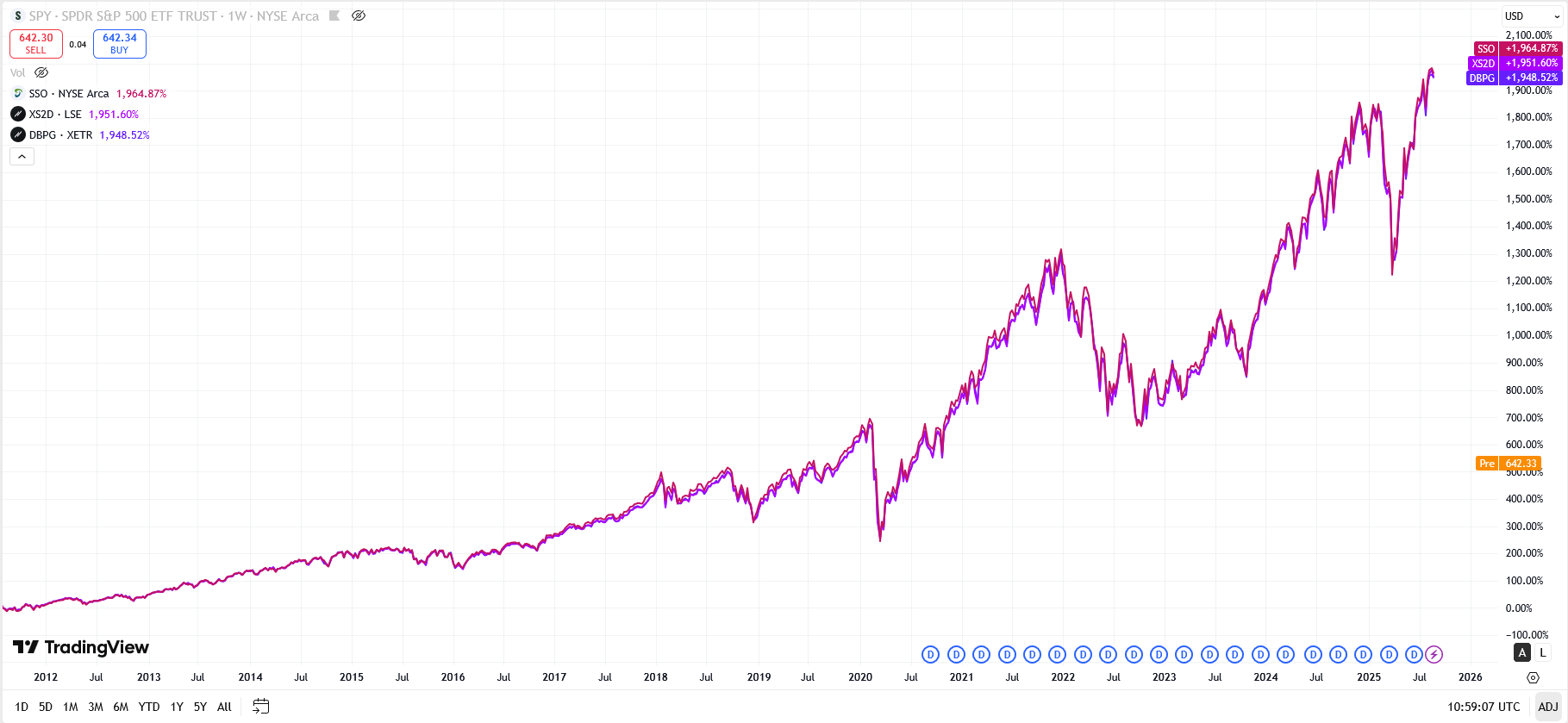

These UCITS products can be as efficient as their US counterparts. Case study 2x S&P 500:

It depends a bit on the day (different exchanges and closing times), but this UCITS ETF (DBPG / XS2D) can keep up with the US ETF (SSO). Over more than a decade, the annualized difference to the US ETF is low. The worst day I could find was -0.4%, on many days it is about 0% and in recent years it was also often positive. But I admit, a rigorous analysis on hourly data would be more pleasing.

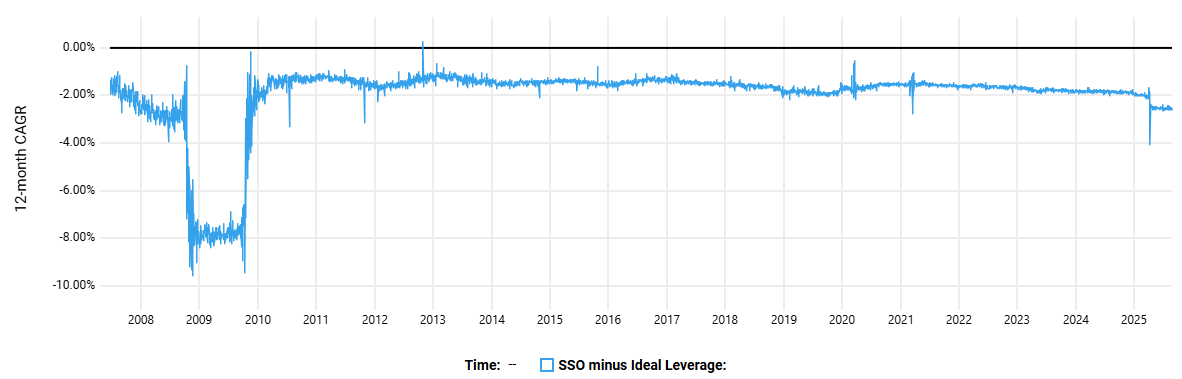

Over all available data it has an annual excess cost of -2.0%. Since the S&P 500 costs next to nothing, this can be attributed as the excess cost of one unit of leverage. It is more expensive than IBKR margin (starting at -1.5%), futures (-0.5%), and box spreads (-0.3%). But it can only blow up itself instead of your whole portfolio.

Because if you don’t get institutional financing cost of ~.5% over risk-free (and a reasonable TER), then it’s not worth it in my opinion and you should do it yourself.

To me this new etf gets worth it at 0.5% TER + 0.5% excess financing cost. Anything above and you should use margin or other means.

Interestingly, if you set the same total leverage with SSO or UPRO and compensate with CASHX you get the same CAGR for both. I must say, I have trouble wrapping my head around this effect. Also going from 2x to 3x does not double the cost but only makes it 1.5 larger. Which makes some sense, but also doesn’t: The leverage part that costs something only doubled from 1 unit to 2 units.

If you compensate with more realistic cash that has some markup (on both sides), the one that uses less cash wins, of course.

If you compensate with SPY ETF (50/50 UPRO/SPY vs. 100 SSO), UPRO wins. Probably, because you need less of the expensive UPRO/SSO TER.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.