Equities can have a negative return over a decade and obliterate your 3x leveraged position. Do you constantly rebalance without new contributions and erode your retirement portfolio?

You are more thinking with abond tent right? Meaning you only consume your bonds until equities recover?

What if that‘s not enough and you run out after X years, meanwhile volatility decay has eroded your equities?

What do you do then?

daily reset leveraged etfs are definitely not something I would let near my retirement.

First, this is not a leveraged portfolio. It is equivalent to 91/9. You are borrowing money with one instrument while earning interest with another instrument. The difference in rates is not in your favor, at least usually.

What you can do instead is to keep unleveraged portfolio, but consider an option to replace unlevereged ETFs with leveraged one while keeping the same exposure, i.e. sell 60k worth normal ETFs, buy 20k worth UPRO, withdraw 40k.

This is equivalent to borrowing against your portfolio, but might be easier to implement. You would need a strict guidelines when to start using the leverage and, probably more important, when to stop using it.

I am not completely sure, but my feelings tell me that it depends on what the purpose of 20% fixed income is.

If you want to use it as a part of the portfolio and are expecting to rebalance it into stocks when they go down, and if this part is actually accessible and not, for example, locked in a fixed term deposit, then I would say 75/5/20 is equivalent to 90/10 and you can make your life easier by not using the leverage.

If, on the other hand, you consider these 20% to be your fixed income tent and reserved for consumption during the next years, then I would say it might make sense, if only psychologically.

I can imagine that one consumes 4% of the original portfolio per year from the cash buffer and refills it by selling stocks only when the benchmark index is within 5% of the previous ATH. I would also reset the nominal value of these 4% and rebalance from stocks to fixed income if the portfolio value grows above the original one. Should happen quite often .

In this case, you have an option to sit through 5 years of a downturn, instead of 2.5 years with 90/10. But the advantage is purely psychological, I would say. Rationally, you can start borrowing one way or another when you run out of money and not earlier. Rationally I would say there is no point in borrowing money when you don’t need to.

Sorry, came a bit long and I hope you understand what I mean.

P.S. Furthermore, there is a question of what to do with dividends during a downturn. If you don’t reinvest dividends, you are consuming your portfolio, just slower. It means you need a larger price increase to recover losses of stocks.

