I’m curious in your case 1250.- you have included the augmented tax burden because of the ‘eigenheim’ fake income? If they added you 12000 of fake income and you are in the 20% tax regione that would mean 2400.- more taxes every year. And I assume you included insurance…? I’m not criticising I’m very interested in real life example.

On top of that two of the key price driver of homes are accessibility and frequency of public transportation and the presence of schools/jobs nearby. So it’s always difficult to really compare homes/apartments, since even if they are both 30 min from Lausanne one may be in a small city with all good things and the other lost in the fields with one bus every hour.

Finally, it is my personal experience that people owning a home are aaaaalways tinkering something, with higher frequency that they think. A new kitchen every 10-15 years, new heating system, painting and repainting, new light, remodeling and adding rooms and so on. More than 1% a year that is called maintenance, but many try to improve, not only maintain.

And if you think about it, you have to plan 1% of your total value just so that your asset won’t lose value. That’s insane. That’s much more than the 0.25% of ETF fees.

So I’m not against buying homes. It’s a marvelous feeling but it is an emotional decision. Until now for Switzerland I can’t make the numbers work. Because even if you are paying 4000 more per year, I’ll gladly pay that as “price of freedom” to be able to move wherever I want if job disappears in my region. And selling/renting out in a depressing market where everyone is going away (see Jura for a Swiss example) is going to hurt.

Regarding jlcollinsh, he makes some very good points indeed, but I guess some conditions in the US can hardly be compared to Switzerland. For instance hurricane, earthquake, companies closing (sufficient to have an impact on RE) or street gang moving is not very likely.

Currently I suppose the main risk is that the already stagnating prices could decrease when the interest rate increase (speaking of the Lausanne area at least)

I agree that most owner will actually not consider all costs when speaking of “their investment”. I’ve started to talk about it with friends, but it’s indeed difficult to have a clear picture.

The interest on the mortgage can be deducted from taxable income which compensate in part for the virtual renting tax. And a part of the 1250chf is the amortization so actually goes in the asset column.

Of course, I forgot the passive interest deduction.

I agree in Switzerland is very difficult to consider all aspects. You always need to compare apple with apple, so you can compare rent vs owning only when really similar: year of construction, proximity to public transportation and jobs and so on.

I personally moved 2 times in the last 3.5 years (with family), because I switched jobs (3 jobs in 3 different cities) and my salary went up 33%. That wouldn’t have been possible if I had bought a home. So it’s so damn difficult to assess something like this.

btw, one of the option I try to read upon was homes sold for bankruptcy by banks to recover the mortgage. They are usually cheaper but requires money in a short term. More information here: http://zwangsversteigerung.ch/

this could offer some nice investment opportunity, but the general advice is to participate in this bidding passively at the beginning to see how they work instead of jumping full in.

Yes they are cheaper indeed. A friend of me bought one during an auction.

It’s psychologically very difficult as you have to prepare everything not knowing against who you will be betting and have little time to decide.

Assuming 5% gross yield and long-term low mortgage rates, which currently seem to be floored at 0.7%, you can earn yourself a nice 7% after-tax ROE. And that’s just from rent alone. Add to it house prices appreciation of about 1-2% per year multiplied by mortgage leverage of 3-5x, and you’re eyeing some double digit returns here in the best scenario… There’s more stuff to consider here (cap gain tax, renovation), but I think 10+% total ROE is realistic.

It’s somewhat risky however - should the property market crash like in the 90s, it’ll leave you with a disproportionally huge debt and potentially can takes decades to recover

Well, I hate to say it, but the growth seems slowing down

Swiss-wide rental property prices have declined recently: https://data.snb.ch/en/topics/snb#!/cube/plimoincha. It’s understandable - yields deteriorated way too much, What idiot would buy at 2-3% I so often now see? 5% gross yield is where I draw the line. Further growth seems unsupported at the moment by economic factors: salaries ain’t rising, mortgage rates already hit rock bottom, rents are dropping due to reference rate catching up to them, net immigration slowing down…

The prices seem to be driven largely by condos/single family houses - small time buyers are getting overly excited over all time low mortgages and buy at whatever the price for rental savings. Probably we’re not really nowhere near a bubble burst point, given the draconian requirements banks have instituted for mortgages, but realistically I’d expect prices only moving sideways or very slowly growing. So not overpaying is more important than ever

Well, downturns happen all the time on the stocks market too and they are usually bigger than in RE. In the end, I think that investing in RE instead of in the stock market is a question of risk appetite/tolerance and how diversified you want your investments to be.

I think what matters the most in this high prices context is that you don’t overpay. I would consider in a 8-9% gross yield, at 5% I do not consider the risk worth the little reward.

I have never taken price appreciation into account, when calculating potential ROI for real estate. Most books & websites I have consulted for advice and insight seem to recommend against it.

One of the main reasons is that it is anyway very hard to cash in on appreciation for small scale players here in Europe. Most banks, in my experience, are very hesitant to refinance a property for anything more than the purchase + reconstruction costs at any time after purchase.

Another reason is that it is very hard to calculate or even guesstimate current value of a property unless you put it on the market and get some offers. It is by far the easiest for condo’s in relatively large complexes where a couple of similar units change ownership per year. Especially the Swiss market, where there is very little volatility and a large proportion of the market numbers we see is based on new construction – where different standards can have quite a bit of influence on prices.

Hello, if it’s not too late, I would recommend you to read the article on real estate in Switzerland, especially the part about The Price Bubble. The question needs proper calculation, but this is how it is because of the sudden inflation.

