I don’t think the base currency matters… All it does is change the currency in your reports. So it would make sense to use the currency of your tax domicile.

Otherwise the base currency is not magic, you hold different currencies like you hold stocks. Your CHF that you send in are still CHF, they don’t get converted to the base currency for free or anything.

The latter part being one reason why your chosen base currency does matter. But sure… if you cut-off the quote halfway, then I guess it is far easier to make your false claim that it doesn’t matter and “only changes the currency in your reports”.

So for the benefit of everyone else: IB will deduct fees from your base currency. If you transfer CHF but only buy US-domiciled shares, changing your base currency to USD has the benefit of not needing to keep two separate currency balances in your account.

If however you find it simpler from a tax-reporting standpoint to keep your base currency in CHF, then we have now successfully found two reasons why your chosen base currency actually matters

I honestly fail to comprehend how it makes “far” more sense to set it to USD, even in these circumstances.

What’s the substantial benefit of sweeping your CHF balance in its entirety vs. keeping a residual (in absolute terms, not IBKR’s forex conversion terms) balance of 20 CHF or so?

It’s like the equivalent of having a 20 Franc bill lying around somewhere at home, in my wallet or in my pants. Even as the most cashless guy under the sun (which I pretty much am, considering I can’t remember the last time I’ve used cash), I am not going to worry about that amount lying around. Anywhere.

On the other hand, having the base currency set in CHF - and the tax office accepting my reports “as is”, a one-line item on my tax return - makes my tax declaration so much easier and convenient… I’d gladly pay outright the (minuscule) opportunity cost of not having those 20 CHF fully invested.

Great, you ended up answering it yourself. So we can agree that one instance where it can make “far” more sense is if you don’t fill in a tax return yourself, the DA-1 form, etc., but instead pay a tax consultant to do it on your behalf. Then you just send the IB report as-is and save yourself from having to fuss about two currencies, a residuals bucket for fees, etc., each time you deposit money into your IB account (e.g., 12 times a year).

And in your situation, I agree that there’s merit in keeping the base currency in CHF. The point is simply that base currency does matter contrary to what @Double_A wrote, and that it has more implications than just simply “change the currency in your reports” (and just to reiterate, the implication being which currency your fees are deducted from).

The tax consultant won’t be doing anything different than I do, will he?

And what would he do differently?

The point is: in the end, my obligation as a Swiss resident and taxpayer is to report income in CHF - not USD. Why would someone prefer a report in USD then? (Answer: if the tax office doesn’t accept IBKR‘s currency conversion for the amounts reported. In practice and my experience though, they did).

Isn’t that the situation of a lot, or most people on this forum?

Base Currency lets you modify the base currency for your account. Your base currency determines the currency of translation for your statements, the currency used for determination of margin requirement, and for a Cash Account, the currency of products you are allowed to trade. In addition, charges related to market data and research, inactivity fees, and commissions on Forex trades are also charged in your base currency.

The base currency defines:

statements currency

inactivity fee

Forex trades like buying CHF

It does not define the fee for buying ETF:

USD ETF will generate USD fees even if your currency base account is CHF

CHF ETF will generate CHF fees even if your currency base account is USD

How would you know? In any case, you’re getting way too excited about all of this now… it’s not at all clear what you’re even arguing about at this point. I guess it all likely stems from me initially acknowledging Bojack for making this clear, as the majority of your forum activity always appears to be counter-arguing anything that he contributes.

Great overview of why it matters more than simply what currency you like to see on your statements. Thanks!

I am not disputing in any way that choice of base currency matters regarding the currency balance that fees will be charged be in (though that were insufficient, I have little doubt IBKR will liquidate others to charge fees, on a cash account).

You also made a claim though: “if you’re only making US-domiciled purchases on IBKR, then it makes far more sense to have your base currency”.

…and generalised that for CHF-/Swiss-based investors: “I feel that a lot of people are complicating things by setting their base currency to CHF”

I agree with xorfish that CHF as base currency makes the declaration easier. Which is why I would recommend CH-based / CHF-earning investors to set their base currency to CHF.

I am just recommending to make the ease of Swiss tax declaration the deciding factor for these investors - or Swiss and that I would therefore recommend basing their IBKR in CHF.

…unless I am missing something important. The discussion doesn’t make think that so far.

What does it have to do with Bojack?

It doesn’t have to do anything with him. I’m not on a personal vendetta or anything against him. He‘s quite the prolific contributor on the forum. Who happens to have an opinion on things and is not afraid to voice them on the forum. And I commend him for that. He‘s just statistically a likely target to bounce contrary replies off of, I guess.

