Since Zurich tax office even let you deduct 0.3% , I am wondering if there is some sort of regulations which drive this.

Otherwise - it’s insane to have % based fees.

Since Zurich tax office even let you deduct 0.3% , I am wondering if there is some sort of regulations which drive this.

Otherwise - it’s insane to have % based fees.

Good summary.

For me, following is true

I am not worried about losing my assets (due to broker bankruptcy etc) because I know brokers / banks need to segregate assets and eventually the underlying securities are the same.

For me diversification of providers also gives a chance to learn about services from various providers and hedges the risks from fraud/individual mistakes. And to be honest I like to support Swiss economy too. So any broker I will have other than IB will be Swiss.

I did not argue that this is a pleasant thing. Unpleasant for sure.

But i would not overdramatize it.

Your 8% is nominal. I prefer 4% real as a measure for expected return

I expect these fees not to grow with inflation, competition with IBKR and other will continue putting pressure on them.

I would say not exactly.

Cheap brokers register all customer’s securities at a Central Securities Depositary in their name. This is called “omnibus” account. If S really hits the F, the broker busts and isn’t able to sort out who owns what and how much, it will take quite some efforts to settle this situation.

At least Swissquote claims to register securities at customer’s name. Therefore if they are bust, it has no impact on customers.

En cas de faillite de Swissquote Bank SA, l’intégralité des titres est garantie dans la mesure où ils sont en dépôt auprès des dépositaires respectifs qui les conservent en votre nom.

(When I checked few years ago, there was an error in the English translation of this phrase, therefore here is the original in French).

Do you know if registration in the investor’s name works with mutual funds? In other words that MF provider knows who ultimately owns the shares?

No idea, sorry. I check conditions for Swiss mutual funds sometimes but don’t see anything interesting. But I guess they work differently.

Thanks for your reply. I just thought that the mechanics of MF forces not to register in street name.

In principle street name should be fine if the broker doesn’t commit fraud. Registration in client’s name (did not know that some offer sucb thing, no idea how it is done) would be also succeptible to fraud on the broker’s side.

Depends, I will pay 0.4% p.a. towards ZKB and I will gladly do that. Why?

IBKR is not a a bank, it’s a securities broker dealer! ![]()

I believe the features of ZKB you are referring to are for their banking features not custody accounts. So that makes them a great bank but it doesn’t make them a good custody account.

I mean the first three points are for cash deposits / kassenobligation etc. that’s where this unlimited guarantee plays a role

So much this.

I tried using IBKR, multiple times, and it just didn’t click with me. I don’t think I could sleep well having all my money invested there.

Investing can already be enough difficult emotionally for some people even during bull markets, no need to increase the uneasiness even further. And if someone, even after educating themselves, still feels like they want a Swiss bank/broker, then that’s perfectly fine IMO.

I’m even thinking about leaving neon when my portfolio reaches 6 figures, as I’m not totally convinced of their cyber security prowess. Even though I couldn’t prove to you that PF or SQ are more secure.

Aah, yes. Triple-A.

Let me quote from The Devil’s Financial Dictionary by Jason Zweig (highly recommended, btw):

I’ll add — albeit only with my personal guarantee — that ZKB had a bunch of those MBS (mortgage-backed securities) on their books as well.

Speaking of guarantees …

“Unlimited”

You can write down that word, but my feeling is that the canton of Zurich does not have unlimited funds?

![]()

In fact, I’m even tempted to prefer former UBS (or former CS) over ZKB … hear me out:

In case of, ahem, issues, the Swiss state and the Swiss National bank will jump in and settle things within a weekend if necessary.

In case of issues with ZKB, the canton of Zurich would need to backstop first / instead of the Swiss state and the Swiss National bank with both slightly deeper pockets than the canton of Zurich.

At the very least there would be more arguments with more parties involved - it’s like when you have two insurances for the same thing: they’ll argue about who pays how much before you get their money.

At any rate, I’m only playing (financial) devil’s advocate here so please take this with a grain of salt.

Also, anything that makes you sleep well is good for you.

Me, I sleep better paying fewer fees.

I agree that fees matter and credit ratings do not provide any guarantees, moreover, a bankrupt broker would certainly add some few gray hair (or remove hair forever), it should not lead to a substantial loss of the assets. There could be some losses due to fraud or messed up records, but these should not be high and likely covered by investor compensation schemes.

Where local banks stand out is that they … well local. It’s easier to deal with in case of a problem.

As we say in German:

Deine Worte in Gottes Ohr!