Hello! first message in this community, so I hope I’m not breaking any rule

(I’m talking about the “excel-like” sheet of calculation posted by hedgehog)

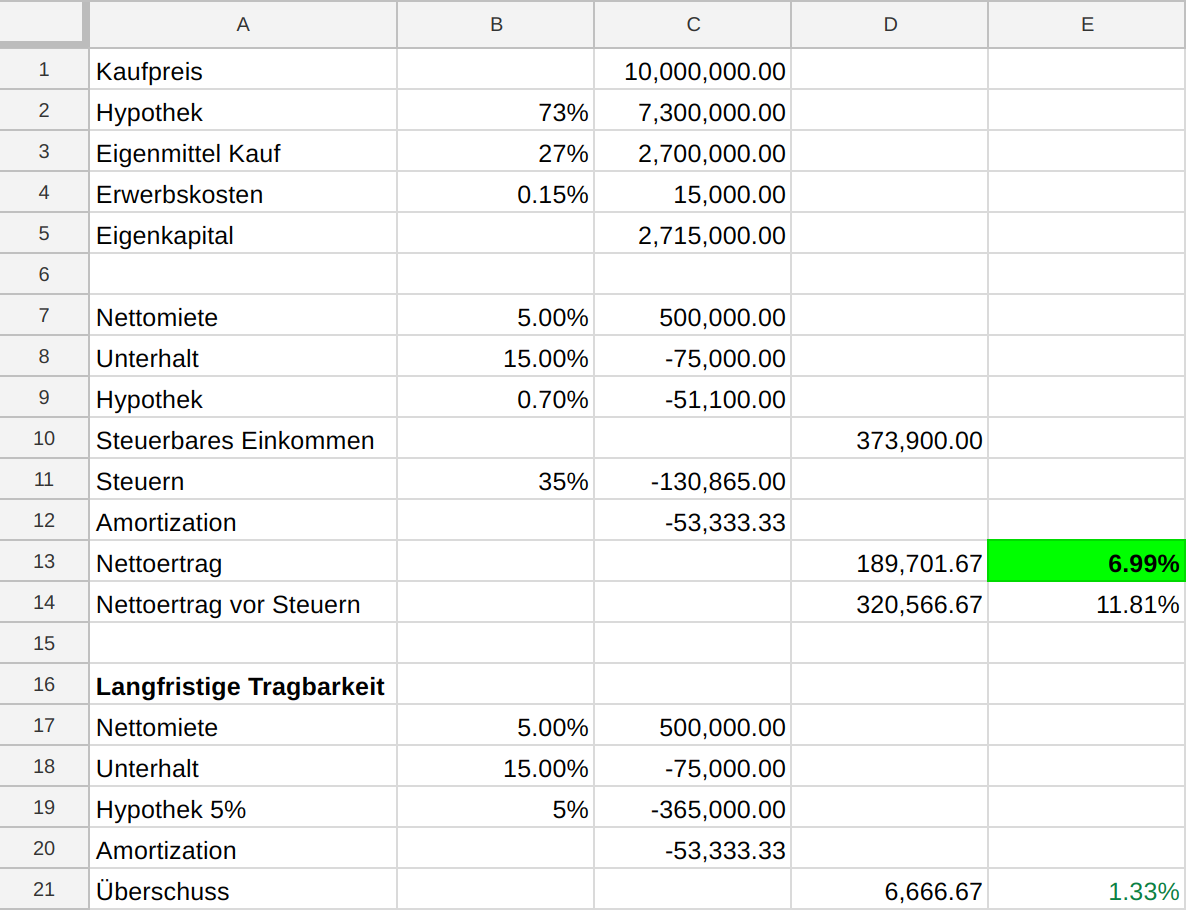

I now I’m referring to a few years old message, but I really have doubt about this: using the translating skills granted me by online dictionaries I see that the purchase cost is 10M while the ‘nettomiete’ (net rent, right?) is 500k (per year, I assume).

In what world would this happen? Legit question. That would be an insame rental income for this investment.

The completely oblivious to the rest of the calculation, but they seem futile compared to the above doubt.

Right, 5% Nettomiete is quite insane. But often, it is even lower in Switzerland. In the Zurich area it is not unusual to see 4% or less Bruttomiete (so, before the deductions for Nebenkosten (heating, etc.)).

No wait, I meant 5% it’s insanely high for my standard.

In northern Italy, Bologna, an apartment in the center valued 250k€ would rent for 750€/month “brutto”, i.e. <4% of gross rental yield, but then you have to subtract -21% fixed taxes (I’m simplifying) - 1k of build servicing and - who knows how much in extra maintenance (e.g. roof). We are solidly below 2,5% of net rental yield.

A semidetached house valued 300k€ 30 min away from the city (in a very well served village, with train, highway, everything) would rent for the same, maybe 800-850. Even an inferior yield, because of the the more expensive extra renovations.

The top yield would be a studioflat: around 80k for a rent of 500/month (pre-covid at least), yielding possibly a little more then 5% net RY.

All of this assuming 0 months of vacancies!

So when i said 5% is insane I meant insanely high.

Ah OK . But as you say, when you deduce extra maintenance (infrequent but costly renovations like the roof), taxes, insurance premiums and the “normal” maintenance (costs you see +/- every year) the 5% melt quickly enough… So it should be rather a floor than a ceiling rate IMHO. Caveat emptor!

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.