How to determine which “Income-domestic stock correlation” you are? If you are in IT or Pharm for example?

As mentioned before I don’t think it matters much.

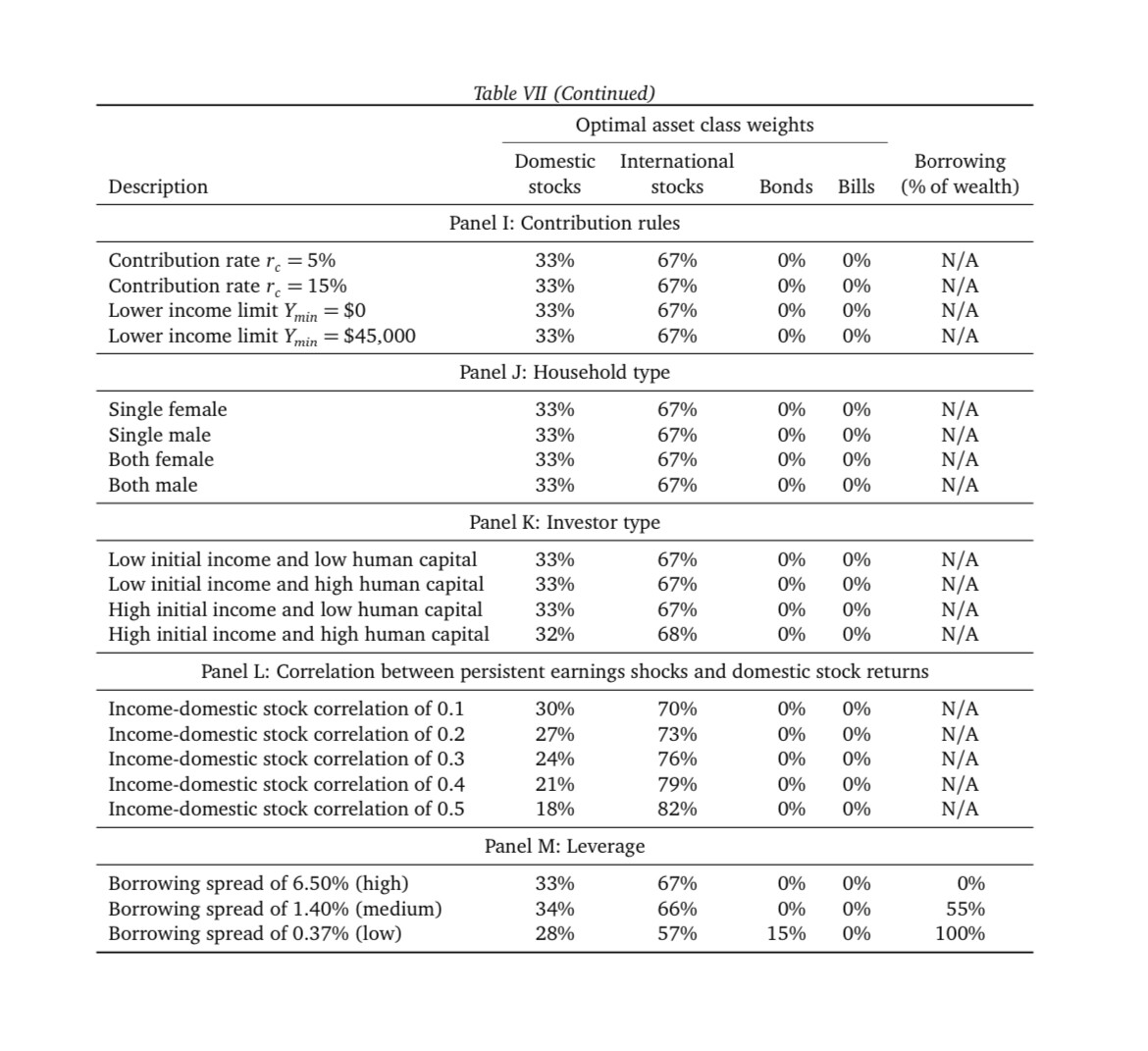

For the base scenario (uncorrelated) the home bias practically can be anything between 10 and 50%. I expect the same thing for any of the correlation rows in Panel L.

I also cannot determine it because its not straightforward. Working in Pharma doesn’t not mean you are correlated to Swiss stock market because Swiss stock market has multiple industries.

So as long as i am between 20-40% for domestic stocks, I am good.

Personally, I think lot of people are obsessed with the breakdown of their geo allocation because they assume it is a predictor of their returns, but in reality it should not matter. The expected returns of all diversified stock portfolios should be same. So the focus should be on risk management rather than return expectations.

When you say Europe do you mean Euro zone?

Domestic in the mentioned paper means “Stock market with the same ‘local’ currency”.

For instance someone leaving in France he should consider the euro zone for the domestic part percentage.

Since there is no ETF covering only the eurozone I suppose the next best thing is to slightly overweight Europe?

On the other hand does it worth splitting a single World ETF (VWRL etc) in multiple ones for a ~5% tilt?

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.