They’re not using the official exchange. As for the ones they do use in their reports, I just checked my statement, cause it’s not quite obvious from the layout itself which FX they’re using to report for individual dividend payments (this is just a small excerpt):

“Total” is a (sub)total of USD gross dividends for the full year, in USD (payment currency)

“Total in CHF” is the (sub)total of USD gross dividends, converted to the base currency CHF*

("Total Dividends in CHF is the sum of all gross dividends across all currencies)

* comparing to the USD 178.94, it is crucially not using the year-end FX rate for USD/CHF of 0.88xxx (ICTax has is at 0.883944, other sources differ slightly but it’s 0.88xxx everywhere).

This shows they are not just adding USD gross dividends over the year and then converting that sum at year end FX rate (which would be wrong).

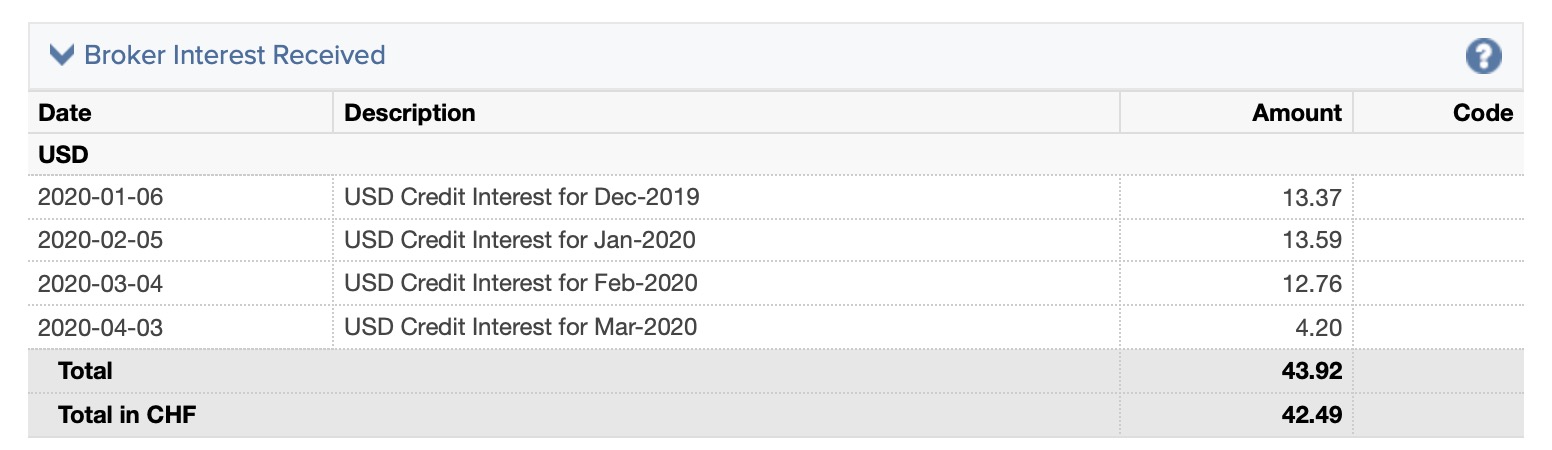

It’s more obvious from the broker interest statement, where I happened to only receive interest in the first four months of the year - when USD/CHF was between 1.00 und 0.975:

(Again, this is a statement for the full year 2020, I just happened to receive no interest from May on, for lack of eligible balance or change in interest rate)

Seems to confirm that “Total in CHF” is the sum of received interest/dividends, each converted at their historical exchange rates.

Therefore I’m confident about copying the totals into my tax return. It’s not exact to the point of using ICTax rates, but the values are based on rates at the distribution/payment date. Close enough.

I am for the first time putting something in my tax declaration as a Sammelposten, 2 positions IB “cash” and “stocks”. This thanks to tips from @San_Francisco and others, if I remember correctly.

The dividends are nicely in one chapter, incl a total for WHT. The buy/sell transactions with dates in another.

I have no idea if this will be definitely accepted though.

fwiw, the annual report is hard to parse for withholding tax since it can mix two years (previous year adjustment is mixed with current year withholding).

If a fund end up having non-qualified distribution, the withholding usually get refunded the next year (you’d see that with BND for example since most of the interests have no withholding). The dividend report will have the correct split and numbers (which is why it is made available much later since they need to receive the data from all the funds).

Oh, ok. Oops. Didn’t realise that. Thanks. So do u know when will dividend report become available, does it depend on my holdings?

And is this to do with dividend accruals, totally don’t understand this chapter, although it’s really only a small amount so chose “to ignore it”.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.