I don’t entirely agree with this. When I first started work, I had a lot of student debt and was earning just 20k per year, which in London doesn’t go very far.

I made the conscious decision to spend more than I earned and go into more debt as I expected to get pay rises and so was smoothing my consumption by spending future higher wages.

In the same way, I do now reverse smoothing, where I spend less than I earn so that I can spend more when I am retired and not earning.

BTW the lump-sum vs. DCA is when you have a large amount of money to invest (e.g. not having anything invested previously, inheritance, etc.). Here it’s mostly about which frequency and timing to target for regular contributions.

Same here. I guess there may be natural tendencies to spend or save and if you are a saver, then the FIRE route might be easier (at least until it is time to pull the plug on earning and actually spend your pile).

I get it, I am very allergic to debt though, even my car loan which I could pay off today if I wanted to is a mental burden for me. In fact I took the approach to “gamble” that growth/year will be more than 7% (which is my car loan’s interest, in Greece) and pulled the cash I had to cover this loan to use it for investing. It worked out but won’t be doing it again!

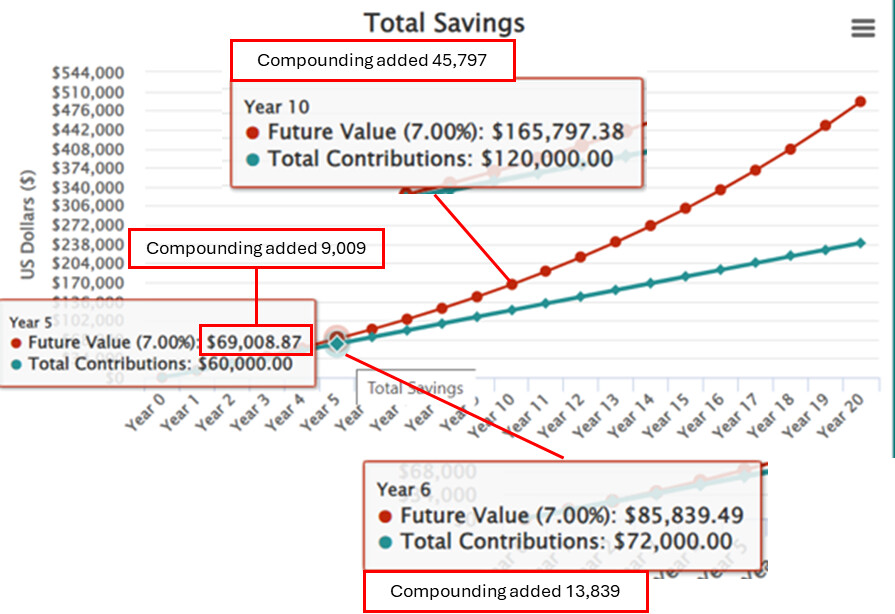

Actually, unless I’ve done something stupid, the compound growth per month starts being more than what the investor contributes by year 6, and 4x more by year 10 (after which in my opinion it makes little sense to continue trickling). Assuming 1000/month, 7% CAGR, 20 years:

This chart looks so professional

Just to be sure, I get it

You are estimating the point where the annual return from the investment goes beyond annual contribution (12000 in this example) right?

Between year 5 and year 6, the future value increased by 16.8 K and 12K was monthly contributions, so the compounding added only 4.8K. Isn’t it? Your chart shows something different

Come on, it looks like it was cobbled together by a cryptobro on MS paint

See that’s where I may be wrong and end up red-faced. My mental arithmetic says that by year 6 the investor has contributed 72k, and compounding added 13.8k on top (ie more than 12k which is the annual contribution). I am happy to be corrected.

But the consensus is that lump sum beats DCA (on average) if you immediately invest the lump sum when it is available. If you stock up for a lump sum from timepoint X until timepoint Y to invest then the whole lump sum on timepoint Y, you would have gained more if you would have DCAd starting at X until Y.