I agree with you, certainly from a bank client perspective.* I do my banking with Raiffeisen.**

* Then again — speaking now mainly as an investor — some local US banks are the ones that got caught with duration risk (I haven’t heard of any — local or not — Swiss banks getting caught up on having to mark-to-market their long duration CHF bonds). Or they have an unhealhy proportion of credit exposed to office space which is cratering in some areas (Switzerland again seems shielded from that).

You can say this is all specific to the US, I would say that with local banks you’re just dealing with different risks, both as a client as well as an investor.

** But not my investing.

No disagreement about that! Banks are inherently risky, and in case of bankruptcy your ETFs should be just fine, separated from the bank’s activa and just yours. However, the recent history shows that large systemically important banks are saved. The question that is often debated is what would be saved in the next crisis, it might not be their brokerage department; my opinion is that systemic banks are likely to be saved as a whole.

But bankruptcy is not all, I would even say one of the lesser concerns. In my books the following risks are more likely to have a negative impact than a bancruptcy

The lesson that I draw is that diversification is a reasonable thing to do. You decrease impact of severe event and pay by multiplying the chance of such event and make the portfolio more complex. Where I am stuck at the moment is what share of my stocks to custody at IBKR.

I just found, read, and really liked that article on bankeronwheels.com.

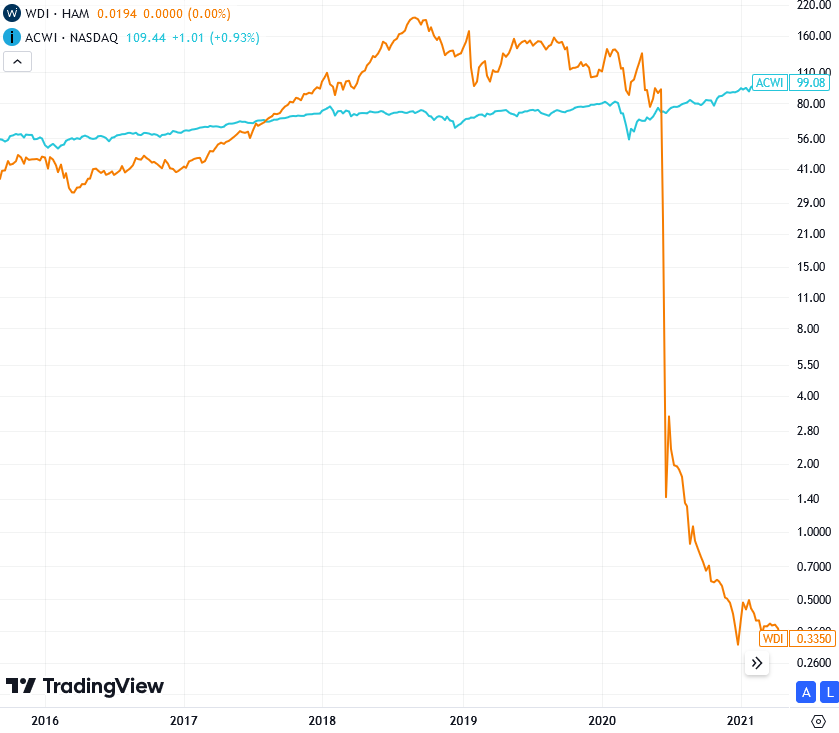

He suggests monitoring the credit rating and stock prices of your broker. Credit ratings seem to be behind paywalls, but stock prices are free. After insiders, the next best informed would be the market. I just added the tickers in the “Stocks Widget” app on my smartphone.

I also added an alert at 20% below. Could even less still be safe or do I need to set it higher? I’m not sure. Looking at Wirecard (orange) vs iShares MSCI ACWI ETF (blue):

Amid news of unsound accounting practices, fraud and money laundering, the share price fell steadily by 50%. In June 2020, it became known that 1.9 billion EUR was missing. The market then decided that was it and pulled the plug.

Here a graph with IBKR, FlatexDegiro, Swissquote:

IBKR had a similar 50% drop in the same timeframe, and FTX and SQN in a shorter one. FTX recently had a drop of 80%.

To be honest, I wouldn’t know which broker would go bust next. How would you tell?

Afterwards.

I’ll see myself out…

There is a “small” problem on this reasoning.

Say you see that SQ has problems and the stock goes down a lot. What do you do? You sell your stocks to move the money elsewhere? That might be the wrong thing to do, since you now gave money to SQ and that is not insured. If you leave your stocks/etf intact, you can get them out once (if) SQ fails.

Perform a title transfer to another broker?

Credit ratings can usually be found on the investors relation website or annual reports.