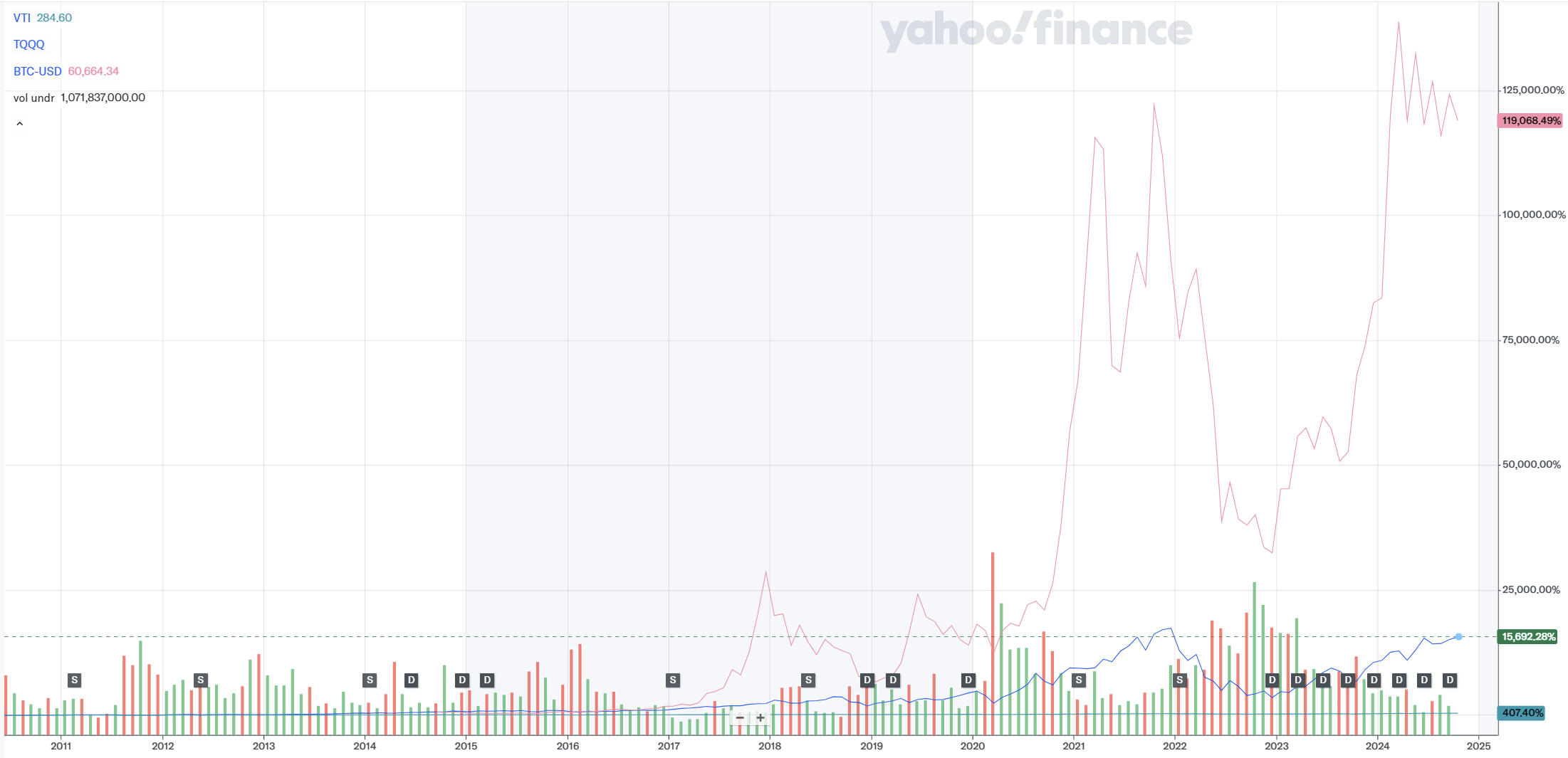

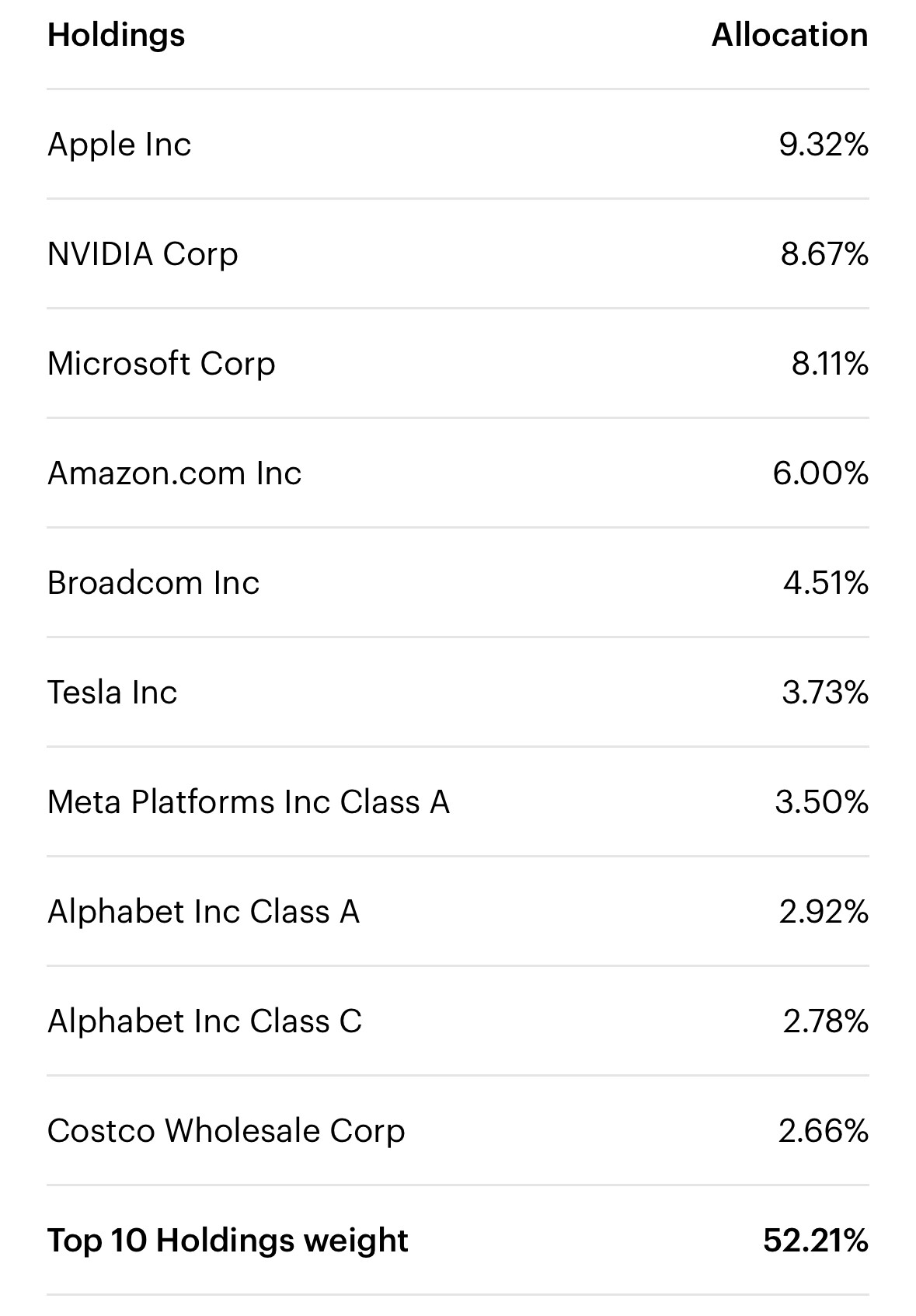

Absolutely. This is why I take companies listed at Nasdaq as a basis - we can debate, if it is wise to have a leverage on an index with only 100 companies and ca. 52% IT companies.