Thats why I am not in favor of paying 3a on the 2nd of January. Whether you then pay it with the first salary/salaries in the new year or do it monthly it is mostly personal taste. Given that you invest the rest of the free money into 3b anyway.

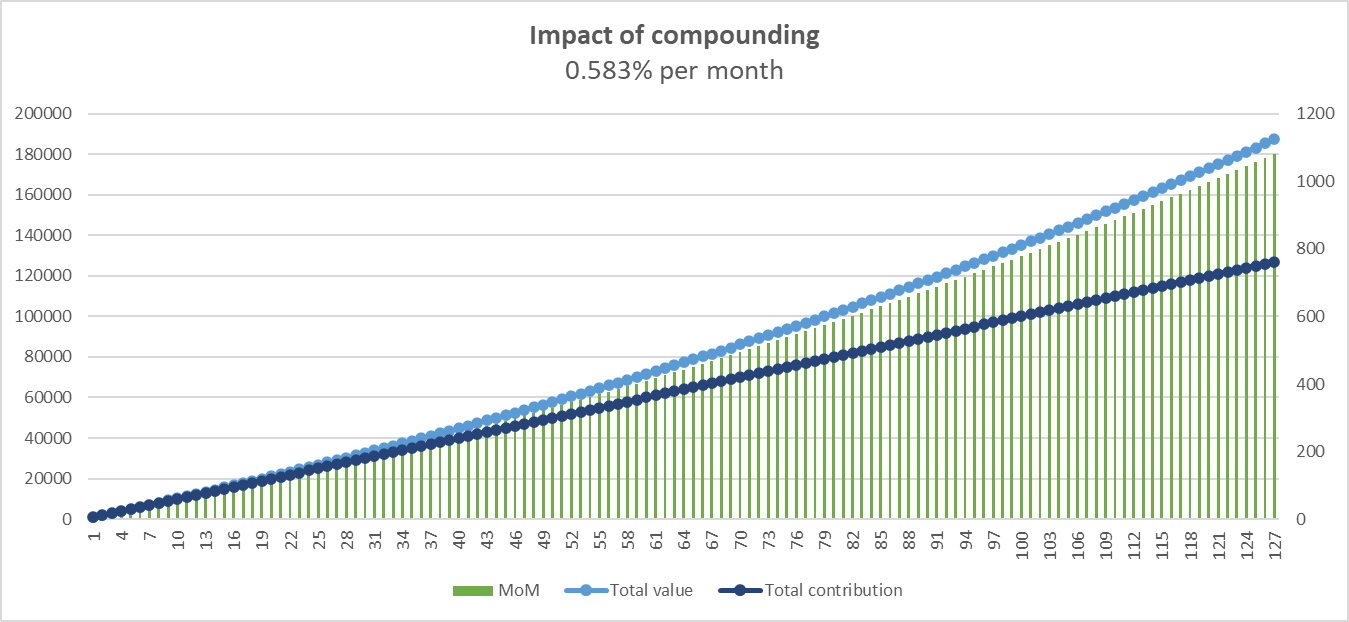

I have following numbers.

n = number of months

MoM = difference in portfolio value month over month minus monthly contribution

monthly contribution = 1000

Based on this, n>120 for MoM to cross 1000 per month

MoM is plotted on secondary axis on right side.

On average as in: for average people with nerves of steel, who invest the lump sum at market bottoms like Oct 2022, March 2020, early 2016, or February 2009.

If you took any month in the last 50 years and had invested a USD sum either all at once or in 3 parts, each a month apart, into MSCI World, after 1 year you’d have been better off in 68% of possible starting months. There are other calculations with different spreads (e.g. 6 or 12 months), all showing approximately the same ⅔ value in favor of lump-sum.

I believe the simulations are suggesting lumpsum because market generally goes up. But they don’t necessarily classify market conditions as suitable vs not.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.