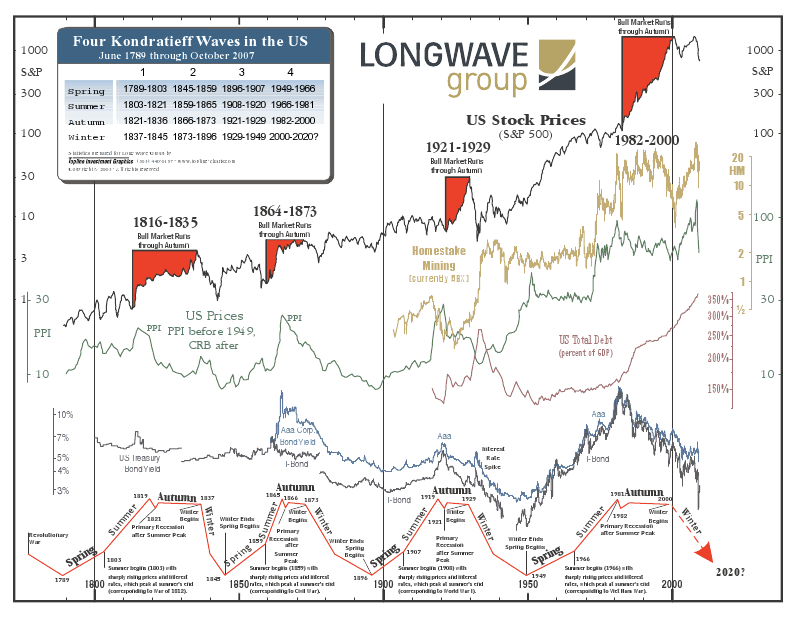

Does anyone else think we have entered spring in the Kondratieff cycle?

1 Like

A friend suggested an theory…

Currently central banks hold a lot of the treasuries of their governments. So a lot of debt is basically on the active and passive side of the countries balance sheet.

Now, if you were to simply net both, the debt goes down without any real harm to any real world investor.

Would this drive inflation? Probably not.

Would this reduce trust in the currency? Maybe a bit, but for USD and EUR probably no alternatives.

What do you think, is this the way out for a reset of the debt without a major craah?

For the US, that would apparently be 5 Trillions out of 35. I don’t think it makes a significant dent if nothing in the fiscal policy is changed.

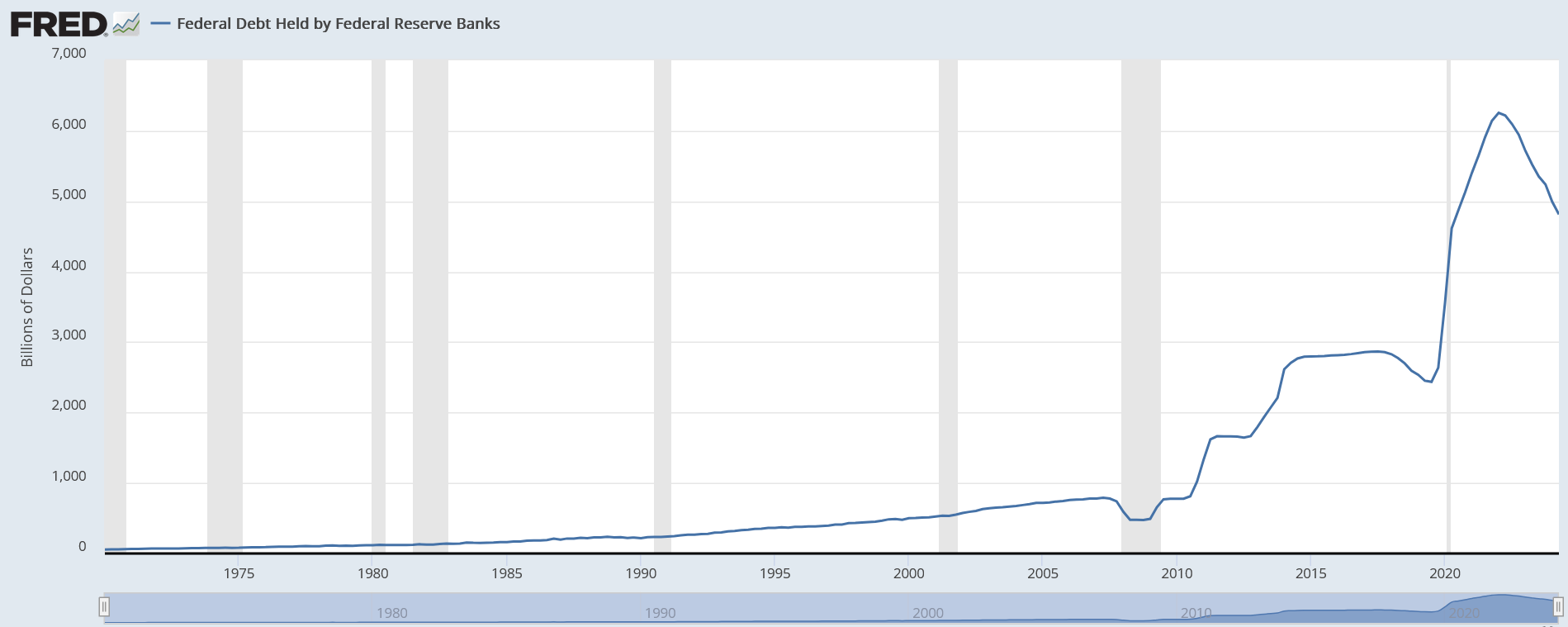

Federal debt held by federal banks:

