UBS pension fund interest:

2021: 9.5%

2022: 7.0%

2023: 9.0%

2024-2026: 6-9% expected

UBS pension fund interest:

2021: 9.5%

2022: 7.0%

2023: 9.0%

2024-2026: 6-9% expected

Bloody hell indeed, who wants the stock bullshit when you get this by your employer?

Risk free and no taxes on top ![]()

So why you’re all whining like…because you can’t save pennies on “mustachian” “solutions” like IBKR?

Next time, can you please post this right after the OP?

Hours and hours of our time were wasted* on coming with creative solutions to save those pennies when you could have just ended the discussion right there.

* Of course, that’s why most of us are here for, so thanks for waiting till now to post this. ![]()

I just dont quite understand how is this possible though. Is UBS paying from pocket?

Two main reasons:

That’s probably because they offer clients (plebs like me) active management with 2.8% TER.

No, without kidding though, this sounds really good in fact, if someone doesn’t want to FIRE. Maybe their transaction advisory/investment banking is interested in someone with 12 years’ pharma pipeline experience? ![]()

Oh, stop it! ![]()

![]()

That’s a nice solution, as in works out fair? Or are all the oldies at UBS (I picture Ermotti at the coffee machine) whining about this oh-so-low conversion rate?

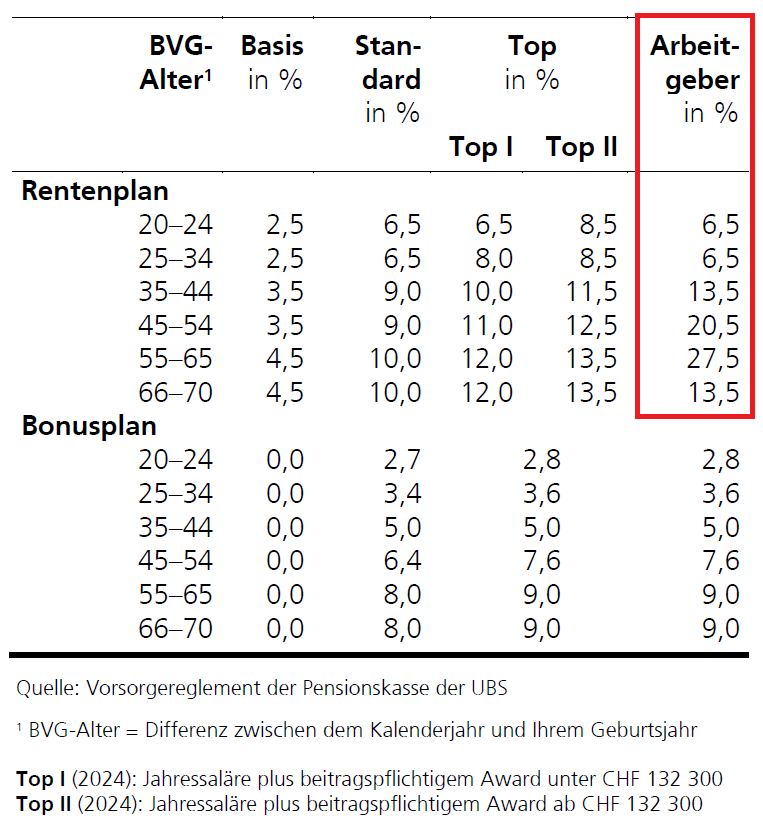

Everybody wins. You might have lower conversion rates, but very high contributions by UBS and probably the highest interest of all pension funds in Switzerland. Check this out:

Lets just assume you stick with the Standard plan and don’t want to overcontribute on your part. That’s 13% from 20-34, 22.5% from 35-44, 29.5% from 45-54 and 37.5% from 55-65. With an insured salary of 75k (most employees at UBS will earn way more) you’ll get to a pension fund of 760k with zero interest if you work there from 25-65. In reality it will be well above 1 million due to interest. Probably closer to 2 million as you will earn more over the years.

Now imagine how much people at Director or Executive Director rank have in their pension fund once they are 60 or older. It’s millions.

This might not always be the case. My partner’s contract specifies a list of securities that both the employee and their spouse (or even unofficial domestic partner) may not trade. Obviously they can not stop me from trading these, but as far as I understand they may then “punish” my partner as they consider contract’s terms violated

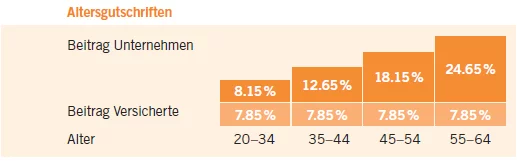

Copy paste from my employer, looks similar.

Don’t know, how they calculated the “Beitrag Versicherte”, since you can choose to contribute eiter 6.5%, 8.5% or 10.5%.

Nevertheless, I always choose the lowest contribution since I outperform the pension fund.

But to stay on topic:

A good quote, which I fully support. The couples of Swiss Francs one has to spend more through the own employer are in my eyes irrelevant and are neglected due to other benefits one probably has.