I would ponder if it is wise to use a 3x leveraged ETF relying on an index that isn’t the one used to trigger circuit breakers. A 33% daily loss of value would wipe out the ETF without a chance at recovery.

Is it likely to happen when circuit breakers calibrated on the S&P500 are enacted? Probably not. Can it absolutely not happen under any circumstances? Who knows? Leveraged ETFs based on the S&P500 are safer.

I can’t come into your home and tie your hands so you don’t finalize the investment but I’ll set a reminder to take news of how well your investment is holding when the crisis will have become worse, stocks lost 40%, you may be worried you’d loose your job and/or your partner might leave you because of the state of your UPRO investment.

Based on my understanding, these leveraged ETFs increase risk to the portfolio and also returns. However it seems that the returns of UPRO are not really 3X of S&P 500. I believe they get suppressed due to sequence of returns. I ran a 10 yr back test and saw 24% CAGR (UPRO) vs 13% CAGR (SP500)

I always thought such products are mainly used by short term traders. It is interesting to see that it is also considered as part of long term portfolio. For me this is too much risk to take and i wonder how can one ensure how liquid these funds actually are. I mean if they get forced to liquidate, the investors would not be able to recover the losses easily without borrowing money themselves and investing in underlying index themselves.

Can work of course. There you also risk the position to get wiped out still. 2000-2008 for example.

Starting 01.01.2000 the position would be close to wiped out multiple times over a decade and take 20 years to break even again in nominal terms (real terms are lookng rather grim still).

Just look at teh drawdowns and how extremely long they are:

It’s even written in their KIDs that the leveraged ETFs are meant to be for very short-term holding

I held UPRO for 6 months or so in the beginning of this year, did a very decent return but in practice irrelevant as I’d only put in CHF500. I figured I don’t have the stomach to hold a substantial amount of money in such a product. I think the big ones UPRO and TQQQ are very liquid though.

I remember that at least UPRO has three circuit breakers to prevent a portfolio going to -99% in a single day. This doesn’t mean it can’t go to -99% over a few months, though!

Yes, but we are continuously investing in ETFs on a monthly basis - why not doing that as well with a LETF? If you do that with UPRO/TQQQ, it does not matter if the investments have nearly been wiped out (which are ideally max 10% of your portfolio), you will be back in the green range again pretty quickly.

I will definitely start this experiment and will continue to increase TQQQ to 10% of my available portfolio. I can imagine to sell parts to rebalance it im another ETF as VTI. In case I only experience draw downs, I will continue either monthly or bi-monthly to contribute to TQQQ, as I am doing now for VTI.

I was wrong, it’s not UPRO that has circuit breakers, but the S&P500 itself. Apparently trading is suspended in cases of 7%, 13% single day drops, and halted for the day in case of a single day 20% drop (Black Monday was at 20.5% in a single day).

Now I’ll get a bit stupid. I was playing around with the numbers of the 9sig strategy I saw on reddit. The idea is holding 60% TQQQ (or other leveraged ETF) and 40% AGG (US investment grade bonds). I’d sub the bonds for cash myself.

One gets the “signal line” by calculating their TQQQ position + 9% (so TQQQ in $ x 1.09)

At the end of the quarter one looks at what did TQQQ do

You adjust by selling the surplus or buying the deficit to maintain the signal line to be [value of TQQQx1.09], so you sell 1% if it did 10% or buy 1% if it did -10%

You calculate the next signal line by taking the final balance of TQQQ for the quarter x1.09

Rinse and repeat until you use lambos for toilet seats.

Obvious problem of this strategy is that if it crashes HARD then there’s no chance to have the liquidity to buy up the deficit, but apparently the strategy is pretty pragmatic about it and acknowledges that you’d still be buying at a discount. It’s basically value averaging by another name.

My original plan was to have some set it and forget it money to plug in TQQQ when we have a nice big drop (I mean really forget it, consider it gone forever and not touch for 10+ years), but I found this strategy and it tickles my craving for being a bit more active than just buying. I like that there is an emotionless system behind it, I like the forced, timed trading and forced selling high/buying low. Would not put more than 5k in this.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.