Source: Federal Debt Held by Federal Reserve Banks (FDHBFRBN) | FRED | St. Louis Fed

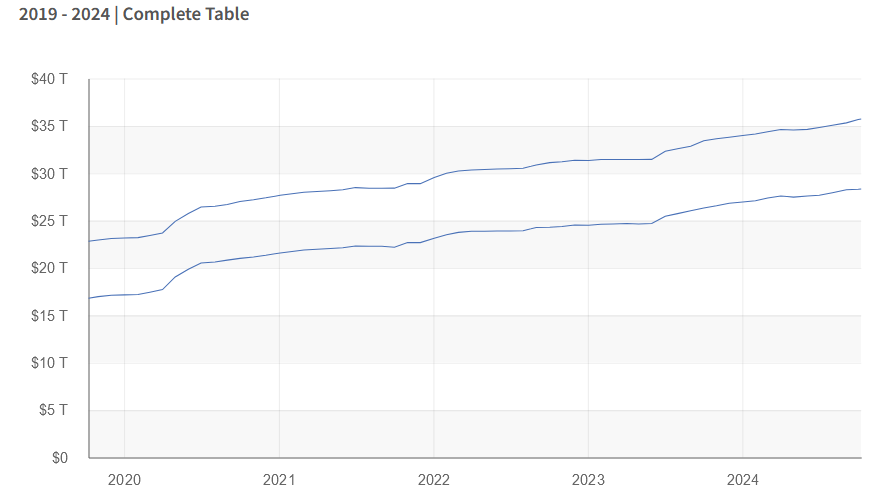

Total public US debt (higher curve, currently around 35T) and debt held by the public (lower curve, currently around 28T):

Source: Debt to the Penny | U.S. Treasury Fiscal Data

Sounds convoluted to me and I really don’t see the cycles in this graph. Can you educate me further on what makes each season of the Kondratieff wave and what would make the current times a spring of such wave?

Edit: I should be more precise: I don’t see cyclical patterns on the graph (the 1845-1896 seems particularly odd to me) and would fail to extend it; which leads me to assume that Kondratieff waves are not pure market events, in which case, knowing the underlying would be useful. I may be wrong but if it’s purely market driven, then I fail to see the cycles.

get a mortgage

Yes, I think a long term low interest fix will be a winner.

Do you think inflation in dollars will jump over to inflation in CHF? Or more likely that the dollar will lose more value compared to CHF? Probably a combination of both…

Well the long term trend has been for USD to decline vs CHF.

Though I wonder with China economy in trouble whether we actually get deflation exported to us over the next years.

As of 2023, approximately 40% of the revenue for S&P 500 companies is generated from outside the United States.

But also, companies are assets. When they’re denominated in USD, the assets are still worth the same as when they’re denominated in some other currency.

If the USD currency continues to devalue against other currencies like the CHF, then the price of these assets (in USD) will go up the same.*

* Probably more, as e.g. S&P 500 companies have been growing earnings with a close to 10% CAGR. Sure, that’s nominally and before inflation, but I’m pretty sure if you look at it measured in CHF, you still arrive at impressive numbers.

1 Like

If they stay the same asset, they do, but if their earnings prospects vs other investable assets diminishes as a result of the USD loosing value, then their intrinsic value diminishes too. That’s why the currencies in which the earnings are made and the liabilities are held would matter to someone trying to sort through companies to hedge against a potential crash of the USD. It’s quite a bit of work and has to be performed regularly so I’m not sure I’d go through it.

1 Like

I see your point.

I still wouldn’t bet against America (insert Warren Buffet quote here ![]() ).

).

2 Likes

Stock markets reached new highs even as Iran situation remains unresolved.

I can only imagine we’re in for one hell of a melt-up if the Iran situation is resolved nicely.

I’m more conservative/pessimistic, thinking that the market has priced in a “nice resolution” already and/or is delusional.

For me the melt-up will be when Trump is out.

3 Likes

I have the same opinion. Market basically prices Hormuz opening as being imminent. If it doesn’t open soon, we’ll have an inflationary meltdown.

1 Like

No one wants to escalate this more than the level where we are now, imho; the question is how much damage will the current situation do in the future, but that’s not known / not priced in / dependent of how current scenario will evolve. And it can resolve or go worse, but markets can’t just sell everything in case it will go bad. That’s how I think markets look at it.

1 Like

Meanwhile the portfolio goes from ATH to ATH…

1 Like

It looks like Trump has TACO’d. If this tanks oil stocks, I will be buying!